|

市場調查報告書

商品編碼

1766226

血管通路設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Vascular Access Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

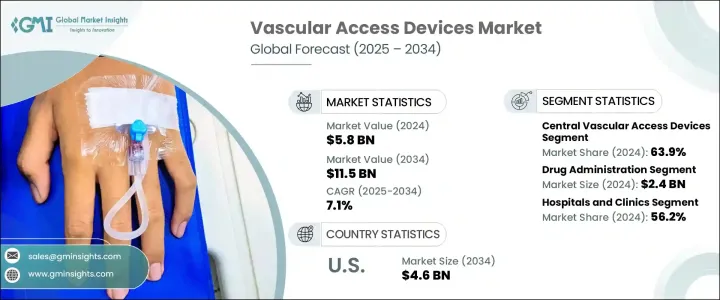

2024年,全球血管通路器械市場規模達58億美元,預計2034年將以7.1%的複合年成長率成長,達到115億美元。由於需要長期或反覆靜脈注射治療的慢性疾病負擔日益加重,這些器械的需求也隨之成長。在整個醫療保健領域,接受重症治療的患者通常需要持續的藥物傳遞、營養支持或液體管理,這需要可靠的血管通路解決方案。

在臨床環境中,血管通路設備對於輸送藥物、抽血、輸液以及執行其他關鍵操作至關重要。隨著需要重症監護、外科手術和專科治療的患者數量不斷增加,其角色也變得更加重要。隨著發展中國家醫療保健體系的擴展以及成熟市場的技術升級,無論是在急性護理環境中還是非急性護理環境中,對血管通路設備的需求都在持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 58億美元 |

| 預測值 | 115億美元 |

| 複合年成長率 | 7.1% |

這些設備專為提供直接且高效的血流路徑而設計,可用於多種治療。它們廣泛應用於外科手術等短期治療,以及透析或化療等長期治療。隨著醫療保健模式轉向門診和居家照護模式轉變,這些設備在院外的使用也日益受到關注。設備材料和設計的創新有助於提高安全性,最大限度地減少感染和血栓等併發症,並提高醫務人員的易用性。因此,血管通路設備已成為現代醫療保健服務不可或缺的一部分,確保病人安全和手術效率。

市場分為周邊血管通路和中心血管通路。 2024年,中心血管通路佔據主導地位,佔市場總收入的63.9%。這些器械通常在需要持續或重複靜脈治療的情況下更受歡迎,尤其是在複雜的治療方案中。它們能夠長時間保持原位並將藥物直接輸送到大靜脈,因此特別適合長期應用。在各種中心血管通路選擇中,周邊插入中心導管、隧道導管和植入式輸液港等器械因其較低的插入頻率和更高的患者舒適度而被廣泛使用。

該領域的最新進展推動了血管器械的開發,其抗菌性能和抗凝血特性均有所提升。這些產品升級旨在最大限度地降低長期使用相關的風險,例如導管相關血流感染,並提高器械的可靠性。此外,影像技術與置入技術的融合使置入更加精準和安全,有助於提高治療方案的整體效率。

從應用角度來看,藥物管理佔了最高的收入,到2024年將達到24億美元。由於慢性病患者對持續輸液治療的需求日益成長,該領域將繼續蓬勃發展。包括抗生素、生物製劑和免疫療法在內的藥物通常需要長時間的靜脈通路,這使得血管通路設備不可或缺。隨著醫療機構擴大支持家庭輸液服務和門診治療以降低住院成本,血管通路工具在家庭護理環境中也變得越來越普遍。

市場也按最終用戶細分,包括醫院和診所、門診手術中心、家庭護理機構等。醫院和診所成為領先細分市場,2024 年的市佔率為 56.2%。手術量的持續成長,以及急慢性病患者流量的增加,使得這些機構對血管器械的需求持續強勁。這些機構通常使用周邊靜脈輸液進行常規手術,並使用中心靜脈導管滿足更複雜的治療需求。感染預防和合規性是至關重要的考量,促使醫院投資採用封閉系統設計和抗菌材料的先進通路器械。

從區域來看,北美市場佔據主導地位,2024 年市場收入達 26 億美元,預計未來十年複合年成長率將達到 7%。在北美地區,美國血管通路器械市場預計將從 2024 年的 23 億美元成長至 2034 年的 46 億美元。長期健康狀況的日益成長,加上患者轉向門診治療和居家治療,推動了市場的持續擴張。在醫療服務提供者追求高品質治療結果和以患者為中心的解決方案的推動下,對有效、耐用且更安全的血管通路方案的需求仍然旺盛。

市場競爭格局涵蓋了專注於創新和產品性能的知名產業參與者。 2024年,像碧迪醫療、泰利福、貝朗、美敦力和費森尤斯醫療這樣的公司共佔據了全球約60%的市場。市場動態在很大程度上受到產品技術進步和成本考量的影響,尤其是在價格敏感的地區。跨國公司往往面臨在價格承受能力和品質之間取得平衡的壓力,而本土製造商則將自己定位為提供經濟高效且合規的替代方案的供應商。在未來幾年,這種創新與可近性之間的平衡仍將是血管通路器械市場的決定性特徵。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病盛行率不斷上升

- 微創手術日益受到青睞

- 技術進步

- 家庭醫療保健需求不斷成長

- 產業陷阱與挑戰

- 導管相關血流感染(CRBSI)風險高

- 先進血管通路設備成本高昂

- 成長動力

- 成長潛力分析

- 技術格局

- 定價分析

- 差距分析

- 未來市場趨勢

- 監管格局

- 專利分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 周邊血管通路裝置

- 中央血管通路裝置

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 藥物管理

- 液體和營養管理

- 輸血

- 診斷測試

- 其他應用

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院和診所

- 門診手術中心

- 居家照護環境

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Access Vascular

- AngioDynamics

- B Braun

- Becton Dickinson and Company

- ConvaTec

- Cook Medical

- Fresenius Medical Care

- ICU Medical

- Medical Components

- Medtronic

- Nipro

- Penumbra

- Teleflex

- Terumo

- Vygon

The Global Vascular Access Devices Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 11.5 billion by 2034. Demand for these devices is being propelled by the rising burden of chronic health conditions that require long-term or repeated intravenous therapies. Across the healthcare spectrum, patients undergoing treatment for serious ailments often require sustained drug delivery, nutritional support, or fluid management, which calls for dependable vascular access solutions.

In clinical settings, vascular access devices are essential for delivering medications, drawing blood, administering fluids, and performing other critical procedures. Their role becomes even more vital with the growing number of patients needing intensive care, surgical procedures, and specialized treatments. As healthcare systems expand in developing countries and upgrade technologies in established markets, the need for vascular access equipment continues to grow in both acute and non-acute care environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 7.1% |

These devices are specifically designed to provide direct and efficient access to the bloodstream for a range of treatments. They are widely used in both short-term scenarios, such as surgical procedures, and for long-duration therapies like dialysis or chemotherapy. As the healthcare landscape shifts toward more outpatient and home-based care models, the use of these devices outside hospital settings is also gaining traction. Innovations in device materials and design have contributed to greater safety, minimizing complications like infections and blood clots, and improving ease of use for medical personnel. Vascular access equipment has thus become integral to modern healthcare delivery, ensuring both patient safety and procedural efficiency.

The market is categorized into peripheral and central vascular access devices. In 2024, central vascular access devices held the dominant position, generating 63.9% of the total market revenue. These devices are frequently preferred in situations requiring consistent or repeated intravenous treatments, especially in complex therapeutic regimens. Their ability to remain in place for extended durations and deliver drugs directly into large veins makes them particularly suitable for long-term applications. Among the various central access options, devices such as peripherally inserted central catheters, tunneled catheters, and implantable ports are widely used due to their lower insertion frequency and enhanced patient comfort.

Recent advancements in this segment have led to the development of vascular devices with improved antimicrobial properties and anti-clotting features. These product upgrades are designed to minimize risks associated with prolonged usage, such as catheter-related bloodstream infections, and enhance device reliability. Additionally, the integration of imaging technologies in insertion techniques has made placements more accurate and safer, contributing to the overall efficiency of treatment protocols.

From an application standpoint, drug administration accounted for the highest revenue, reaching USD 2.4 billion in 2024. This segment continues to thrive due to the growing need for continuous infusion therapies in patients with chronic illnesses. Medications, including antibiotics, biologics, and immunotherapies, often require prolonged intravenous access, which makes vascular access devices indispensable. As medical practices increasingly support home infusion services and outpatient therapy to reduce hospitalization costs, vascular access tools are becoming more common in homecare environments as well.

The market is also segmented by end users, including hospitals and clinics, ambulatory surgical centers, homecare settings, and others. Hospitals and clinics emerged as the leading segment, with a market share of 56.2% in 2024. The consistent rise in surgical volumes, along with a higher patient inflow for both acute and chronic care, sustains a strong demand for vascular devices in these facilities. These settings frequently utilize both peripheral IVs for routine procedures and central lines for more complex treatment needs. Infection prevention and compliance with regulatory standards are critical concerns, prompting hospitals to invest in advanced access devices that incorporate closed-system designs and antimicrobial materials.

Regionally, North America led the market, generating USD 2.6 billion in revenue in 2024 and is forecasted to grow at a CAGR of 7% over the next decade. Within this region, the United States is expected to see its vascular access device market grow from USD 2.3 billion in 2024 to USD 4.6 billion by 2034. The increasing prevalence of long-term health conditions, combined with a shift toward outpatient care and at-home treatment programs, supports continued market expansion. The demand for effective, durable, and safer vascular access options remains high, driven by healthcare providers striving for quality outcomes and patient-centered solutions.

The competitive landscape of the market includes prominent industry players that focus on innovation and product performance. Companies such as Becton Dickinson and Company, Teleflex, B. Braun, Medtronic, and Fresenius Medical Care collectively captured approximately 60% of the global market share in 2024. Market dynamics are heavily influenced by advancements in product technology and cost considerations, particularly in price-sensitive regions. Multinational corporations often face pressure to balance affordability with quality, while local manufacturers position themselves as providers of cost-effective yet compliant alternatives. This balance between innovation and accessibility will remain a defining feature of the vascular access devices market in the years ahead.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing preference for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising demand for home healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of catheter-related bloodstream infections (CRBSIs)

- 3.2.2.2 High cost of advanced vascular access devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pricing analysis

- 3.6 Gap analysis

- 3.7 Future market trends

- 3.8 Regulatory landscape

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Peripheral vascular access devices

- 5.3 Central vascular access devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Drug administration

- 6.3 Fluid and nutrition administration

- 6.4 Blood transfusion

- 6.5 Diagnostic testing

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Access Vascular

- 9.2 AngioDynamics

- 9.3 B Braun

- 9.4 Becton Dickinson and Company

- 9.5 ConvaTec

- 9.6 Cook Medical

- 9.7 Fresenius Medical Care

- 9.8 ICU Medical

- 9.9 Medical Components

- 9.10 Medtronic

- 9.11 Nipro

- 9.12 Penumbra

- 9.13 Teleflex

- 9.14 Terumo

- 9.15 Vygon

靜脈通路裝置市場:按類型、年齡層、最終用戶和應用分類-2026-2032年全球市場預測

靜脈通路裝置市場:按類型、年齡層、最終用戶和應用分類-2026-2032年全球市場預測 全球靜脈通路裝置市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球靜脈通路裝置市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球靜脈通路裝置市場報告

2026年全球靜脈通路裝置市場報告 靜脈通路裝置市場規模、佔有率和成長分析(按產品、應用和地區分類)-2026-2033年產業預測

靜脈通路裝置市場規模、佔有率和成長分析(按產品、應用和地區分類)-2026-2033年產業預測 全球兒童血管通路市場按類型、應用和最終用戶分類-預測至2030年

全球兒童血管通路市場按類型、應用和最終用戶分類-預測至2030年 靜脈通路裝置:市場洞察、競爭格局及預測(至2032年)

靜脈通路裝置:市場洞察、競爭格局及預測(至2032年) 心室間隔穿刺系統:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

心室間隔穿刺系統:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 靜脈通路裝置市場:按裝置類型、應用、最終用戶、插入方法、材料和地區分類

靜脈通路裝置市場:按裝置類型、應用、最終用戶、插入方法、材料和地區分類 血管通路設備市場

血管通路設備市場 血管通路手術市場-全球產業規模、佔有率、趨勢、機會及預測(依手術類型、應用、地區及競爭格局分類,2020-2030 年預測)

血管通路手術市場-全球產業規模、佔有率、趨勢、機會及預測(依手術類型、應用、地區及競爭格局分類,2020-2030 年預測)