|

市場調查報告書

商品編碼

1766210

支氣管炎治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Bronchitis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

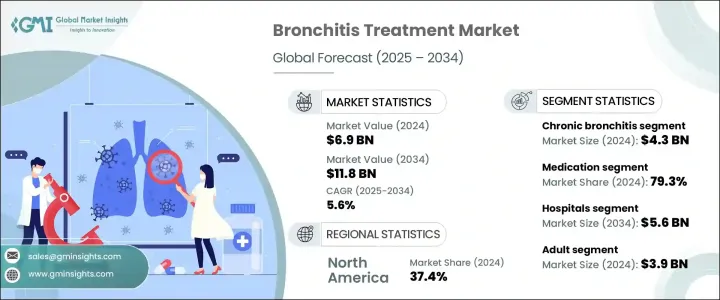

2024年,全球支氣管炎治療市場規模達69億美元,預計2034年將以5.6%的複合年成長率成長,達到118億美元。這一成長主要源於呼吸系統疾病負擔的增加,主要原因是吸煙、接觸環境污染物、職業危害以及反覆出現的病毒感染。急性支氣管炎通常與流感和呼吸道合胞病毒等季節性病毒有關,如今發生率越來越高,尤其是在寒冷的月份。呼吸系統疾病的增加推高了對有效支氣管炎療法的需求,從而推動了市場表現的提升,並促進了全球治療模式的創新。

全球人口老化顯著增加了對支氣管炎相關藥物和療法的需求。由於免疫力下降和肺功能減弱,老年人更容易罹患慢性呼吸系統疾病。隨著65歲及以上老年人口的不斷成長,支氣管擴張劑、抗發炎藥物和其他吸入治療藥物的消耗量也不斷增加。支氣管炎是指支氣管的炎症,通常透過緩解呼吸道發炎、稀釋粘液、止咳和改善呼吸功能來治療。大多數患者需要藥物治療,例如支氣管擴張劑、祛痰藥和抗發炎藥物。在病情較為嚴重的情況下,可以引入氧氣治療來幫助患者有效地控制呼吸。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 69億美元 |

| 預測值 | 118億美元 |

| 複合年成長率 | 5.6% |

2024年,慢性支氣管炎細分市場收入達43億美元。由於慢性支氣管炎具有持續性和長期性,需要持續的醫療監督和複雜的治療策略,該細分市場將繼續成長。與急性支氣管炎的短暫性不同,慢性支氣管炎需要持續管理,並且經常與慢性阻塞性肺病 (COPD) 等疾病重疊,這進一步增加了對持續護理的需求。隨著全球老化人口的成長,長期呼吸系統疾病的病例也在增加,這推動了對慢性支氣管炎治療的額外需求。

2024年,藥物領域佔了79.3%的主導佔有率。此類別包括廣泛使用的藥物,例如支氣管擴張劑、止咳藥、黏液活性劑和其他治療藥物。這些藥物對於控制急性和慢性支氣管炎症狀至關重要。止咳藥和祛痰藥常用於控制持續性咳嗽並幫助排出呼吸道中多餘的黏液-這是支氣管炎患者最常見且最令人不適的兩種症狀。由於其在症狀控制方面已被證實有效,以及藥物輸送系統的持續創新(包括長效製劑和吸入劑型),該領域持續蓬勃發展,從而提高了患者的依從性和治療效果。

2024年,美國支氣管炎治療市場規模達23億美元,成為全球成長的關鍵貢獻者。人口對呼吸系統疾病的易感性日益增加是主要的成長動力。隨著人口稠密的城市地區越來越多的人接觸過敏原和污染,支氣管炎的診斷數量持續攀升。此外,美國擁有強大的醫療基礎設施、更廣泛的保險覆蓋範圍以及強化的公共衛生運動,所有這些都提高了治療的可及性。美國成熟的製藥業務以及持續的產品開發,進一步鞏固了其在全球支氣管炎治療領域的地位。

全球支氣管炎治療市場的主要參與者包括 Sunovion Pharma、Glenmark、Lupin、3M Pharmaceuticals、輝瑞、賽諾菲、利潔時、雷迪博士實驗室、勃林格殷格翰、強生、Teva Pharmaceuticals、葛蘭素史克、Aurobindo Pharmauticals 和默克。在支氣管炎治療市場運作的公司正在採取多管齊下的方法來提升市場佔有率。主要參與者正在大力投資研發緩釋製劑、吸入療法和藥物組合,以改善患者預後和依從性。正在尋求戰略合作夥伴關係和許可協議,以擴大產品線和地理覆蓋範圍。鑑於老齡人口的成長,許多公司正在加大對慢性支氣管炎解決方案的關注。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 增加醫療服務

- 呼吸系統疾病盛行率不斷上升

- 藥物開發和治療方案的進步

- 產業陷阱與挑戰

- 藥物依從性問題

- 替代藥物的可用性

- 市場機會

- 空氣污染和吸煙率上升

- 非處方藥供應不斷擴大,自我藥療趨勢日益增強

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 管道分析

- 定價分析

- 消費者行為分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

第5章:市場估計與預測:按疾病類型,2021 - 2034 年

- 主要趨勢

- 急性支氣管炎

- 慢性支氣管炎

第6章:市場估計與預測:依治療方式,2021 - 2034 年

- 主要趨勢

- 藥物

- 依藥物類型

- 止咳藥

- 支氣管擴張劑

- 黏液活性劑

- 其他藥物

- 按類型

- 處方

- 場外交易(OTC)

- 依給藥途徑

- 口服

- 鼻腔

- 注射劑

- 依藥物類型

- 氧氣治療

第7章:市場估計與預測:按年齡層,2021 - 2034 年

- 主要趨勢

- 兒科

- 成人

- 老年

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診所

- 居家照護環境

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3M pharmaceuticals

- Aurobindo Pharma

- Boehringer Ingelheim

- Dr. Reddy's Laboratories

- GlaxoSmithKline

- Glenmark

- Johnson & Johnson

- Lupin

- Merck

- Macleods Pharmaceuticals

- Pfizer

- Reckitt Benckiser

- Sunovion Pharma

- Sanofi

- Teva Pharmaceuticals

The Global Bronchitis Treatment Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 11.8 billion by 2034. This growth is being driven by an increasing burden of respiratory conditions, mainly due to smoking, exposure to environmental pollutants, occupational hazards, and recurring viral infections. Acute bronchitis, typically linked with seasonal viruses like influenza and RSV, is becoming more frequent, especially during colder months. This rise in respiratory illnesses is pushing up demand for effective bronchitis therapies, leading to stronger market performance and innovation in treatment modalities worldwide.

An aging global population is significantly boosting demand for bronchitis-related medications and therapies. Older adults are more likely to develop chronic respiratory conditions because of weakened immunity and diminished lung function. As the demographic aged 65 and over continues to expand, so does the consumption of bronchodilators, anti-inflammatory drugs, and other inhaled treatments. Bronchitis, defined as inflammation of the bronchial tubes, is typically treated by relieving airway inflammation, loosening mucus, calming cough, and improving breathing capacity. Most patients require drug-based therapies like bronchodilators, expectorants, and anti-inflammatories. In more severe cases, oxygen therapy is introduced to help patients manage their breathing effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 5.6% |

In 2024, chronic bronchitis segment generated USD 4.3 billion. This segment continues to grow due to the persistent and long-term nature of chronic bronchitis, which requires consistent medical supervision and complex therapeutic strategies. Unlike the short-lived nature of acute bronchitis, chronic bronchitis demands ongoing management and frequently overlaps with conditions such as chronic obstructive pulmonary disease (COPD), further escalating the need for continuous care. As older populations rise globally, cases of long-term respiratory disease are also on the rise, driving additional demand for chronic bronchitis treatment.

The medication segment held a commanding 79.3% share in 2024. This category includes widely used drugs such as bronchodilators, cough suppressants, mucoactive agents, and other therapeutic drugs. These treatments are essential for managing both acute and chronic bronchitis symptoms. Cough suppressants and expectorants are prescribed frequently to manage persistent coughing and help expel excess mucus from the airways-two of the most common and discomforting symptoms for bronchitis patients. The segment continues to thrive due to its proven effectiveness in symptom control and ongoing innovations in drug delivery systems, including long-acting formulations and inhalable formats, which improve patient adherence and therapeutic outcomes.

United States Bronchitis Treatment Market reached USD 2.3 billion in 2024, making it a key contributor to global growth. The increasing susceptibility of the population to respiratory illnesses is a primary growth driver. With more people exposed to allergens and pollution in dense urban areas, the number of bronchitis diagnoses continues to climb. Additionally, the country benefits from strong healthcare infrastructure, wider insurance coverage, and enhanced public health campaigns, all of which improve access to treatment. A well-established pharmaceutical presence, along with continual product development, is further solidifying the US market's position in the global bronchitis treatment landscape.

Major players in the Global Bronchitis Treatment Market include Sunovion Pharma, Glenmark, Lupin, 3M Pharmaceuticals, Pfizer, Sanofi, Reckitt Benckiser, Dr. Reddy's Laboratories, Boehringer Ingelheim, Johnson & Johnson, Teva Pharmaceuticals, GlaxoSmithKline, Aurobindo Pharma, Macleods Pharmaceuticals, and Merck. Companies operating in the bronchitis treatment market are adopting a multi-pronged approach to enhance market presence. Key players are heavily investing in R&D to develop extended-release formulations, inhalable therapies, and drug combinations that improve patient outcomes and compliance. Strategic partnerships and licensing agreements are being pursued to expand product pipelines and geographic reach. Many firms are increasing their focus on chronic bronchitis solutions, given the growing elderly population.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Disease type

- 2.2.3 Treatment

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased health access

- 3.2.1.2 Increasing prevalence of respiratory diseases

- 3.2.1.3 Advancement in drug developments and treatment options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Drug compliance issues

- 3.2.2.2 Availability of alternative medicines

- 3.2.3 Market opportunities

- 3.2.3.1 Increase in air pollution and smoking rates

- 3.2.3.2 Expanding over-the-counter availability and increasing trend of self-medications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Pricing analysis

- 3.8 Consumer behaviour analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnership and collaborations

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Acute bronchitis

- 5.3 Chronic bronchitis

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Medication

- 6.2.1 By drug type

- 6.2.1.1 Cough suppressants

- 6.2.1.2 Bronchodilators

- 6.2.1.3 Mucoactive agents

- 6.2.1.4 Other drugs

- 6.2.2 By type

- 6.2.2.1 Prescription

- 6.2.2.2 Over-the-counter (OTC)

- 6.2.3 By route of administration

- 6.2.3.1 Oral

- 6.2.3.2 Nasal

- 6.2.3.3 Injectable

- 6.2.1 By drug type

- 6.3 Oxygen therapy

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

- 7.4 Geriatric

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Clinics

- 8.4 Homecare settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M pharmaceuticals

- 10.2 Aurobindo Pharma

- 10.3 Boehringer Ingelheim

- 10.4 Dr. Reddy’s Laboratories

- 10.5 GlaxoSmithKline

- 10.6 Glenmark

- 10.7 Johnson & Johnson

- 10.8 Lupin

- 10.9 Merck

- 10.10 Macleods Pharmaceuticals

- 10.11 Pfizer

- 10.12 Reckitt Benckiser

- 10.13 Sunovion Pharma

- 10.14 Sanofi

- 10.15 Teva Pharmaceuticals

支氣管炎治療市場:2026-2032年全球市場預測(按藥物類別、治療方法、給藥途徑、年齡層、劑型、最終用戶和分銷管道分類)支氣管炎治療市場:全球市場按藥物類型、給藥途徑、分銷管道和最終用戶分類的預測-2026-2032年

支氣管炎治療市場:2026-2032年全球市場預測(按藥物類別、治療方法、給藥途徑、年齡層、劑型、最終用戶和分銷管道分類)支氣管炎治療市場:全球市場按藥物類型、給藥途徑、分銷管道和最終用戶分類的預測-2026-2032年 支氣管炎治療市場:按類型、治療方法、藥物類別、給藥途徑、分銷管道和地區分類

支氣管炎治療市場:按類型、治療方法、藥物類別、給藥途徑、分銷管道和地區分類 阻塞性細支氣管炎症候群市場規模、佔有率和成長分析:按治療層級、患者特徵、診斷和監測、最終用戶和地區分類 - 行業預測,2026-2033 年阻塞性細支氣管炎症候群市場:依藥物類別、治療類型、給藥方式、最終用戶和通路分類-2026-2032年全球預測

阻塞性細支氣管炎症候群市場規模、佔有率和成長分析:按治療層級、患者特徵、診斷和監測、最終用戶和地區分類 - 行業預測,2026-2033 年阻塞性細支氣管炎症候群市場:依藥物類別、治療類型、給藥方式、最終用戶和通路分類-2026-2032年全球預測 支氣管炎治療市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物類型、類別、最終用戶、地區和競爭格局分類,2021-2031年

支氣管炎治療市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物類型、類別、最終用戶、地區和競爭格局分類,2021-2031年 支氣管炎治療藥物市場規模、佔有率及成長分析(按藥物類別、類型、最終用戶和地區分類)-2026-2033年產業預測

支氣管炎治療藥物市場規模、佔有率及成長分析(按藥物類別、類型、最終用戶和地區分類)-2026-2033年產業預測 毛細支氣管炎市場-全球及區域分析:按國家/地區分類-分析與預測(2025-2035)

毛細支氣管炎市場-全球及區域分析:按國家/地區分類-分析與預測(2025-2035) 支氣管炎市場報告:2030 年趨勢、預測與競爭分析

支氣管炎市場報告:2030 年趨勢、預測與競爭分析