|

市場調查報告書

商品編碼

1766209

ELISpot 和 Fluorospot 檢測市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測ELISpot and Fluorospot Assay Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

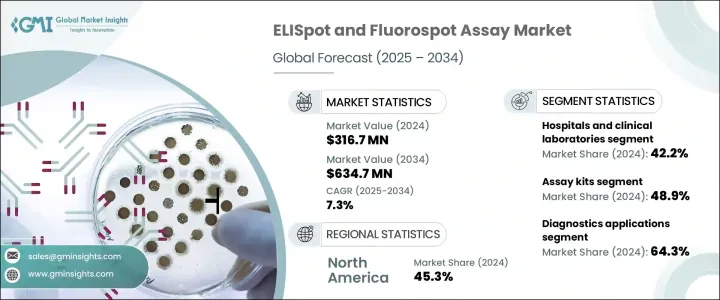

2024年,全球酵素連結免疫斑點 (ELISpot) 和螢光斑點 (Fluorospot) 檢測市場規模達3.167億美元,預計到2034年將以7.3%的複合年成長率成長,達到6.347億美元。 ELISpot是目前最靈敏的技術之一,可用於檢測細胞層面(尤其是T細胞或B細胞)的細胞激素或抗體分泌。螢光斑點檢測是ELISpot的延伸,它使用螢光標記技術,可以同時檢測單一細胞分泌的多種蛋白質。這兩種檢測方法都廣泛用於臨床研究、疫苗開發和臨床研究中的免疫監測。傳染病和免疫相關疾病的發生率不斷上升,是這些檢測需求成長的重要促進因素。

這些檢測在監測免疫反應中發揮著至關重要的作用,尤其是在針對傳染病的疫苗接種工作、免疫療法和疫苗研究中。結核病、癌症和新興病毒感染等疾病的發生率不斷上升,加劇了對先進免疫學檢測的需求。 ELISpot 和 Fluorospot 系統以其高靈敏度、單細胞解析度和多重分析能力而脫穎而出,使其成為臨床和研究免疫學中不可或缺的工具。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.167億美元 |

| 預測值 | 6.347億美元 |

| 複合年成長率 | 7.3% |

2024年,檢測試劑盒領域佔最大佔有率,達48.9%。這種優勢可歸因於標準化試劑盒的日益普及,這些試劑盒易於使用、可重複,且與細胞介導免疫研究框架相容。即用型試劑盒的便利性使其成為學術、臨床和藥物研究領域的首選。這些試劑盒因其在傳染病、癌症免疫治療和移植排斥監測中的作用而特別受歡迎。對細胞激素特異性檢測的旺盛需求促進了這些檢測方法的日益普及。此外,全球疾病負擔的不斷加重也持續推動對這些檢測解決方案的需求。

診斷應用領域在2024年佔最大佔有率,達64.3%。這主要歸因於酶聯免疫斑點(ELISpot)和螢光斑點(Fluorospot)檢測在各種傳染病(包括結核病、自體免疫疾病、癌症免疫療法和其他發炎性疾病)診斷中的應用日益廣泛。這些檢測方法的高精度使其成為臨床診斷中必不可少的工具,並使其成為精準醫療的關鍵工具。它們能夠識別和監測免疫相關疾病的進展,進一步推動了市場成長。這一趨勢凸顯了這些檢測方法在疾病診斷和管理中發揮的關鍵作用,鞏固了它們在臨床環境中的重要性。

亞太地區酵素連結免疫斑點 (ELISpot) 和螢光斑點 (Fluorospot) 檢測市場預計將實現最高成長,2025 年至 2034 年的複合年成長率為 8%。推動這一成長的因素包括:醫療保健技術的日益普及、免疫學研究的大量投入,以及該地區結核病和病毒感染等傳染病的日益普及。中國、印度和韓國等國家正迅速擁抱這些技術,這得益於其醫療保健意識的提升和完善的監管框架。生物製藥產業的蓬勃發展和臨床試驗活動的增多,進一步推動了對 ELISpot 和螢光斑點檢測等精準免疫監測工具的需求。

市場的主要參與者包括 Bio-Techne Corporation、BD、Mabtech、Oxford Immunotec、Bio-Connect、Cellular Technology、Abcam Limited、Stemcell Technologies、Autoimmun Diagnostika、Lophius Biosciences、GenScript Biotech、Merck、R&D Systems 和 U-CyTech。為了鞏固市場地位,酶聯免疫斑點 (ELISpot) 和螢光斑點 (Fluorospot) 檢測市場的公司正致力於透過開發創新、靈敏度更高、準確度和解析度更高的檢測方法,擴大其產品範圍。與學術機構、醫療保健提供者和製藥公司的合作正成為推動這些檢測方法廣泛應用的關鍵策略。此外,該公司正在投資研發,以增強現有產品線並開發下一代檢測方法。整合自動化、提高易用性和提供即用型試劑盒的努力,對於讓更廣泛的研究和臨床使用者更容易獲得這些檢測方法也至關重要。此外,策略性的區域擴張,尤其是在亞太地區等新興市場,使公司能夠滿足對先進診斷解決方案日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病和傳染病發生率上升

- 早期疾病診斷意識不斷增強

- 增加醫療支出和政府支持

- 產業陷阱與挑戰

- 缺乏熟練的人員

- 嚴格的監管要求

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

- 專利分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 檢測試劑盒

- 分析器

- 配套產品

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 研究應用

- 診斷應用程式

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院和臨床實驗室

- 學術和研究機構

- 生物製藥公司

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- BD

- Abcam Limited

- Autoimmun Diagnostika

- Bio-Connect

- Bio-Techne Corporation

- Cellular Technology

- GenScript Biotech

- Lophius Biosciences

- Mabtech

- Merck

- Oxford Immunotec

- R&D Systems

- Stemcell Technologies

- U-CyTech

The Global ELISpot and Fluorospot Assay Market was valued at USD 316.7 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 634.7 million by 2034. ELISpot is one of the most sensitive techniques available to detect cytokine or antibody secretion at the cellular level, specifically from T or B cells. The Fluorospot assay, an extension of the ELISpot, allows for the simultaneous detection of multiple proteins secreted from a single cell using fluorescent labeling. Both assays are widely used for immune monitoring in clinical research, vaccine development, and clinical studies. The rising prevalence of infectious and immune-related diseases is a significant driver for the increased demand for these assays.

These assays play a crucial role in monitoring immune responses, especially in vaccination efforts targeting infectious diseases, immunotherapies, and vaccine research. The growing incidence of diseases like tuberculosis, cancer, and emerging viral infections has intensified the need for advanced immunological assays. ELISpot and Fluorospot systems stand out for their high sensitivity, single-cell resolution, and multiplexing abilities, which make them invaluable tools in clinical and research immunology.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $316.7 Million |

| Forecast Value | $634.7 Million |

| CAGR | 7.3% |

In 2024, the assay kits segment held the largest share of 48.9%. This dominance can be attributed to the growing adoption of standardized kits that are easy to use, reproducible, and compatible with cell-mediated immunity research frameworks. The convenience of ready-to-use kits makes them a preferred choice in academic, clinical, and pharmaceutical research settings. These kits are particularly popular for their role in infectious disease, cancer immunotherapy, and transplant rejection monitoring. The high demand for cytokine-specific detection has contributed to the growing adoption of these assays. Furthermore, the increasing global burden of diseases continues to drive the need for these assay solutions.

The diagnostics application segment held the largest share 64.3% in 2024. This is primarily due to the increasing use of ELISpot and Fluorospot assays in the diagnosis of various infectious diseases, including tuberculosis, autoimmune disorders, cancer immunotherapy, and other inflammatory conditions. The assays' high accuracy makes them essential in clinical diagnostics, positioning them as key tools in precision medicine. Their ability to identify and monitor the progression of immune-related disorders further propels market growth. This trend highlights the critical role these assays play in both the diagnosis and management of diseases, cementing their importance in clinical settings.

Asia Pacific ELISpot and Fluorospot Assay Market is expected to witness the highest growth, with a CAGR of 8% from 2025 to 2034. The growth is driven by the rising adoption of healthcare technologies, significant investments in immunological research, and the increasing prevalence of infectious diseases such as tuberculosis and viral infections in the region. Countries like China, India, and South Korea are rapidly embracing these technologies, aided by heightened healthcare awareness and favorable regulatory frameworks. The growing biopharmaceutical industry and an increase in clinical trial activity are further contributing to the demand for precise immune surveillance tools like ELISpot and Fluorospot assays.

The market features major participants including Bio-Techne Corporation, BD, Mabtech, Oxford Immunotec, Bio-Connect, Cellular Technology, Abcam Limited, Stemcell Technologies, Autoimmun Diagnostika, Lophius Biosciences, GenScript Biotech, Merck, R&D Systems, U-CyTech. To strengthen their market position, companies in the ELISpot and Fluorospot assay market are focusing on expanding their product offerings by developing innovative and more sensitive assays that provide higher accuracy and resolution. Partnerships and collaborations with academic institutions, healthcare providers, and pharmaceutical companies are becoming a key strategy to promote the widespread adoption of these assays. Additionally, companies are investing in research and development to enhance their existing product lines and create next-generation assays. Efforts to integrate automation, improve ease of use, and offer ready-to-use kits are also crucial in making these assays more accessible to a wider range of research and clinical users. Moreover, strategic regional expansion, particularly in emerging markets like Asia Pacific, is enabling companies to tap into the growing demand for advanced diagnostic solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic and infectious diseases

- 3.2.1.2 Growing awareness of early disease diagnosis

- 3.2.1.3 Increasing healthcare spending and government support

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled personnel

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Assay kits

- 5.3 Analyzers

- 5.4 Ancillary products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Research applications

- 6.3 Diagnostics applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinical laboratories

- 7.3 Academic and research institutions

- 7.4 Biopharmaceutical companies

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 Abcam Limited

- 9.3 Autoimmun Diagnostika

- 9.4 Bio-Connect

- 9.5 Bio-Techne Corporation

- 9.6 Cellular Technology

- 9.7 GenScript Biotech

- 9.8 Lophius Biosciences

- 9.9 Mabtech

- 9.10 Merck

- 9.11 Oxford Immunotec

- 9.12 R&D Systems

- 9.13 Stemcell Technologies

- 9.14 U-CyTech

ELISpot 與 FluoroSpot 偵測市場:全球市場預測,2026-2032 年

ELISpot 與 FluoroSpot 偵測市場:全球市場預測,2026-2032 年 Elispot 和 Fluorospot 檢測市場規模、佔有率和成長分析:按產品系列細分、應用研究重點、最終用戶和地區分類—2026-2033 年產業預測

Elispot 和 Fluorospot 檢測市場規模、佔有率和成長分析:按產品系列細分、應用研究重點、最終用戶和地區分類—2026-2033 年產業預測 ELISpot 和 FluoroSpot 檢測市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、最終用戶、地區和競爭對手分類,2021-2031 年

ELISpot 和 FluoroSpot 檢測市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、最終用戶、地區和競爭對手分類,2021-2031 年 ELISpot 和 Fluorospot 檢測市場規模、佔有率、趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年

ELISpot 和 Fluorospot 檢測市場規模、佔有率、趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年 ELISpot 和 FluoroSpot 檢測的全球市場 - 全球規模、佔有率、趨勢分析、機會、預測,2019-2030 年

ELISpot 和 FluoroSpot 檢測的全球市場 - 全球規模、佔有率、趨勢分析、機會、預測,2019-2030 年