|

市場調查報告書

商品編碼

1766188

生物活性玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Bioactive Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

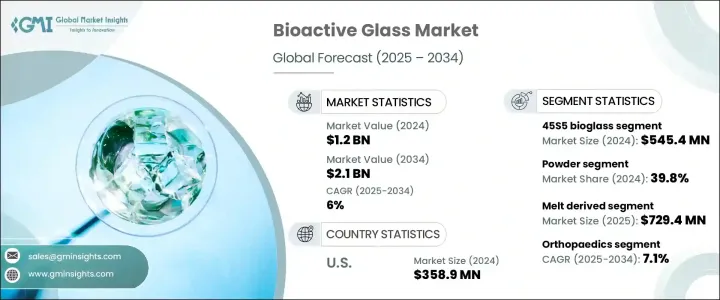

2024年,全球生物活性玻璃市場價值為12億美元,預計到2034年將以6%的複合年成長率成長,達到21億美元。這一成長主要得益於該材料獨特的再生特性,尤其是在生物醫學領域,生物活性玻璃與生物組織能夠產生積極的相互作用。與傳統的惰性材料不同,生物活性玻璃能夠促進軟組織和骨骼的主動再生,並具有成骨、血管生成和抗菌等優勢。這些特性使其成為廣泛臨床應用中的關鍵材料。在骨科領域,生物活性玻璃因其能夠刺激骨骼生長和整合,擴大應用於骨移植、脊椎融合和創傷修復。

在牙科領域,它被用於填充物、植入物和牙周治療。此外,它在再生醫學、藥物傳輸系統和組織工程中的作用也不斷擴大。溶膠-凝膠合成、熔融衍生技術和積層製造等新製造方法的發展,使得能夠生產具有可客製化孔隙率、分解速率和離子釋放曲線的客製化生物活性玻璃,從而進一步增強了其在醫療應用中的用途。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 21億美元 |

| 複合年成長率 | 6% |

2024年,S53P4(BonAlive)生物活性玻璃板塊的市值為3.871億美元,預計到2034年將成長至7.281億美元。 S53P4以其抗骨質疏鬆和骨骼刺激特性而聞名,使其在治療骨感染和慢性骨髓炎方面非常有效。這種生物活性玻璃成分即使在存在細菌感染的情況下也能促進骨形成,常用於骨科手術,尤其是在感染風險較高的手術中。歐洲和北美對生物活性玻璃的日益普及促進了該板塊的成長,尤其是作為骨骼替代品和抗菌劑。

預計到2034年,熔融法生物活性玻璃市場的複合年成長率將達到6.2%。這類生物活性玻璃透過熔融原料生產,其結構比傳統生物醫學玻璃更均勻緻密。熔融法生物活性玻璃在先進的組織工程領域尤其有用,它能夠提供多孔結構,增強生物活性和表面積。這項特性非常適合增強表面反應性和塗層等應用,這些應用可以透過火焰噴塗合成等可擴展方法來實現,從而形成奈米級玻璃粉末。

2024年,美國生物活性玻璃市場規模達3.589億美元。由於醫療和牙科應用對生物活性玻璃的需求不斷成長,尤其是在骨再生和矯正植體塗層領域,美國生物活性玻璃市場正在快速成長。生物活性玻璃因其與骨組織的優異相容性及其抗菌特性,在骨科、牙科和傷口癒合領域至關重要。骨質疏鬆症、骨折和牙科疾病的發生率不斷上升,進一步推動了市場的成長。此外,患者和醫療專業人員對微創治療益處的認知不斷提高,也推動了生物活性玻璃的普及。

全球生物活性玻璃市場的知名企業包括 Mo-Sci Corporation、Stryker Corporation(及其子公司 Ortho Vita, Inc.)、肖特股份公司、DePuy Synthes(強生公司)和 NovaBone Products, LLC。生物活性玻璃市場中的企業為鞏固其市場地位而實施的關鍵策略包括投資研發,以開發創新和客製化的生物活性玻璃配方。這些進步使企業能夠提供具有特定特性(例如可控離子釋放、增強生物活性和可調節分解速率)的客製化產品。

企業也致力於擴大產品組合,以滿足新興市場和醫療需求旺盛地區日益成長的需求。此外,與學術機構、醫療保健提供者和其他行業領導者建立策略合作夥伴關係,有助於企業提升市場影響力。此外,企業正在加大對行銷和教育活動的投入,以提高大眾對生物活性玻璃優勢的認知,這有望推動其在各個醫療領域的應用。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- Pestel 分析

- 價格趨勢

- 按地區

- 按成分

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計數據(HS 代碼)(註:僅提供主要國家的貿易統計數據

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依構成,2021 - 2034 年

- 主要趨勢

- 45S5生物玻璃

- S53p4(活著)

- 13-93生物活性玻璃

- 58S生物活性玻璃

- 70S30c生物活性玻璃

- 磷酸鹽基生物活性玻璃

- 硼酸鹽基生物活性玻璃

- 其他作品

第6章:市場估計與預測:依形式 2021 - 2034

- 主要趨勢

- 粉末

- 顆粒和微粒

- 支架和多孔結構

- 塗料

- 纖維和網狀物

- 複合材料

- 其他形式

第7章:市場估計與預測:依方法,2021 - 2034 年

- 主要趨勢

- 熔融衍生

- 溶膠-凝膠

- 火焰噴塗合成

- 微波處理

- 3D列印/積層製造

- 其他加工方法

第8章:市場估計與預測:按應用 2021 - 2034

- 主要趨勢

- 骨科

- 骨移植和骨替代物

- 骨空隙填充物

- 脊椎融合

- 創傷修復

- 其他骨科應用

- 牙科

- 牙齒填充物

- 牙種植體

- 牙周治療

- 牙髓科材料

- 其他牙科應用

- 組織工程與再生醫學

- 骨組織工程

- 軟組織工程

- 藥物輸送系統

- 其他組織工程應用

- 傷口癒合

- 化妝品和個人護理

- 其他應用

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 醫院和診所

- 牙醫診所

- 門診手術中心(ascs)

- 研究與學術機構

- 醫療器材製造商

- 製藥和生物技術公司

- 其他最終用途

第10章:市場估計與預測:按物業類型,2021 - 2034 年

- 主要趨勢

- 骨傳導性

- 抗菌活性

- 血管生成特性

- 生物分解性

- 其他屬性

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- MEA 其餘地區

第12章:公司簡介

- 3M Company

- Artoss, Inc.

- Berkeley Advanced Biomaterials Inc.

- Biomatlante

- Biomin Technologies Ltd.

- Biovision GmbH

- BonAlive Biomaterials Ltd.

- Cambioceramics BV

- Cerapedics, Inc.

- Curasan AG

- Dentsply Sirona Inc.

- DePuy Synthes (Johnson & Johnson)

- Ferro Corporation

- GC Corporation

- Matexcel

- Medtronic plc

- Mo-Sci Corporation

- Nippon Electric Glass Co., Ltd.

- Noraker

- NovaBone Products, LLC

- Orthovita, Inc. (Stryker)

- Pulpdent Corporation

- SCHOTT AG

- Septodont

- Stryker Corporation

- Synergy Biomedical, LLC

- TheraMetrics AG

- Wuxi Jinxin Science & Technology Co., Ltd.

- Zimmer Biomet Holdings, Inc.

The Global Bioactive Glass Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 2.1 billion by 2034. This expansion is largely driven by the material's unique regenerative properties, particularly in the biomedical field, where bioactive glass interacts positively with biological tissues. Unlike traditional inert materials, bioactive glass promotes active regeneration of soft tissues and bones, offering benefits such as osteogenesis, angiogenesis, and antimicrobial activity. These qualities make it a key material in a wide range of clinical applications. In orthopedics, bioactive glass is increasingly used in bone grafts, spinal fusions, and trauma repair due to its ability to stimulate bone growth and integration.

In dentistry, it is employed in fillings, implants, and periodontal treatments. Moreover, its role in regenerative medicine, drug delivery systems, and tissue engineering continues to expand. The development of new manufacturing methods, such as sol-gel synthesis, melt-derived techniques, and additive manufacturing, has enabled the production of tailored bioactive glasses with customizable porosity, degradation rates, and ion release profiles, further enhancing their use in medical applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 6% |

In 2024, the bioactive glass segment from the S53P4 (BonAlive) segment was valued at USD 387.1 million and is expected to grow to USD 728.1 million by 2034. S53P4 is known for its osteoporosis and osteostimulative properties, making it highly effective in treating bone infections and chronic osteomyelitis. This bioactive glass composition assists in bone formation, even in the presence of pre-existing bacterial infections, and is commonly used in orthopedic surgeries, particularly where infection risks are high. The increasing adoption of bioactive glasses in Europe and North America has contributed to the segment's growth, especially as a bone substitute and antimicrobial agent.

The melt-derived bioactive glass segment is expected to grow at a CAGR of 6.2% through 2034. This type of bioactive glass is produced by melting raw materials, resulting in a more homogeneous and dense structure than conventional biomedicine glass. Melt-derived bioactive glass is especially useful in advanced tissue engineering, offering porous structures with enhanced bioactivity and surface area. This property is ideal for applications such as surface reactivity enhancement and coating applications, which can be achieved through scalable methods like flame spray synthesis, allowing the formation of nano-sized glass powders.

U.S. Bioactive Glass Market generated USD 358.9 million in 2024. The market in the U.S. is growing rapidly due to the rising demand for bioactive glass in medical and dental applications, particularly in bone regeneration and orthodontic implant coatings. Bioactive glass is essential in orthopedics, dentistry, and wound healing due to its excellent compatibility with bone tissue and its antibacterial properties. The increasing prevalence of osteoporosis, bone fractures, and dental disorders is further fueling market growth. Additionally, the growing awareness of patients and medical professionals about the benefits of less invasive treatments is driving adoption.

Prominent players in the Global Bioactive Glass Market include Mo-Sci Corporation, Stryker Corporation (and its subsidiary Ortho Vita, Inc.), SCHOTT AG, DePuy Synthes (Johnson & Johnson), and NovaBone Products, LLC. Key strategies implemented by companies in the bioactive glass market to strengthen their position include investing in R&D to develop innovative and customized bioactive glass formulations. These advancements allow companies to offer tailored products with specific properties like controlled ion release, enhanced bioactivity, and adjustable degradation rates.

Companies are also focusing on expanding their product portfolios to meet the growing demand in emerging markets and regions with high medical needs. Additionally, strategic partnerships and collaborations with academic institutions, healthcare providers, and other industry leaders are helping companies enhance their market presence. Furthermore, players are increasing their investments in marketing and educational campaigns to raise awareness about the advantages of bioactive glass, which is expected to drive adoption across various medical fields.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Composition

- 2.2.3 Form

- 2.2.4 Method

- 2.2.5 Application

- 2.2.6 End use

- 2.2.7 Property

- 2.3 Tam analysis, 2025-2034

- 2.4 Cxo perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By composition

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (hs code) (note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Composition, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 45S5 bioglass

- 5.3 S53p4 (bonalive)

- 5.4 13-93 bioactive glass

- 5.5 58S bioactive glass

- 5.6 70S30c bioactive glass

- 5.7 Phosphate-based bioactive glass

- 5.8 Borate-based bioactive glass

- 5.9 Other compositions

Chapter 6 Market Estimates and Forecast, By Form 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Granules & particles

- 6.4 Scaffolds & porous structures

- 6.5 Coatings

- 6.6 Fibers & meshes

- 6.7 Composites

- 6.8 Other forms

Chapter 7 Market Estimates and Forecast, By Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Melt-derived

- 7.3 Sol-gel

- 7.4 Flame spray synthesis

- 7.5 Microwave processing

- 7.6 3d printing/additive manufacturing

- 7.7 Other processing methods

Chapter 8 Market Estimates and Forecast, By Application 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Orthopedics

- 8.2.1 Bone grafts & substitutes

- 8.2.2 Bone void fillers

- 8.2.3 Spinal fusion

- 8.2.4 Trauma repair

- 8.2.5 Other orthopedic applications

- 8.3 Dentistry

- 8.3.1 Dental fillings

- 8.3.2 Dental implants

- 8.3.3 Periodontal treatment

- 8.3.4 Endodontic materials

- 8.3.5 Other dental applications

- 8.4 Tissue engineering & regenerative medicine

- 8.4.1 Bone tissue engineering

- 8.4.2 Soft tissue engineering

- 8.4.3 Drug delivery systems

- 8.4.4 Other tissue engineering applications

- 8.5 Wound healing

- 8.6 Cosmetics & personal care

- 8.7 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Hospitals & clinics

- 9.2 Dental clinics

- 9.3 Ambulatory surgical centers (ascs)

- 9.4 Research & academic institutions

- 9.5 Medical device manufacturers

- 9.6 Pharmaceutical & biotechnology companies

- 9.7 Other end use

Chapter 10 Market Estimates and Forecast, By Property, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Osteoconductivity

- 10.3 Antimicrobial activity

- 10.4 Angiogenic properties

- 10.5 Biodegradability

- 10.6 Other properties

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 3M Company

- 12.2 Artoss, Inc.

- 12.3 Berkeley Advanced Biomaterials Inc.

- 12.4 Biomatlante

- 12.5 Biomin Technologies Ltd.

- 12.6 Biovision GmbH

- 12.7 BonAlive Biomaterials Ltd.

- 12.8 Cambioceramics B.V.

- 12.9 Cerapedics, Inc.

- 12.10 Curasan AG

- 12.11 Dentsply Sirona Inc.

- 12.12 DePuy Synthes (Johnson & Johnson)

- 12.13 Ferro Corporation

- 12.14 GC Corporation

- 12.15 Matexcel

- 12.16 Medtronic plc

- 12.17 Mo-Sci Corporation

- 12.18 Nippon Electric Glass Co., Ltd.

- 12.19 Noraker

- 12.20 NovaBone Products, LLC

- 12.21 Orthovita, Inc. (Stryker)

- 12.22 Pulpdent Corporation

- 12.23 SCHOTT AG

- 12.24 Septodont

- 12.25 Stryker Corporation

- 12.26 Synergy Biomedical, LLC

- 12.27 TheraMetrics AG

- 12.28 Wuxi Jinxin Science & Technology Co., Ltd.

- 12.29 Zimmer Biomet Holdings, Inc.