|

市場調查報告書

商品編碼

1755367

開關商用電壓調節器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Switching Commercial Voltage Regulator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

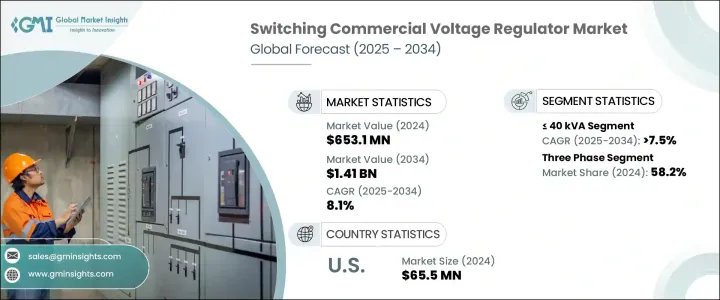

2024年,全球商用開關穩壓器市場規模達6.531億美元,預計2034年將以8.1%的複合年成長率成長,達到14.1億美元。這主要得益於對敏感設備精確保護需求的不斷成長,以及電能品質管理的重要性日益提升。人工智慧穩壓技術的進步有望進一步增強該產業的發展。此外,商業建築用電量的不斷成長以及對電湧的擔憂也促進了市場的擴張。將風能和太陽能等再生能源併入電網,刺激了對先進穩壓系統的需求。

世界各國政府都致力於提高能源效率,這進一步推動了對這些設備的需求,以最佳化功耗並降低營運成本。自動化、可靠和可程式數位系統的不斷進步,為商用電壓調節器市場帶來了新的成長機會。工業自動化的日益普及,以及資料中心和電信網路的成長,推動了對精確電壓調節的需求。隨著企業越來越依賴數位基礎設施,對穩定、精確的電力系統以支援關鍵營運的需求比以往任何時候都更加重要,這為電壓調節器創造了巨大的商機。隨著這些行業的持續成長,對高性能電壓調節系統的需求預計將激增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6.531億美元 |

| 預測值 | 14.1億美元 |

| 複合年成長率 | 8.1% |

預計到 2034 年,40 kVA 開關商用電壓調節器市場將實現超過 7.5% 的強勁成長率。這些電壓調節器對於保護敏感商用設備免受電壓波動的影響至關重要,可確保電腦、銷售點系統、暖通空調裝置和照明系統等電子設備的運作可靠性和使用壽命。

同樣,預計到2034年,三相開關穩壓器市場的需求將以8%的複合年成長率成長。這些穩壓器對於高負載應用至關重要,例如維持暖通空調系統、電梯和其他工業設備的不間斷運作。更嚴格的電能品質標準的採用推動了對三相穩壓器的需求。

2024年,美國商用開關穩壓器市場規模達6,550萬美元。由於政府扶持政策、技術進步以及對可靠配電系統日益成長的需求,預計該市場將大幅成長。資料中心、醫療保健基礎設施以及其他需要穩定高品質電力系統的關鍵產業的快速擴張,將在未來幾年進一步推動該市場的成長。

全球商用開關穩壓器市場的主要參與者包括西門子、英飛凌科技、微芯科技、亞德諾半導體和東芝電子元件及儲存設備株式會社等。這些公司專注於透過投資產品創新、建立策略合作夥伴關係和增強分銷管道來擴大市場佔有率。這使得他們能夠提供先進的解決方案,提高營運效率,並滿足對高性能穩壓器日益成長的需求。此外,許多公司正在投資人工智慧驅動的技術和智慧系統,以提供更自動化和可靠的穩壓解決方案,滿足電信、醫療保健和工業自動化等各行業不斷變化的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 戰略儀表板

- 策略舉措

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依階段,2021 - 2034

- 主要趨勢

- 單相

- 三相

第6章:市場規模及預測:按電壓,2021 - 2034

- 主要趨勢

- ≤40千伏安

- > 40 千伏安至 250 千伏安

- > 250千伏安

第7章:市場規模及預測:依地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 俄羅斯

- 英國

- 義大利

- 西班牙

- 荷蘭

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 馬來西亞

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 秘魯

- 阿根廷

第8章:公司簡介

- Analog Devices

- Bel Fuse

- Eaton

- Infineon Technologies

- Legrand

- MaxLinear

- Microchip Technology

- Minmax Technology

- Nisshinbo Micro Devices

- NXP Semiconductors

- Renesas Electronics Corporation

- ROHM

- SEMTECH

- Siemens

- STMicroelectronics

- SynQor

- TOREX SEMICONDUCTOR

- Toshiba Electronic Devices & Storage Corporation

- Vicor Corporation

- Vishay Intertechnology

The Global Switching Commercial Voltage Regulator Market was valued at USD 653.1 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 1.41 billion by 2034, driven by the increasing demand for precise protection of sensitive equipment, along with the rising importance of managing power quality. Technological advancements in AI-powered voltage stabilization technologies are expected to strengthen the industry. Additionally, the growing power consumption in commercial buildings and concerns about power surges contribute to the market's expansion. Integrating renewable energy sources such as wind and solar power into the grid spurs demand for advanced voltage regulation systems.

Governments worldwide are focusing on energy efficiency initiatives, which are further boosting the need for these devices to optimize power consumption and reduce operational costs. The continuous advancements in automated, reliable, and programmable digital systems are unlocking new growth opportunities in the commercial voltage regulator market. The increasing adoption of industrial automation, alongside the growth of data centers and telecommunication networks, is driving the demand for precise voltage regulation. As businesses rely more on digital infrastructure, the need for stable and accurate power systems to support critical operations is more important than ever, creating significant business opportunities for voltage regulators. With the continuous rise of these sectors, the demand for high-performance voltage regulation systems is expected to surge.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $653.1 Million |

| Forecast Value | $1.41 Billion |

| CAGR | 8.1% |

The market for ? 40 kVA switching commercial voltage regulator segment is projected to experience a robust growth rate of over 7.5% through 2034. These voltage regulators are crucial in protecting sensitive commercial equipment from voltage fluctuations, ensuring the operational reliability and longevity of electronics such as computers, point-of-sale systems, HVAC units, and lighting systems.

Similarly, the demand for three-phase switching voltage regulator segment is forecast to grow at a CAGR of 8% by 2034. These regulators are vital for high-load applications, such as maintaining the uninterrupted operation of HVAC systems, elevators, and other industrial equipment. Adopting stricter power quality standards drives the demand for three-phase voltage regulators.

United States Switching Commercial Voltage Regulator Market was valued at USD 65.5 million in 2024. It is expected to grow significantly due to supportive government policies, technological advancements, and the increasing need for reliable distribution systems. The rapid expansion of data centers, healthcare infrastructure, and other critical sectors that demand consistent and high-quality power systems will further fuel this market's growth in the coming years.

Key players in the Global Switching Commercial Voltage Regulator Market include Siemens, Infineon Technologies, Microchip Technology, Analog Devices, and Toshiba Electronic Devices & Storage Corporation, among others. Companies focus on expanding their market presence by investing in product innovation, forming strategic partnerships, and enhancing distribution channels. This allows them to offer advanced solutions, improve operational efficiencies, and meet the increasing demand for high-performance voltage regulators. Additionally, many of these companies are investing in AI-driven technologies and smart systems to offer more automated and reliable voltage regulation solutions, catering to the evolving needs of various industries such as telecommunications, healthcare, and industrial automation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 ≤ 40 kVA

- 6.3 > 40 kVA to 250 kVA

- 6.4 > 250 kVA

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 Analog Devices

- 8.2 Bel Fuse

- 8.3 Eaton

- 8.4 Infineon Technologies

- 8.5 Legrand

- 8.6 MaxLinear

- 8.7 Microchip Technology

- 8.8 Minmax Technology

- 8.9 Nisshinbo Micro Devices

- 8.10 NXP Semiconductors

- 8.11 Renesas Electronics Corporation

- 8.12 ROHM

- 8.13 SEMTECH

- 8.14 Siemens

- 8.15 STMicroelectronics

- 8.16 SynQor

- 8.17 TOREX SEMICONDUCTOR

- 8.18 Toshiba Electronic Devices & Storage Corporation

- 8.19 Vicor Corporation

- 8.20 Vishay Intertechnology

MEMS單模開關市場按裝置類型、連接埠配置、應用、最終用戶和波長分類,全球預測(2026-2032年)

MEMS單模開關市場按裝置類型、連接埠配置、應用、最終用戶和波長分類,全球預測(2026-2032年) 商用開關電壓調節器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、安裝類型、解決方案及部署方式分類

商用開關電壓調節器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、安裝類型、解決方案及部署方式分類 開關電源市場按類型、最終用戶和地區分類無風扇PC電源市場,按額定功率、外形規格、電源配置、應用和最終用戶分類,全球預測,2026-2032年

開關電源市場按類型、最終用戶和地區分類無風扇PC電源市場,按額定功率、外形規格、電源配置、應用和最終用戶分類,全球預測,2026-2032年 全球底盤安裝電阻器市場:績效與預測(2020-2031)

全球底盤安裝電阻器市場:績效與預測(2020-2031) 無風扇電源市場報告:趨勢、預測與競爭分析(至2031年)底盤安裝開關電源市場報告:2031 年趨勢、預測與競爭分析

無風扇電源市場報告:趨勢、預測與競爭分析(至2031年)底盤安裝開關電源市場報告:2031 年趨勢、預測與競爭分析