|

市場調查報告書

商品編碼

1755364

汽車動態稱重市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Weigh in Motion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

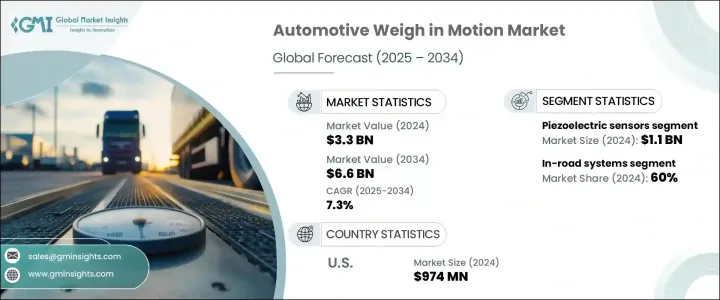

2024 年全球汽車動態稱重市場規模達 33 億美元,預計到 2034 年將以 7.3% 的複合年成長率成長,達到 66 億美元。這一成長趨勢得益於對智慧交通解決方案以及貨運走廊、收費站、高速公路和物流樞紐即時車輛重量追蹤需求的不斷成長。在不中斷交通的情況下進行精確、動態的車輛稱重的需求日益成長,這促使 WIM 技術得到廣泛應用。各國政府和交通部門擴大採用 WIM 系統來提高道路安全、延長道路使用壽命並確保遵守軸載法規。隨著人工智慧、先進感測器和即時資料分析的整合,WIM 系統在全球交通基礎設施中變得更加可靠、高效和智慧。

這些系統現已包含雲端整合、嵌入式攝影機、高速資料傳輸和遠端診斷功能,以簡化交通管理。物聯網感測器、預測性維護功能和數位孿生模擬的使用也重塑了基礎設施規劃。內建的防篡改、網路安全協定和合規性功能進一步支援安全且有效率的道路監控。這些創新使當局和商業營運商能夠降低成本、提高營運效率、減少交通中斷,同時改善城市和長途運輸路線的環境永續性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 33億美元 |

| 預測值 | 66億美元 |

| 複合年成長率 | 7.3% |

壓電感測器細分市場在2024年創收11億美元,成為全球車輛重量測量 (WIM) 市場領先的感測器類型。其廣泛應用源自於其高訊號靈敏度、緊湊的尺寸以及在高速公路速度下測量重量的能力。由於安裝簡便且維護需求極低,這些感測器成為交通部門的首選。它們在大規模部署中尤其有效,因為在大規模部署中,可擴展且經濟高效的系統至關重要。它們與現有道路基礎設施相容,並能夠支援交通資料應用、收費營運和貨運分析,這使得它們在智慧旅行項目中極具吸引力。

2024年,道路車輛重量監測系統佔據60%的市場佔有率,佔據市場主導地位。這些系統直接嵌入道路,提供持續、準確的重量資料,且不會造成交通阻塞。它們非常適合高流量通道、貨運路線和收費站。它們與智慧交通網路的無縫整合實現了自動化,提高了執法準確性,並提升了營運吞吐量。主管機關依靠道路車輛重量監測系統(WIM)進行高速車輛分類、即時合規性檢查和動態車輛評估,所有這些都無需人工干預。其低可見度和高性能使其成為道路基礎設施最佳化和監管執法的重要工具。

美國汽車動態稱重市場在 2024 年創造了 9.74 億美元的產值,預計到 2034 年的複合年成長率將達到 7.6%。美國大力推動基礎設施現代化和交通數位轉型,使其成為 WIM 應用的主要領導者。對維持道路品質、管理貨運量和遵守軸載合規規則的關注推動了全國先進重量監測系統的部署。美國擁有全球最廣泛的公路系統之一,並持續投資用於城市和農村貨運走廊的高精度 WIM 技術。在聯邦和州一級的資金支持、強大的 ITS 生態系統以及日益增多的數據驅動型交通政策舉措的支持下,美國市場仍然是下一代動態稱重平台創新和部署的重要樞紐。

汽車動態稱重市場的主要參與者包括 Intercomp、SWARCO AG、Kistler、Q-Free ASA、Kapsch TrafficCom、西門子交通、TE Connectivity、TDC Systems Ltd.、Econolite 和 International Road Dynamics。為了鞏固其在汽車動態稱重市場的地位,各公司正專注於持續創新,尤其是在人工智慧驅動的重量分析、感測器整合和智慧基礎設施相容性方面。對雲端連接、機器學習和邊緣運算的投資有助於實現即時診斷和自動車輛分類。各公司還提供可擴展的模組化系統,以滿足不同的道路狀況和交通密度。與交通部門和智慧城市規劃者的合作已成為拓展應用領域的關鍵。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按安裝量,2021 - 2034 年

- 主要趨勢

- 道路系統

- 重量橋系統

- 機載系統

第6章:市場估計與預測:按感測器,2021 - 2034 年

- 主要趨勢

- 壓電感測器

- 彎板

- 單一稱重感測器

- 其他

第7章:市場估計與預測:依車橋配置,2021 - 2034 年

- 主要趨勢

- 單軸

- 串聯軸

- 三軸

- 四軸

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 重量執行

- 交通資料收集

- 基於重量的收費

- 橋樑保護

- 工業車輛稱重

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 政府

- 運輸

- 私部門

- 其他

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Adient

- Applus

- Axis Communications

- Cestel

- Continental

- Econolite

- Efftronics Systems

- Golden River

- IAC Group

- Intercomp

- International Road Dynamics

- Kapsch TrafficCom

- Kasai Kogyo

- Q-Free ASA

- Siemens Mobility

- SWARCO AG

- TDC Systems

- TE Connectivity

- Wavetronix

- WIM Systems

The Global Automotive Weigh in Motion Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 6.6 billion by 2034. This upward trend is fueled by rising demand for intelligent traffic solutions and real-time vehicle weight tracking across freight corridors, toll booths, highways, and logistics hubs. The expanding need for accurate, dynamic vehicle weighing without halting traffic is leading to the widespread adoption of WIM technologies. Governments and transportation authorities are increasingly turning to WIM systems to boost road safety, extend road lifespans, and ensure compliance with axle-load regulations. With the integration of artificial intelligence, advanced sensors, and real-time data analytics, WIM systems are becoming more reliable, efficient, and intelligent across transportation infrastructures worldwide.

These systems now include cloud integration, embedded cameras, high-speed data transfer, and remote diagnostics to streamline traffic management. The use of IoT-powered sensors, predictive maintenance features, and digital twin simulations has also reshaped infrastructure planning. Built-in tamper resistance, cybersecurity protocols, and compliance features further support safe and efficient road monitoring. These innovations empower authorities and commercial operators to cut costs, enhance operational efficiency, and reduce traffic disruptions while improving environmental sustainability across both urban and long-haul transport routes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 billion |

| Forecast Value | $6.6 billion |

| CAGR | 7.3% |

The piezoelectric sensors segment generated USD 1.1 billion in 2024, making it the leading sensor type in the global WIM market. Their widespread use stems from their high signal sensitivity, compact size, and ability to measure weights at highway speeds. These sensors are a preferred choice for transportation authorities due to their straightforward installation process and minimal upkeep needs. They are particularly effective in large-scale deployments, where scalable and cost-efficient systems are essential. Their compatibility with existing road infrastructure, as well as their ability to support traffic data applications, toll operations, and freight analytics, makes them highly attractive in smart mobility projects.

In 2024, in-road systems led the market with a 60% share. These systems are directly embedded into roadways and provide continuous, accurate weight data without causing traffic delays. They are ideally suited for high-traffic corridors, freight transport routes, and toll stations. Their seamless integration into intelligent transportation networks enables automation, improves enforcement accuracy, and increases operational throughput. Authorities rely on in-road WIM systems to carry out high-speed vehicle classification, real-time compliance checks, and dynamic vehicle assessments, all without manual intervention. Their low visibility and high performance make them vital tools in road infrastructure optimization and regulatory enforcement.

U.S. Automotive Weigh in Motion Market generated USD 974 million in 2024 and is estimated to grow at a CAGR of 7.6% through 2034. The country's strong push toward infrastructure modernization and digital transformation in transportation has positioned it as a key leader in WIM adoption. The focus on preserving road quality, managing freight volumes, and adhering to axle-load compliance rules has driven nationwide deployments of advanced weight monitoring systems. With one of the most extensive highway systems globally, the U.S. continues to invest in high-precision WIM technology for both urban and rural freight corridors. Backed by federal and state-level funding, robust ITS ecosystems, and increasing data-driven transport policy initiatives, the U.S. market remains a key hub for innovation and deployment of next-gen weigh-in-motion platforms.

Key industry participants in the Automotive Weigh in Motion Market include Intercomp, SWARCO AG, Kistler, Q-Free ASA, Kapsch TrafficCom, Siemens Mobility, TE Connectivity, TDC Systems Ltd., Econolite, and International Road Dynamics. To enhance their position in the automotive weigh-in-motion market, companies are focusing on continuous innovation, particularly in AI-powered weight analytics, sensor integration, and smart infrastructure compatibility. Investments in cloud connectivity, machine learning, and edge computing help deliver real-time diagnostics and automated vehicle classification. Firms are also offering scalable modular systems to meet varying roadway conditions and traffic densities. Collaborations with transportation authorities and smart city planners have become central to expanding application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Installation

- 2.2.3 Sensor

- 2.2.4 Axle configuration

- 2.2.5 Application

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 In-road systems

- 5.3 Weight bridge systems

- 5.4 Onboard systems

Chapter 6 Market Estimates & Forecast, By Sensor, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Piezoelectric sensors

- 6.3 Bending plate

- 6.4 Single load cell

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Axle Configuration, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Single axle

- 7.3 Tandem axle

- 7.4 Triple axle

- 7.5 Quad axle

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Weight enforcement

- 8.3 Traffic data collection

- 8.4 Weight based tolling

- 8.5 Bridge protection

- 8.6 Industrial truck weighing

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Government

- 9.3 Transportation

- 9.4 Private sector

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Adient

- 11.2 Applus

- 11.3 Axis Communications

- 11.4 Cestel

- 11.5 Continental

- 11.6 Econolite

- 11.7 Efftronics Systems

- 11.8 Golden River

- 11.9 IAC Group

- 11.10 Intercomp

- 11.11 International Road Dynamics

- 11.12 Kapsch TrafficCom

- 11.13 Kasai Kogyo

- 11.14 Q-Free ASA

- 11.15 Siemens Mobility

- 11.16 SWARCO AG

- 11.17 TDC Systems

- 11.18 TE Connectivity

- 11.19 Wavetronix

- 11.20 WIM Systems