|

市場調查報告書

商品編碼

1755349

馬匹醫療保健市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Equine Healthcare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

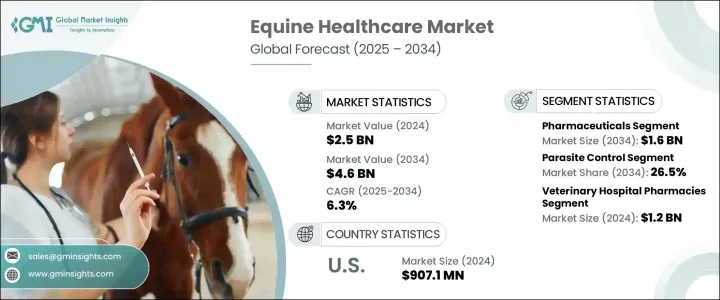

2024年,全球馬匹醫療保健市場規模達25億美元,預計到2034年將以6.3%的複合年成長率成長,達到46億美元。該市場的擴張主要歸因於動物醫療保健支出的增加,以及馬主、飼養員和獸醫對預防性護理和早期診斷的日益重視。這種意識的增強顯著增加了對馬匹醫療保健產品和服務的需求。肌肉骨骼疾病和馬匹傳染病的增加也推動了先進診斷和治療方法的採用。

此外,市場受益於對創新療法(例如再生藥物、標靶療法和數位健康監測工具)開發的持續關注。馬術運動和賽馬領域的投資不斷成長也推動了需求成長。隨著馬匹相關疾病發生率的上升,對更有效、更方便的治療方案的需求也日益成長。獸醫基礎設施的加強以及製藥公司對專有馬用藥物的持續投資,也在加速成長中發揮關鍵作用。馬匹領域寵物人性化的趨勢進一步促進了技術進步,並持續推動了對專為馬匹量身定做的現代醫療保健解決方案的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 25億美元 |

| 預測值 | 46億美元 |

| 複合年成長率 | 6.3% |

馬匹醫療保健是指透過預防、診斷和治療各種疾病來維持和改善馬匹健康的整體方法。市場涵蓋由獸醫、製藥公司和專業馬匹診所提供的各種醫療和診斷服務。這些解決方案確保用於育種、娛樂和運動的馬匹的整體健康和最佳表現。

就產品類別而言,全球馬匹保健市場細分為疫苗、藥品、診斷試劑、藥用飼料添加劑等。其中,藥品領域在2024年佔據市場主導地位,營收佔有率達8.179億美元,預計到2034年將達到16億美元,複合年成長率為6.6%。此領域產品包括抗感染藥、殺寄生蟲藥、消炎藥、止痛藥和其他藥物治療。這個領域佔據主導地位的原因是,針對呼吸道疾病、肌肉骨骼疾病和傳染病等常見馬匹疾病的先進療法的需求不斷成長。此外,休閒騎馬和競技賽事的參與度不斷提高,凸顯了對卓越健康管理方案的需求。

依適應症分類,市場分為寄生蟲控制、肌肉骨骼疾病、馬流感、馬腦脊髓炎、馬皰疹、西尼羅河病毒、破傷風等。寄生蟲控制細分市場在 2024 年佔據了 25.1% 的市場佔有率,預計到 2034 年將達到 26.5%。由於人們普遍需要控制危害馬匹健康和運動表現的有害寄生蟲,這一細分市場將繼續發揮關鍵作用。體內和體外寄生蟲會引發胃腸不適、皮毛退化和體重問題。馬匹飼養員和獸醫對預防性寄生蟲管理的認知不斷提高,這推動了對驅蟲藥和其他控制措施的需求。氣候變遷和全年均可進入牧場增加了人們接觸寄生蟲的機會,從而增加了對創新有效療法的需求。

按配銷通路分類,市場細分為獸醫院藥房、電商和其他管道。 2024年,獸醫院藥局佔據市場主導地位,估值達12億美元,預計2034年仍將維持領先地位,複合年成長率達6.7%。這些藥房因其全面的服務而備受青睞,包括專業諮詢、治療以及種類繁多的馬用藥物。其綜合的診療方法使其成為馬主獲取馬匹資訊的關鍵管道。

從區域來看,北美地區預計在預測期內的複合年成長率為 6.1%。該地區蓬勃發展的馬業、對動物福利的高度重視以及先進的獸醫基礎設施,使其成為馬匹醫療保健領域的領導者。龐大的馬匹數量和馬匹活動的廣泛參與進一步支撐了該地區對專業醫療保健服務的需求。

塑造全球馬匹保健市場的關鍵參與者包括赫斯卡公司 (Heska Corporation)、香奈兒製藥 (Chanelle Pharma)、詩華製藥 (Ceva)、碩騰 (Zoetis)、百勝 (Esaote)、奧特奇 (Alltech)、Vetoquinol、嘉吉 (Cargill)、德克本藥 (Dechra Pharmaceuticals)、愛德金托(Equal Pharma)、默克 (Merck)、Hallmarq Veterinary、勃林格殷格翰 (Boehringer Ingelheim) 和英泰辛 (Intacin)。這些公司積極參與產品創新、策略合作,並不斷擴展其產品組合,以滿足馬匹產業不斷變化的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 日益壯大的馬術運動與休閒活動

- 獸醫學技術進步

- 政府和公共組織對動物照護的支持不斷增加

- 產業陷阱與挑戰

- 缺乏熟練的獸醫專業人員

- 成長動力

- 成長潛力分析

- 技術格局

- 製藥業的管道分析

- 監管格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 疫苗

- 製藥

- 殺寄生蟲劑

- 抗感染

- 抗發炎鎮痛藥

- 其他醫藥產品

- 藥用飼料添加劑

- 診斷

- 其他產品

第6章:市場估計與預測:按適應症,2021 年至 2034 年

- 主要趨勢

- 肌肉骨骼疾病

- 寄生蟲控制

- 馬皰疹

- 馬腦脊髓炎

- 馬流感

- 破傷風

- 西尼羅病毒

- 其他適應症

第7章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 獸醫院藥房

- 電子商務

- 其他分銷管道

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Alltech

- Bentoii

- Boehringer Ingelheim

- Cargill

- Ceva

- Chanelle Pharma

- Dechra Pharmaceuticals

- Equal pharma

- Esaote

- Hallmarq Veterinary

- Heska Corporation

- IDEXX Laboratories

- Intacin

- Merck

- Vetoquinol

- Zoetis

The Global Equine Healthcare Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 4.6 billion by 2034. The expansion of this market is primarily attributed to rising animal healthcare spending and an increasing emphasis on preventive care and early diagnosis among horse owners, breeders, and veterinarians. This heightened awareness has significantly increased the demand for equine healthcare products and services. The rise in musculoskeletal disorders and equine infectious diseases has also driven the adoption of advanced diagnostics and treatments.

Furthermore, the market is benefiting from a continuous focus on developing innovative therapeutics such as regenerative medicines, targeted therapies, and digital health monitoring tools. Demand is also being propelled by growing investments in the equine sports and racing sectors. As the occurrence of equine-related diseases increases, so does the need for more effective and accessible treatment options. The strengthening of veterinary infrastructure and rising investments from pharmaceutical companies in proprietary equine medications are also playing a critical role in accelerating growth. The trend of pet humanization within the equine segment is further contributing to technological advancements and sustained demand for modern healthcare solutions tailored for horses.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 6.3% |

Equine healthcare refers to the holistic approach to maintaining and improving horse health through prevention, diagnosis, and treatment of various conditions. The market covers a wide range of medical and diagnostic offerings delivered by veterinarians, pharmaceutical firms, and dedicated equine clinics. These solutions ensure the overall wellness and peak performance of horses used in breeding, recreation, and sports.

In terms of product categories, the global equine healthcare market is segmented into vaccines, pharmaceuticals, diagnostics, medicinal feed additives, and others. Among these, the pharmaceuticals segment led the market in 2024 with a revenue share of USD 817.9 million and is expected to reach USD 1.6 billion by 2034, growing at a CAGR of 6.6%. This segment includes products such as anti-infectives, parasiticides, anti-inflammatories, analgesics, and other pharmaceutical treatments. The segment's dominance is driven by rising demand for advanced therapies targeting common equine conditions like respiratory, musculoskeletal, and infectious diseases. Moreover, the increased involvement in recreational riding and competitive events underscores the need for superior health management protocols.

The market by indication is categorized into parasite control, musculoskeletal disorders, equine influenza, equine encephalomyelitis, equine herpes, West Nile virus, tetanus, and others. The parasite control segment captured a 25.1% market share in 2024 and is forecasted to reach 26.5% by 2034. This segment continues to play a pivotal role due to the widespread need to manage harmful parasites that compromise a horse's health and performance. Internal and external parasites can trigger gastrointestinal distress, coat degradation, and weight issues. Rising awareness among horse caretakers and veterinarians around preventive parasite management is pushing the demand for anthelmintics and other control measures. Changing climatic patterns and year-round access to pasturelands have amplified exposure to parasites, boosting the need for innovative and effective therapeutics.

By distribution channel, the market is segmented into veterinary hospital pharmacies, e-commerce, and others. Veterinary hospital pharmacies dominated the market in 2024 with a valuation of USD 1.2 billion and are projected to maintain their lead through 2034, growing at a CAGR of 6.7%. These pharmacies are preferred due to their comprehensive services, which include professional consultation, treatment, and access to a wide variety of equine medications. Their integrated approach to diagnosis and therapy continues to make them a critical access point for horse owners.

Regionally, North America is projected to grow at a CAGR of 6.1% over the forecast period. The region's robust equine industry, heightened focus on animal welfare, and advanced veterinary infrastructure have positioned it as a leader in the equine healthcare space. A large horse population and widespread participation in equine activities further support the demand for specialized healthcare offerings across the region.

Key players shaping the global equine healthcare market include Heska Corporation, Chanelle Pharma, Ceva, Zoetis, Esaote, Alltech, Vetoquinol, Cargill, Dechra Pharmaceuticals, IDEXX Laboratories, Bentoii, Equal Pharma, Merck, Hallmarq Veterinary, Boehringer Ingelheim, and Intacin. These companies are actively involved in product innovation, strategic collaborations, and expanding their product portfolios to meet the evolving needs of the equine industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing equine sports and recreational activities

- 3.2.1.2 Technological advancements in veterinary medicine

- 3.2.1.3 Increasing support offered by government and public organizations for animal care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled veterinary professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pipeline analysis, by pharmaceuticals

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Gap Analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Vaccines

- 5.3 Pharmaceuticals

- 5.3.1 Parasiticides

- 5.3.2 Anti-infective

- 5.3.3 Anti-inflammatory and analgesics

- 5.3.4 Other pharmaceutical products

- 5.4 Medicinal feed additives

- 5.5 Diagnostics

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Musculoskeletal disorders

- 6.3 Parasite control

- 6.4 Equine herpes

- 6.5 Equine encephalomyelitis

- 6.6 Equine influenza

- 6.7 Tetanus

- 6.8 West Nile Virus

- 6.9 Other indications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospital pharmacies

- 7.3 E-commerce

- 7.4 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alltech

- 9.2 Bentoii

- 9.3 Boehringer Ingelheim

- 9.4 Cargill

- 9.5 Ceva

- 9.6 Chanelle Pharma

- 9.7 Dechra Pharmaceuticals

- 9.8 Equal pharma

- 9.9 Esaote

- 9.10 Hallmarq Veterinary

- 9.11 Heska Corporation

- 9.12 IDEXX Laboratories

- 9.13 Intacin

- 9.14 Merck

- 9.15 Vetoquinol

- 9.16 Zoetis

馬匹保健市場:按產品、適應症、分銷管道和地區分類(2026-2034 年)

馬匹保健市場:按產品、適應症、分銷管道和地區分類(2026-2034 年) 馬匹保健市場:依產品類型、疾病、給藥途徑及最終用戶分類-2026-2032年全球市場預測

馬匹保健市場:依產品類型、疾病、給藥途徑及最終用戶分類-2026-2032年全球市場預測 全球馬匹保健市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球馬匹保健市場規模、佔有率、趨勢和成長分析報告(2026-2034) 馬匹保健市場規模、佔有率和趨勢分析報告:按產品、適應症、活動、分銷管道、地區和細分市場分類(2026-2033 年)

馬匹保健市場規模、佔有率和趨勢分析報告:按產品、適應症、活動、分銷管道、地區和細分市場分類(2026-2033 年) 馬匹保健市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、形式、材質、設備和解決方案分類

馬匹保健市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、形式、材質、設備和解決方案分類 馬匹保健市場:依產品、適應症、用途、配銷通路、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測馬匹健康市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2025-2034)

馬匹保健市場:依產品、適應症、用途、配銷通路、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測馬匹健康市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2025-2034) 馬匹醫療保健市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、適應症、活動、配銷通路、地區和競爭細分,2020-2030 年

馬匹醫療保健市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、適應症、活動、配銷通路、地區和競爭細分,2020-2030 年 到 2030 年馬醫療保健市場預測:按產品類型、動物類型、疾病類型、分銷管道、最終用戶和地區進行的全球分析

到 2030 年馬醫療保健市場預測:按產品類型、動物類型、疾病類型、分銷管道、最終用戶和地區進行的全球分析 全球馬匹保健市場 2024-2031

全球馬匹保健市場 2024-2031