|

市場調查報告書

商品編碼

1755335

調味料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Seasoning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年,全球調味料市場規模達213億美元,預計到2034年將以5.7%的複合年成長率成長,達到371億美元。這主要得益於飲食習慣的改變、簡便食品的日益普及以及人們對提升食品風味日益成長的興趣。儘管全球經濟波動,但調味料的需求仍然強勁,因為它在已開發經濟體和新興經濟體的家庭廚房和商業食品行業中都扮演著不可或缺的角色。調味料不僅對風味至關重要,也對保持全球美食的原汁原味至關重要。

技術進步和全球化的不斷發展,拓寬了世界各地各種香草和香料的供應,催生了更複雜、更客製化的香料混合物。這些發展使得調味料能夠無縫融入包裝食品和即食食品領域。隨著城市化和國際美食的普及,調味料市場蓬勃發展。消費者對清潔標籤、天然和非基因改造產品表現出明顯的偏好,這促使企業在成分透明度和永續性方面不斷創新。除了烹飪用途外,對功能性食品日益成長的需求也進一步推動了富含健康益處的調味料產品的使用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 213億美元 |

| 預測值 | 371億美元 |

| 複合年成長率 | 5.7% |

2024年,以香料為基礎的調味品市場價值達113億美元,預計到2034年將以5.6%的複合年成長率成長。香料在食品製備中依然至關重要,因為它們能夠提升口感和營養價值。人們的健康意識不斷增強,全球各地對當地風味的熱愛也推動了香料在傳統菜餚和現代食譜中的廣泛應用。消費者對薑黃、辣椒、孜然和辣椒粉等香料的需求持續成長,不僅源自於其美味,也源自於其健康功效。香料的靈活使用方式——無論是整粒、研磨還是萃取物——也增強了其持久的吸引力。此外,電子商務和零售通路的蓬勃發展也使得香料的供應更加便利。

2024年,粉狀調味料市場規模達181億美元,佔市佔率的26.4%。由於其便利性和與各種食譜的兼容性,預計2025年至2034年期間的複合年成長率將達到5.5%。粉狀調味料質地均勻、易於儲存,使其在加工和包裝食品中具有顯著優勢,尤其在口味均勻和保存期限較長的加工和包裝食品中。消費者和製造商更青睞粉狀調味料,用於製作調味醬、湯品、醬汁、零食和餐盒。此外,這些調味料運輸和儲存成本低廉,也使其日益受歡迎。

美國調味料市場在2024年創收48億美元,預計2025年至2034年期間的複合年成長率將達到6%。該市場受益於國內消費旺盛、食品加工能力強勁以及向有機和天然食材的廣泛轉變。多元文化美食(尤其是亞洲、地中海和拉丁美洲的美食)日益流行,引發了人們對混合香料和民族風味組合的需求。同時,家庭烹飪、社群媒體影響力以及人們對美食烹飪的興趣也隨之激增。低鈉和無過敏原混合香料等注重健康的創新產品正成為關鍵賣點。這些發展勢頭使美國成為全球調味料行業的領導者。

活躍於全球調味料市場的公司包括:奇華頓公司 (Givaudan SA)、奧蘭國際 (Olam International)、味好美公司 (McCormick & Company, Inc.)、嘉里集團 (Kerry Group plc) 和味之素株式會社 (Ajinomoto Co., Inc.)。為了鞏固和擴大市場佔有率,調味料行業的公司正在實施有針對性的策略。許多公司正在推出文化多元化的混合香料和更健康的替代品,以滿足清潔標籤的需求。產品創新是核心-各大品牌正在推出兼顧風味和健康的香料配方,例如低鈉和無防腐劑的選擇。進軍電商領域使公司能夠觸及更廣泛的消費者群體,同時提供可客製化的包裝和基於訂閱的香料套裝。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 對民族和異國美食的需求不斷成長

- 消費者對美食烹飪的興趣日益濃厚

- 消費者對清潔標籤產品的偏好日益增加

- 食品服務業的成長

- 產業陷阱與挑戰

- 原物料價格波動

- 食品添加物的嚴格監管

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- Pestel 分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)

(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 草藥

- 羅勒

- 牛至

- 百里香

- 迷迭香

- 香菜

- 其他

- 香料

- 胡椒

- 肉桂

- 孜然

- 薑黃

- 小荳蔻

- 丁香

- 其他

- 鹽和鹽替代品

- 食鹽

- 海鹽

- 喜馬拉雅鹽

- 低鈉鹽

- 其他

- 調味料混合物

- 義大利調味料

- 卡真調味料

- 咖哩粉

- 塔可調味料

- 咖哩粉

- 其他

- 其他

第6章:市場估計與預測:依形式,2021-2034

- 主要趨勢

- 粉末

- 完整/完好

- 粉碎/研磨

- 液體

- 貼上

- 其他

第7章:市場估計與預測:依性質,2021-2034

- 主要趨勢

- 傳統的

- 有機的

- 非基因改造

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 肉類和家禽

- 零食和簡便食品

- 湯、醬汁和調味品

- 烘焙和糖果

- 海鮮

- 冷凍食品

- 飲料

- 其他

第9章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 食品加工業

- 食品服務業

- 餐廳

- 飯店

- 咖啡廳

- 速食連鎖店

- 其他

- 零售/家居

第 10 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- B2B

- B2C

- 超市/大賣場

- 便利商店

- 專賣店

- 網路零售

- 其他

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Ajinomoto Co., Inc.

- Ariake Japan Co., Ltd.

- Baria Pepper

- British Pepper & Spice Co Ltd

- Dohler GmbH

- DS Group

- Everest Spices

- Firmenich SA

- Frontier Co-op

- Fuchs Gewurze GmbH

- Givaudan SA

- Kerry Group plc

- McCormick & Company, Inc.

- MDH Spices

- Nestle SA

- Olam International

- Sensient Technologies Corporation

- Symrise AG

- The Kraft Heinz Company

- Unilever PLC

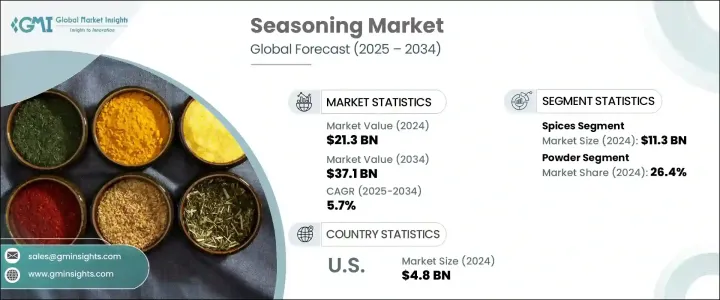

The Global Seasoning Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 37.1 billion by 2034, fueled by changing dietary habits, the rising popularity of convenient food products, and a heightened interest in enhancing food flavor. Despite fluctuations in the global economy, the demand for seasoning remains strong due to its indispensable role in household kitchens and the commercial food industry across developed and emerging economies. Seasonings have become integral not just for flavor but also for preserving authenticity in global cuisines.

Technological improvements and increasing globalization have broadened the availability of diverse herbs and spices worldwide, giving rise to more complex and tailored spice blends. These developments have enabled the seamless incorporation of seasonings into packaged and ready-to-eat food segments. As urbanization and exposure to international cuisines rise, the market thrives. Consumers are showing a clear preference for clean-label, natural, and non-GMO products, which is encouraging companies to innovate in ingredient transparency and sustainability. In addition to culinary uses, the increasing demand for functional foods further boosts the use of seasoning products enriched with health benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $37.1 Billion |

| CAGR | 5.7% |

The seasoning segment based on spices was valued at USD 11.3 billion in 2024 and is projected to grow at a CAGR of 5.6% through 2034. Spices remain vital in food preparation thanks to their role in enhancing both taste and nutritional value. Their widespread use in traditional dishes and contemporary recipes alike is driven by rising health consciousness and the global appreciation for regional flavors. Consumers continue to demand spices like turmeric, chili, cumin, and paprika not only for taste but for their wellness properties. The flexibility of using spices in different formats-whether whole, ground or as extracts-adds to their sustained appeal. Moreover, growing e-commerce and retail availability have made spices more accessible.

The powdered seasoning segment generated USD 18.1 billion in 2024, holding a 26.4% share, and is set to grow at a CAGR of 5.5% from 2025 to 2034 driven by the convenience and compatibility with a wide range of recipes. The consistent texture and ease of storage give powdered seasonings a significant edge, particularly in processed and packaged foods where uniform taste and longer shelf life are key. Consumers and manufacturers prefer powdered formats for applications in rubs, soups, sauces, snacks, and meal kits. Additionally, these seasonings are cost-effective to transport and store, contributing to their growing popularity.

U.S. Seasoning Market generated USD 4.8 billion in 2024 and is expected to grow at a CAGR of 6% from 2025 to 2034. The market benefits from high domestic consumption, strong food processing capabilities, and a widespread shift toward organic and natural ingredients. The growing popularity of multicultural cuisines-particularly those from Asia, the Mediterranean, and Latin America-has sparked increased demand for blended and ethnic spice combinations. Simultaneously, home cooking, social media influence, and interest in gourmet meal preparation have surged. Health-focused innovations, such as low-sodium and allergen-free spice blends, are becoming key selling points. These dynamics position the U.S. as a leader in the global seasoning industry.

Companies active in the Global Seasoning Market include: Givaudan SA, Olam International, McCormick & Company, Inc., Kerry Group plc, and Ajinomoto Co., Inc. To secure and expand their market footprint, companies in the seasoning industry are implementing targeted strategies. Many are introducing culturally diverse blends and healthier alternatives that cater to clean-label demands. Product innovation is central-brands are rolling out spice formulations that balance flavor and health, such as low-sodium and preservative-free options. Expansion into e-commerce has enabled companies to reach broader consumer segments while offering customizable packaging and subscription-based spice kits.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Product type

- 2.2.1.3 Form

- 2.2.1.4 Nature

- 2.2.1.5 Application

- 2.2.1.6 End use

- 2.2.1.7 Distribution channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for ethnic and exotic cuisines

- 3.2.1.2 Rising consumer interest in gourmet cooking

- 3.2.1.3 Increasing preference for clean label products

- 3.2.1.4 Growth in the food service industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Stringent regulations on food additives

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Herbs

- 5.2.1 Basil

- 5.2.2 Oregano

- 5.2.3 Thyme

- 5.2.4 Rosemary

- 5.2.5 Parsley

- 5.2.6 Others

- 5.3 Spices

- 5.3.1 Pepper

- 5.3.2 Cinnamon

- 5.3.3 Cumin

- 5.3.4 Turmeric

- 5.3.5 Cardamom

- 5.3.6 Cloves

- 5.3.7 Others

- 5.4 Salt & salt substitutes

- 5.4.1 Table salt

- 5.4.2 Sea salt

- 5.4.3 Himalayan salt

- 5.4.4 Low-sodium salt

- 5.4.5 Others

- 5.5 Seasoning blends

- 5.5.1 Italian seasoning

- 5.5.2 Cajun seasoning

- 5.5.3 Curry powder

- 5.5.4 Taco seasoning

- 5.5.5 Garam masala

- 5.5.6 Others

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Whole/intact

- 6.4 Crushed/ground

- 6.5 Liquid

- 6.6 Paste

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Organic

- 7.4 Non-GMO

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Meat & Poultry

- 8.3 Snacks & convenience food

- 8.4 Soups, sauces & dressings

- 8.5 Bakery & confectionery

- 8.6 Seafood

- 8.7 Frozen foods

- 8.8 Beverages

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food processing industry

- 9.3 Food service industry

- 9.3.1 Restaurants

- 9.3.2 Hotels

- 9.3.3 Cafes

- 9.3.4 Fast food chains

- 9.3.5 Others

- 9.4 Retail/household

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 B2B

- 10.3 B2C

- 10.3.1 Supermarkets/hypermarkets

- 10.3.2 Convenience stores

- 10.3.3 Specialty stores

- 10.3.4 Online retail

- 10.3.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Ajinomoto Co., Inc.

- 12.2 Ariake Japan Co., Ltd.

- 12.3 Baria Pepper

- 12.4 British Pepper & Spice Co Ltd

- 12.5 Dohler GmbH

- 12.6 DS Group

- 12.7 Everest Spices

- 12.8 Firmenich SA

- 12.9 Frontier Co-op

- 12.10 Fuchs Gewurze GmbH

- 12.11 Givaudan SA

- 12.12 Kerry Group plc

- 12.13 McCormick & Company, Inc.

- 12.14 MDH Spices

- 12.15 Nestle S.A.

- 12.16 Olam International

- 12.17 Sensient Technologies Corporation

- 12.18 Symrise AG

- 12.19 The Kraft Heinz Company

- 12.20 Unilever PLC

調味料市場報告:趨勢、預測和競爭分析(至2035年)

調味料市場報告:趨勢、預測和競爭分析(至2035年) 燒烤調味料市場:依產品、銷售管道和地區分類

燒烤調味料市場:依產品、銷售管道和地區分類 燒烤調味料市場規模、佔有率、成長和全球行業分析:按類型、應用和地區分類,並對 2026-2034 年進行洞察和預測。

燒烤調味料市場規模、佔有率、成長和全球行業分析:按類型、應用和地區分類,並對 2026-2034 年進行洞察和預測。 燒烤調味料市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、地區和競爭格局分類,2021-2031年

燒烤調味料市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、銷售管道、地區和競爭格局分類,2021-2031年 燒烤調味品市場規模、佔有率和成長分析(按類型、分銷管道和地區分類)—產業預測(2026-2033 年)

燒烤調味品市場規模、佔有率和成長分析(按類型、分銷管道和地區分類)—產業預測(2026-2033 年) 全球燒烤調味料市場

全球燒烤調味料市場 調味料混合物和醃料市場規模及預測 2021-2031、全球及地區佔有率、趨勢和成長機會分析報告範圍:按最終用途、按產品類型分類的食品服務、按食品服務管道和地理分類卡真調味料的全球市場

調味料混合物和醃料市場規模及預測 2021-2031、全球及地區佔有率、趨勢和成長機會分析報告範圍:按最終用途、按產品類型分類的食品服務、按食品服務管道和地理分類卡真調味料的全球市場 調味料混合市場,規模,佔有率,趨勢,產業分析報告:各產品,各用途,不同形態,各地區,2025年~2034年的市場預測

調味料混合市場,規模,佔有率,趨勢,產業分析報告:各產品,各用途,不同形態,各地區,2025年~2034年的市場預測