|

市場調查報告書

商品編碼

1755295

血液透析血管移植市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hemodialysis Vascular Grafts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

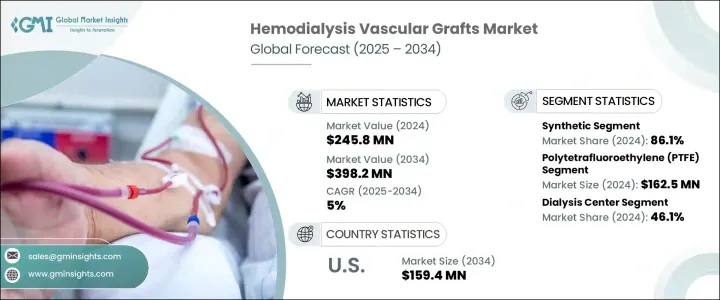

2024年全球血液透析血管移植物市場規模達2.458億美元,預計2034年將以5%的複合年成長率成長至3.982億美元。這些醫療器材在為接受血液透析的患者,尤其是不適合動靜脈瘻管的末期腎病變 (ESRD) 患者提供血管通路方面發揮著至關重要的作用。由於糖尿病、高血壓和人口老化,全球ESRD負擔日益加重,導致血液透析治療的需求不斷成長。此外,移植物技術的創新,例如生物工程和混合材料的開發,正在提高這些移植物耐久性、柔韌性和生物相容性,從而減少併發症,延長移植物通暢時間,並在已開發市場和新興市場得到更廣泛的臨床應用。

慢性腎病 (CKD) 和末期腎病 (ESRD) 的發生率上升與全球人口老化息息相關。老年患者通常血管通路有限,更依賴合成或生物血管移植物,這進一步推動了對基於移植物透析的需求。發展中國家透析中心的成長,以及醫療服務可近性的提高,正在提高血管移植物的應用率。政府的舉措和對腎臟護理的持續投入,也有助於使先進的移植技術更加經濟實惠、更容易獲得,從而支持全球腎臟醫療基礎設施的成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.458億美元 |

| 預測值 | 3.982億美元 |

| 複合年成長率 | 5% |

2024年,合成移植物市場佔據主導地位,佔據86.1%的顯著佔有率。合成血液透析移植物可立即使用,而動靜脈瘻管則需要數週才能成熟。這種即時可用性使其成為急性或緊急透析情況下的必需品。此外,膨體聚四氟乙烯(ePTFE)和聚氨酯等合成材料提高了這些移植物的性能、柔韌性和耐用性。表面處理和肝素塗層降低了血栓形成和感染的風險,使合成移植物在長期透析治療中更有效。隨著緊急血液透析需求的不斷成長,尤其是在醫院和急診環境中,合成移植物的應用也隨之增加,因為它們成熟時間更短,通常比生物移植物更受歡迎。

透析中心細分市場在2024年的市佔率為46.1%。全球慢性腎臟病和末期腎病病例的增加刺激了透析中心的快速發展。隨著這些設施的擴建以容納更多患者,對血液透析移植物等血管通路解決方案的需求也在增加。高容量透析中心需要提供患者可靠、有效的血管通路選擇。合成血液透析移植物與動靜脈瘻管相比,成熟時間較短,在這些情況下尤其有益,使其成為首選方案。因此,透析中心經常儲備合成移植物,促進了該細分市場的成長。

2034年,美國血液透析血管移植市場規模將達到1.594億美元。美國糖尿病和高血壓的盛行率很高,而這兩種疾病是導致慢性腎臟病和末期腎病的主要原因。這些疾病的發生率不斷上升意味著更多患者需要長期透析,從而推動了對血管通路解決方案的需求。聯邦醫療保險(Medicare)和其他聯邦醫療保健計劃為透析治療和血管通路手術提供全面的覆蓋,這使得患者更容易獲得血液透析血管移植。這些報銷政策激勵醫療保健提供者採用先進的移植技術,進一步推動市場成長。

全球血液透析血管移植物產業的主要市場參與者包括 Artivion、Becton Dickinson and Company、BIOVIC、Cook Medical、CryoLife、Getinge、Laminate Medical Technologies、LeMaitre、Merit Medical Systems、ParaGen Technologies、Proteon Therapeutics、Terumo & Medical、Vascudyne、Vascular Geneore、Vascular Genesis 和 WL Gam & Medicalore、Vascudyne、Vascular Geneore、Vascular Geneore 和 WL Gam & Medicalore, Vascular。血液透析血管移植物市場的公司正在採用多種關鍵策略來提升其市場地位。這些策略包括大力投資研發,以提高移植物的性能、生物相容性和使用壽命。製造商也致力於透過引入先進材料和混合移植物來擴展其產品組合,以滿足患者的多樣化需求。與醫療保健提供者、醫院和透析中心的合作正在幫助公司滲透新市場並提高產品的可及性。為了進一步鞏固立足點,公司正在透過進入透析服務需求不斷成長的新興市場來擴大其地域覆蓋範圍。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 末期腎病(ESRD)盛行率上升

- 移植材料和技術的進步

- 老年人口不斷增加

- 擴大醫療基礎設施和透析中心

- 產業陷阱與挑戰

- 血管移植手術和設備成本高昂

- 感染、血栓形成和移植失敗等併發症的風險

- 成長動力

- 成長潛力分析

- 技術格局

- 未來市場趨勢

- 監管格局

- 差距分析

- 專利分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 競爭市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 合成的

- 生物

第6章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 聚四氟乙烯(PTFE)

- 聚氨酯

- 聚酯纖維

- 生物

- 混合

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 透析中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Artivion

- Becton Dickinson and Company

- BIOVIC

- Cook Medical

- CryoLife

- Getinge

- Laminate Medical Technologies

- LeMaitre

- Merit Medical Systems

- ParaGen Technologies

- Proteon Therapeutics

- Terumo Medical

- Vascudyne

- Vascular Genesis

- WL Gore & Associates

The Global Hemodialysis Vascular Grafts Market was valued at USD 245.8 million in 2024 and is estimated to grow at a CAGR of 5% to reach USD 398.2 million by 2034. These medical devices play a vital role in providing vascular access for patients undergoing hemodialysis, particularly those with end-stage renal disease (ESRD) who are not suitable candidates for arteriovenous fistulas. The increasing global burden of ESRD, driven by diabetes, hypertension, and aging populations, is contributing to a growing need for hemodialysis treatments. Moreover, innovations in graft technology, such as the development of bioengineered and hybrid materials, are enhancing the durability, flexibility, and biocompatibility of these grafts, which results in fewer complications, prolonged graft patency, and broader clinical adoption in both developed and emerging markets.

The rise in chronic kidney disease (CKD) and ESRD correlates with an aging global population. Elderly patients, who often have limited vascular access, rely more on synthetic or biological vascular grafts, further boosting the demand for graft-based dialysis access. The growth of dialysis centers in developing countries, along with enhanced healthcare service access, is increasing the utilization of vascular grafts. Government initiatives and rising investments in renal care also contribute to making advanced graft technologies more affordable and accessible, supporting global growth in renal healthcare infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $245.8 Million |

| Forecast Value | $398.2 Million |

| CAGR | 5% |

In 2024, the synthetic graft segment led the market with a significant share of 86.1%. Synthetic hemodialysis grafts offer immediate use, unlike arteriovenous fistulas, which require weeks for maturation. This immediate availability makes synthetic grafts essential for acute or emergency dialysis situations. Furthermore, synthetic materials such as expanded polytetrafluoroethylene (ePTFE) and polyurethane have improved the performance, flexibility, and durability of these grafts. Surface treatments and heparin-bonded coatings reduce the risk of thrombosis and infection, making synthetic grafts more effective for long-term dialysis therapies. The growing demand for emergency hemodialysis access, especially in hospitals and emergency settings, is increasing the adoption of synthetic grafts, which have shorter maturation times and are often preferred over their biological counterparts.

The dialysis centers segment held a 46.1% share in 2024. The rise in chronic kidney disease and end-stage renal disease cases worldwide has spurred the rapid growth of dialysis centers. As these facilities expand to accommodate more patients, the demand for vascular access solutions such as hemodialysis grafts increases. High-volume dialysis centers require reliable, effective vascular access options for their patients. Synthetic hemodialysis grafts, with their shorter maturation times compared to arteriovenous fistulas, are particularly beneficial in these settings, making them a preferred option. As a result, dialysis centers are frequently stocking synthetic grafts, contributing to the segment's growth.

U.S. Hemodialysis Vascular Grafts Market will reach USD 159.4 million by 2034. The U.S. faces a high prevalence of diabetes and hypertension, which are leading causes of chronic kidney disease and end-stage renal disease. The increasing incidence of these conditions means more patients require long-term dialysis, thereby driving demand for vascular access solutions. Medicare and other federal healthcare programs offer comprehensive coverage for dialysis treatments and vascular access procedures, which makes hemodialysis grafts more accessible to patients. These reimbursement policies incentivize healthcare providers to adopt advanced graft technologies, further fueling the market's growth.

Key market players in the Global Hemodialysis Vascular Grafts Industry include Artivion, Becton Dickinson and Company, BIOVIC, Cook Medical, CryoLife, Getinge, Laminate Medical Technologies, LeMaitre, Merit Medical Systems, ParaGen Technologies, Proteon Therapeutics, Terumo Medical, Vascudyne, Vascular Genesis, and W.L. Gore & Associates. Companies in the hemodialysis vascular grafts market are employing several key strategies to enhance their market position. These strategies include significant investments in research and development to improve graft performance, biocompatibility, and longevity. Manufacturers are also focusing on expanding their product portfolios by introducing advanced materials and hybrid grafts to meet the diverse needs of patients. Collaborations with healthcare providers, hospitals, and dialysis centers are helping companies penetrate new markets and improve product accessibility. To further strengthen their foothold, companies are increasing their geographic reach by entering emerging markets with growing demand for dialysis services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of end-stage renal disease (ESRD)

- 3.2.1.2 Advancements in graft materials and technology

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Expanding healthcare infrastructure and dialysis centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of vascular graft procedures and devices

- 3.2.2.2 Risk of complications such as infections, thrombosis, and graft failure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Biological

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polytetrafluoroethylene (PTFE)

- 6.3 Polyurethane

- 6.4 Polyester

- 6.5 Biological

- 6.6 Hybrid

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Dialysis centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Artivion

- 9.2 Becton Dickinson and Company

- 9.3 BIOVIC

- 9.4 Cook Medical

- 9.5 CryoLife

- 9.6 Getinge

- 9.7 Laminate Medical Technologies

- 9.8 LeMaitre

- 9.9 Merit Medical Systems

- 9.10 ParaGen Technologies

- 9.11 Proteon Therapeutics

- 9.12 Terumo Medical

- 9.13 Vascudyne

- 9.14 Vascular Genesis

- 9.15 W L Gore & Associates

血管移植物市場報告:按產品、原料、應用、最終用戶和地區分類(2026-2034 年)

血管移植物市場報告:按產品、原料、應用、最終用戶和地區分類(2026-2034 年) 血管移植物市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年

血管移植物市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年 血管移植物市場:2026-2032年全球市場預測(依產品類型、血管直徑、適應症、最終用戶及通路分類)

血管移植物市場:2026-2032年全球市場預測(依產品類型、血管直徑、適應症、最終用戶及通路分類) 2026年全球人造皮膚市場報告2026年全球血管移植市場報告

2026年全球人造皮膚市場報告2026年全球血管移植市場報告 2026-2034年全球血液透析血管移植市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球血液透析血管移植市場規模、佔有率、趨勢和成長分析報告 血管移植物市場規模、佔有率和成長分析(按產品、原料、應用、最終用戶和地區分類)-2026-2033年產業預測

血管移植物市場規模、佔有率和成長分析(按產品、原料、應用、最終用戶和地區分類)-2026-2033年產業預測 血管移植市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)血管移植市場:2025-2030 年預測2021-2029年全球血管移植市場

血管移植市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)血管移植市場:2025-2030 年預測2021-2029年全球血管移植市場