|

市場調查報告書

商品編碼

1755273

飛機密封件市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Aircraft Seals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

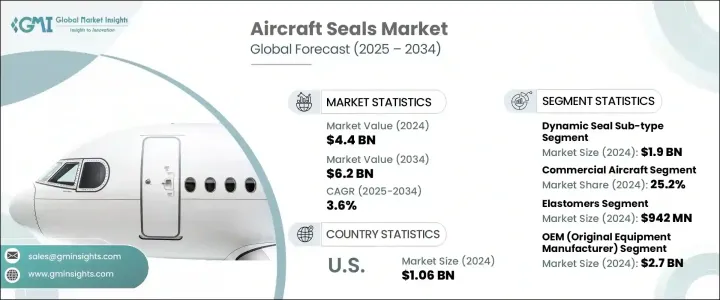

2024年,全球飛機密封件市場規模達44億美元,預計2034年將以3.6%的複合年成長率成長,達到62億美元。這主要得益於全球航空旅行需求的不斷成長,尤其是在亞太新興航空市場。航空運輸量的增加促使航空公司投資新飛機,直接刺激了對先進密封技術的需求。飛機製造商面臨著提高燃油效率和減少碳排放的壓力,這帶來了對輕量化、高性能密封的強烈需求。因此,製造商正在轉向高級彈性體和複合材料等先進材料。

此外,不斷變化的地緣政治格局和關稅法規也改變了供應鏈策略。貿易緊張局勢導致材料成本上升,迫使航太供應商轉向在地化採購,並重組採購流程以降低風險。這些轉變正在加強密封件的開發力度,使其不僅滿足性能標準,還能支持永續性和長期營運效率。彈性體材料的技術進步以及耐高溫耐壓密封件的開發,正在進一步塑造商用和國防領域飛機密封市場的發展軌跡。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 44億美元 |

| 預測值 | 62億美元 |

| 複合年成長率 | 3.6% |

2024年,動態密封件市場領先,估值達19億美元。它們在引擎組件、飛行控制系統和起落架等運動和受壓部件中發揮關鍵作用,使其成為現代飛機工程中不可或缺的一部分。動態密封件市場佔最大佔有率,得益於彈性體共混物的持續創新,這種共混物能夠承受極端條件,且不影響其功能性。

在各類飛機中,商用飛機在2024年的市佔率為25.2%。這一主導地位的形成歸因於越來越多的航空公司擴大機隊規模,以滿足客運需求並在定期維護週期內保持性能標準。密封件在引擎、環境控制和機身整合等關鍵系統中至關重要,這些系統需要耐用且可靠的零件。

2024年,美國飛機密封件市場規模達10.6億美元。憑藉其強大的航太基礎,美國仍然是全球市場的重要貢獻者。洛克希德馬丁、雷神索爾和波音等領先原始設備製造商的入駐,推動了對高階密封解決方案持續且高容量的需求。這些公司優先考慮精密零件,以最大限度地減少意外維護,並提高飛機在商用、國防和航太領域的可靠性。美國先進的研發生態系統和嚴格的監管標準也推動了密封技術的創新。

全球飛機密封件市場的主要領導者包括特瑞堡密封系統公司、派克漢尼汾公司和斯凱孚集團。各大公司專注於透過材料創新和精密製造技術擴展其產品組合。與航太原始設備製造商的策略合作使供應商能夠共同開發針對下一代飛機設計的客製化密封解決方案。許多公司在研發方面投入巨資,以提高密封件在極端溫度和壓力環境下的性能。向新興市場的擴張和製造本地化有助於降低物流成本並提高客戶親近度。此外,各公司還增強了售後服務,以在飛機的整個生命週期中獲取價值,並透過維護和升級確保長期收益。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 全球飛機機隊的擴張

- 飛機設計和材料的進步

- 混合動力和電力推進系統的興起

- 密封解決方案的技術創新

- 嚴格的監管標準和安全要求

- 產業陷阱與挑戰

- 材料和認證成本高

- 複雜的供應鏈和售後市場限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按密封類型,2021 - 2034 年

- 主要趨勢

- 動密封子類型

- 接觸式密封件

- 間隙密封件

- 其他

- 靜密封子類型

- O 型環和墊圈

- 其他密封件

- 防火密封

第6章:市場估計與預測:依飛機類型,2021 - 2034 年

- 主要趨勢

- 商用飛機

- 軍用機

- 公務機

- 直升機

- 無人機(無人駕駛飛行器)

- 其他

第7章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 彈性體

- 熱塑性塑膠

- 複合材料

- 金屬密封件

- 矽基材料

- 其他

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 機身

- 翅膀

- 引擎和引擎艙

- 飛行控制面

- 起落架

- 其他

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- OEM (原始設備製造商)

- MRO(維修、修理和大修)

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Bal Seal Engineering Inc.

- DuPont de Nemours, Inc.

- Eagle Industry Co., Ltd.

- Eaton Corporation plc

- Freudenberg Sealing Technologies

- Hutchinson SA

- International Seal Company Australia (ISCA) Pty Ltd

- Meggitt PLC

- Micro Seals

- Parker Hannifin Corporation

- Performance Sealing Inc.

- PPG Industries Inc.

- Precision Polymer Engineering

- Regal Rexnord Corporation

- Saint-Gobain SA

- SKF Group

- Sujan Industries

- Technetics Group

- Trelleborg Sealing Solutions

The Global Aircraft Seals Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 6.2 billion by 2034, driven by the growing global demand for air travel, particularly across emerging aviation markets in Asia-Pacific. This increased air traffic has prompted airline operators to invest in new aircraft, directly boosting demand for advanced sealing technologies. Aircraft manufacturers are under rising pressure to enhance fuel efficiency and reduce carbon emissions, creating a strong need for lightweight, high-performance seals. As a result, manufacturers are shifting toward advanced materials such as high-grade elastomers and composites.

Additionally, changing geopolitical dynamics and tariff regulations have altered supply chain strategies. Rising material costs due to trade tensions have pushed aerospace suppliers to pivot toward localized sourcing and restructure procurement processes to mitigate exposure. These shifts are reinforcing efforts to develop seals that not only meet performance standards but also support sustainability and long-term operational efficiency. Technological advancements in elastomeric materials and the development of seals with enhanced temperature and pressure resistance are further shaping the trajectory of the aircraft seals market across both commercial and defense segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 billion |

| Forecast Value | $6.2 billion |

| CAGR | 3.6% |

Dynamic seals led the market in 2024 with a valuation of USD 1.9 billion. Their critical role in components subject to movement and pressure, such as engine assemblies, flight control systems, and landing gear, makes them indispensable in modern aircraft engineering. The dynamic seal segment holds the largest share due to ongoing innovation in elastomer blends that can endure extreme conditions without compromising functionality.

Among aircraft types, the commercial aircraft segment accounted for a 25.2% share in 2024. This dominance is attributed to a rising number of airline operators expanding their fleets to meet passenger traffic demand and to maintain performance standards during regular maintenance cycles. Seals are essential in critical systems such as engines, environmental controls, and fuselage integration, which require long-lasting and reliable components.

U.S. Aircraft Seals Market was valued at USD 1.06 billion in 2024. The country remains a vital contributor to the global market due to its strong aerospace base. The presence of leading OEMs like Lockheed Martin, Raytheon, and Boeing fuels a consistent and high-volume demand for premium sealing solutions. These firms prioritize precision components that minimize unexpected maintenance and improve aircraft reliability across commercial, defense, and space applications. The advanced R&D ecosystem and stringent regulatory standards in the U.S. also drive innovation in sealing technologies.

Key players leading the Global Aircraft Seals Market include Trelleborg Sealing Solutions, Parker Hannifin Corporation, and SKF Group. Major companies focus on expanding their product portfolios through material innovation and precision manufacturing techniques. Strategic collaborations with aerospace OEMs enable suppliers to co-develop customized sealing solutions tailored to next-gen aircraft designs. Many invest heavily in R&D to enhance seal performance in extreme temperature and pressure environments. Expansion into emerging markets and localization of manufacturing are helping reduce logistical costs and improve customer proximity. Additionally, companies enhance their aftermarket services to capture value across the aircraft lifecycle, ensuring long-term revenue through maintenance and upgrades.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of global aircraft fleet

- 3.7.1.2 Advancements in aircraft design and materials

- 3.7.1.3 Rise of hybrid and electric propulsion systems

- 3.7.1.4 Technological innovations in sealing solutions

- 3.7.1.5 Stringent regulatory standards and safety requirements

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High material and certification costs

- 3.7.2.2 Complex supply chain and aftermarket constraints

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seal Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Dynamic seal sub-type

- 5.2.1 Contact seals

- 5.2.2 Clearance seals

- 5.2.3 Others

- 5.3 Static seal sub-type

- 5.3.1 O-Rings & gaskets

- 5.3.2 Other seals

- 5.4 Fire seals

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aircraft

- 6.3 Military aircraft

- 6.4 Business jets

- 6.5 Helicopters

- 6.6 UAVs (Unmanned Aerial Vehicles)

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Elastomers

- 7.3 Thermoplastics

- 7.4 Composite materials

- 7.5 Metal seals

- 7.6 Silicone-based materials

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Fuselage

- 8.3 Wings

- 8.4 Engine & nacelle

- 8.5 Flight control surfaces

- 8.6 Landing gear

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM (Original Equipment Manufacturer)

- 9.3 MRO (Maintenance, Repair, and Overhaul)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Bal Seal Engineering Inc.

- 11.2 DuPont de Nemours, Inc.

- 11.3 Eagle Industry Co., Ltd.

- 11.4 Eaton Corporation plc

- 11.5 Freudenberg Sealing Technologies

- 11.6 Hutchinson SA

- 11.7 International Seal Company Australia (ISCA) Pty Ltd

- 11.8 Meggitt PLC

- 11.9 Micro Seals

- 11.10 Parker Hannifin Corporation

- 11.11 Performance Sealing Inc.

- 11.12 PPG Industries Inc.

- 11.13 Precision Polymer Engineering

- 11.14 Regal Rexnord Corporation

- 11.15 Saint-Gobain S.A.

- 11.16 SKF Group

- 11.17 Sujan Industries

- 11.18 Technetics Group

- 11.19 Trelleborg Sealing Solutions

飛機密封件市場:按密封件類型、材質、形狀、應用和最終用戶分類-2026-2032年全球市場預測

飛機密封件市場:按密封件類型、材質、形狀、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球飛機密封件市場報告2026年全球飛機聚合物密封件市場報告

2026年全球飛機密封件市場報告2026年全球飛機聚合物密封件市場報告 飛機密封件市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、平台、地區和競爭對手分類,2021-2031年飛機聚合物密封件市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、應用類型、功能類型、地區和競爭格局分類,2021-2031年)

飛機密封件市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、平台、地區和競爭對手分類,2021-2031年飛機聚合物密封件市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、應用類型、功能類型、地區和競爭格局分類,2021-2031年) 飛機密封件市場規模、佔有率和成長分析(按應用、材料、類型、飛機類型、最終用途和地區分類)-產業預測,2026-2033年飛機擠壓密封件市場-全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、應用類型、地區和競爭格局分類,2020-2030年預測飛機製造密封件市場 - 全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、應用類型、運動類型、地區和競爭格局分類,2020-2030 年預測

飛機密封件市場規模、佔有率和成長分析(按應用、材料、類型、飛機類型、最終用途和地區分類)-產業預測,2026-2033年飛機擠壓密封件市場-全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、應用類型、地區和競爭格局分類,2020-2030年預測飛機製造密封件市場 - 全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、應用類型、運動類型、地區和競爭格局分類,2020-2030 年預測 飛機用密封的全球市場:各材料類型,各功能,各用途,各地區,機會,預測,2018年~2032年飛機用聚合物密封的全球市場:各材料,飛機類別,各應用領域,各地區,機會,預測,2018年~2032年

飛機用密封的全球市場:各材料類型,各功能,各用途,各地區,機會,預測,2018年~2032年飛機用聚合物密封的全球市場:各材料,飛機類別,各應用領域,各地區,機會,預測,2018年~2032年