|

市場調查報告書

商品編碼

1750626

電池測試設備市場機會、成長動力、產業趨勢分析及2025-2034年預測Battery Test Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

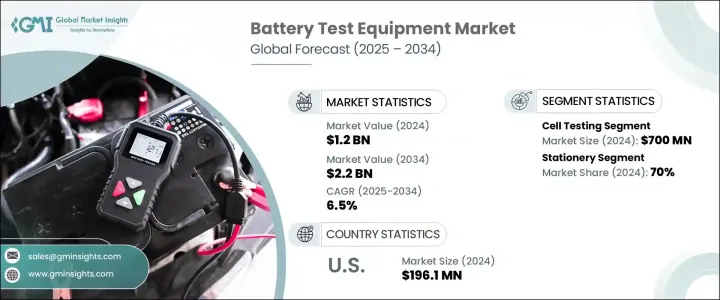

2024年,全球電池測試設備市場規模達12億美元,預計到2034年將以6.5%的複合年成長率成長,達到22億美元,這主要得益於電動車需求的不斷成長、再生能源基礎設施的進步以及智慧電子設備的成長。隨著電池系統日益複雜且性能要求越來越高,製造商越來越重視能夠確保電池耐用性、準確性和符合國際安全標準的測試工具。對電池健康、生命週期最佳化和預測性診斷的日益關注,使得測試設備成為各行各業的必備之物。自動化、資料分析和雲端平台的整合也正在改變傳統的測試工作流程。

這些智慧系統可實現即時監控、進階資料記錄和錯誤檢測,為製造商提供更快、更精準的洞察。隨著新型電池化學成分和架構的出現,對靈活、可擴展且智慧的測試解決方案的需求日益成長,這對於維護運輸、儲存和電子等領域的產品可靠性至關重要。這些現代化系統不僅提高了診斷的準確性,還縮短了測試週期,從而加快了創新電池技術的上市時間。它們能夠適應各種電池規格和配置,確保其在快速發展的能源格局中始終保持競爭力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 22億美元 |

| 複合年成長率 | 6.5% |

在功能性細分領域中,2024年,電池級測試佔據主導地位,市場規模達7億美元,因為在組裝成電池模組或電池組之前,需要對單個電池進行詳細分析,以檢測與能量容量、內阻和電壓一致性相關的問題。這種基礎評估在預防系統故障和提高營運效率方面發揮關鍵作用。隨著電池技術的快速發展,電池測試在確保產品壽命和安全性能方面比以往任何時候都更加重要。

從產品類型來看,固定式測試系統佔據了最大的市場佔有率,到2024年將達到70%。其卓越的精度、更長的測試時間以及管理複雜性能評估的能力使其成為涉及大規模儲能和重型電池組應用的理想選擇。在受控條件下進行全面分析的需求,使得固定式設備繼續成為致力於提供高性能能源解決方案的開發商、研究人員和電池製造商的首選。

美國電池測試設備市場在2024年創收1.961億美元,預計到2034年將以6.8%的複合年成長率成長,這得益於持續創新、清潔能源領域的擴張以及電池生產和測試基礎設施投資的不斷增加。政府的支持性政策和電動車的快速普及也加速了該地區對先進電池測試技術的需求。

為了鞏固市場地位,Chroma ATE、Arbin、NH Research、Midtronics 和 Neware Technology Limited 等公司正在實施以產品創新、全球擴張和協作為重點的策略性舉措。許多公司正在投資研發,以提高測試精度並支援不斷發展的電池化學技術。 Maccor 和 Bitrode 等公司正在推出可擴展的模組化測試平台,以滿足多樣化的客戶需求。此外,一些公司正在整合人工智慧驅動的分析和雲端連接,以提供智慧診斷工具。與研究機構和原始設備製造商 (OEM) 的合作以及客製化服務,也幫助這些公司在充滿活力、創新驅動的市場中獲得競爭優勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 組件提供者

- 製造商

- 技術提供者

- 配銷通路分析

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 對貿易的影響

- 技術與創新格局

- 專利分析

- 監管格局

- 成本細分分析

- 重要新聞和舉措

- 衝擊力

- 成長動力

- 充電電池需求不斷成長

- 電動車(EV)普及率的成長

- 擴大儲能系統

- 電池測試的技術進步

- 產業陷阱與挑戰

- 初始投資成本高

- 電池技術的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 固定式

- 便攜的

第6章:市場估計與預測:依功能,2021 - 2034 年

- 主要趨勢

- 電池測試

- 模組測試

- 包裝測試

第7章:市場估計與預測:按設備,2021 - 2034 年

- 主要趨勢

- 容量測試儀

- 安全檢測設備

- 溫度測試儀

- 電阻測試儀

- 電壓監視器

- 故障追蹤器

- 其他

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 汽車

- 消費性電子產品

- 能源和公用事業

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AMETEK

- Amprobe

- Arbin Instruments

- BatteryDAQ

- Bio-Logic Science

- Bitrode

- Cadex Electronics

- Chroma ATE

- Digatron Power Electronics

- FLIR Systems

- HIOKI EE

- ITECH Electronic

- Keysight Technologies

- Maccor

- Megger

- Midtronics

- Neware

- NH Research

- Pine Research

- Tenmars

The Global Battery Test Equipment Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 2.2 billion by 2034, driven by the rising demand for electric mobility, advancements in renewable energy infrastructure, and growth in smart electronic devices. As battery systems become more complex and performance-intensive, manufacturers are placing higher emphasis on testing tools that ensure battery durability, accuracy, and compliance with international safety standards. This rising focus on battery health, lifecycle optimization, and predictive diagnostics has made test equipment essential across industries. The integration of automation, data analytics, and cloud platforms is also transforming traditional testing workflows.

These intelligent systems allow for real-time monitoring, advanced data logging, and error detection, providing manufacturers with faster, more precise insights. As new battery chemistries and architectures emerge, the need for flexible, scalable, and smart testing solutions becomes increasingly critical in maintaining product reliability across sectors such as transportation, storage, and electronics. These modern systems not only improve the accuracy of diagnostics but also reduce testing cycle times, enabling quicker time-to-market for innovative battery technologies. Their adaptability to a wide range of cell formats and configurations ensures they remain relevant in a rapidly evolving energy landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 6.5% |

Among functional segments, testing at the cell level dominated in 2024, generating USD 700 million due to the need for detailed analysis of individual cells to detect issues related to energy capacity, internal resistance, and voltage consistency before assembly into battery modules or packs. Such foundational evaluation plays a pivotal role in preventing system-wide failures and improving operational efficiency. With the rapid evolution of battery technology, cell testing has become more crucial than ever in guaranteeing product longevity and safe performance.

From a product type perspective, stationary test systems held the largest share of the market, accounting for 70% in 2024. Their superior precision, longer testing capabilities, and ability to manage complex performance evaluations have made them ideal for applications involving large-scale energy storage and heavy-duty battery units. The need for comprehensive analysis under controlled conditions continues to make stationary equipment the preferred choice for developers, researchers, and battery manufacturers focused on delivering high-performance energy solutions.

United States Battery Test Equipment Market generated USD 196.1 million in 2024 and is projected to grow at a CAGR of 6.8% through 2034, driven by continuous innovation, expansion in the clean energy sector, and increasing investments in battery production and testing infrastructure. Supportive government policies and the rapid adoption of electric mobility have also accelerated the demand for advanced battery testing technologies across the region.

To strengthen their market position, companies like Chroma ATE, Arbin, NH Research, Midtronics, and Neware Technology Limited are pursuing strategic initiatives focused on product innovation, global expansion, and collaboration. Many are investing in R&D to enhance test precision and support evolving battery chemistry. Firms such as Maccor and Bitrode are launching scalable, modular testing platforms that address diverse customer needs. Additionally, several players are integrating AI-driven analytics and cloud connectivity to offer intelligent diagnostic tools. Partnerships with research institutes and OEMs, along with customized service offerings, are also helping these companies gain competitive advantages in a dynamic, innovation-driven market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for rechargeable batteries

- 3.8.1.2 Growth in electric vehicle (EV) adoption

- 3.8.1.3 Expansion of energy storage systems

- 3.8.1.4 Technological advancements in battery testing

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High Initial Investment Costs

- 3.8.2.2 Complexity of Battery Technologies

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Stationary

- 5.3 Portable

Chapter 6 Market Estimates & Forecast, By Function, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cell testing

- 6.3 Module testing

- 6.4 Pack testing

Chapter 7 Market Estimates & Forecast, By Equipment, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Capacity tester

- 7.3 Safety testing equipment

- 7.4 Temperature tester

- 7.5 Resistance tester

- 7.6 Voltage monitor

- 7.7 Fault tracker

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Energy and utility

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AMETEK

- 10.2 Amprobe

- 10.3 Arbin Instruments

- 10.4 BatteryDAQ

- 10.5 Bio-Logic Science

- 10.6 Bitrode

- 10.7 Cadex Electronics

- 10.8 Chroma ATE

- 10.9 Digatron Power Electronics

- 10.10 FLIR Systems

- 10.11 HIOKI E.E.

- 10.12 ITECH Electronic

- 10.13 Keysight Technologies

- 10.14 Maccor

- 10.15 Megger

- 10.16 Midtronics

- 10.17 Neware

- 10.18 NH Research

- 10.19 Pine Research

- 10.20 Tenmars

電池測試設備市場:按設備類型、電池類型、測試模式、技術、應用、最終用戶和銷售管道分類-2026-2032年全球預測汽車電池測試器市場:按測試方法、產品類型、技術、應用和最終用戶分類-2026-2032年全球預測高功率電池測試設備市場:依產品類型、技術、應用、最終用戶和分銷管道分類,全球預測,2026-2032年

電池測試設備市場:按設備類型、電池類型、測試模式、技術、應用、最終用戶和銷售管道分類-2026-2032年全球預測汽車電池測試器市場:按測試方法、產品類型、技術、應用和最終用戶分類-2026-2032年全球預測高功率電池測試設備市場:依產品類型、技術、應用、最終用戶和分銷管道分類,全球預測,2026-2032年 電池測試設備市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、最終用戶、功能

電池測試設備市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、最終用戶、功能 全球電池測試設備市場:市場規模、佔有率、成長、依類型和應用劃分的產業分析、區域洞察及預測(2026-2034)鋰測試服務市場(按服務類型、測試方法、應用、最終用戶產業和分銷管道分類),全球預測(2026-2032年)鋰離子電池檢測市場:按技術、檢測方法、設備類型、缺陷類型、檢測階段、外形規格和最終用戶分類,全球預測,2026-2032年

全球電池測試設備市場:市場規模、佔有率、成長、依類型和應用劃分的產業分析、區域洞察及預測(2026-2034)鋰測試服務市場(按服務類型、測試方法、應用、最終用戶產業和分銷管道分類),全球預測(2026-2032年)鋰離子電池檢測市場:按技術、檢測方法、設備類型、缺陷類型、檢測階段、外形規格和最終用戶分類,全球預測,2026-2032年 電池測試設備市場規模、佔有率和成長分析(按產品類型、測試類型、應用、電池類型和地區分類)-2026-2033年產業預測

電池測試設備市場規模、佔有率和成長分析(按產品類型、測試類型、應用、電池類型和地區分類)-2026-2033年產業預測 全球電池測試設備市場

全球電池測試設備市場 2025-2029年全球汽車電池測試儀市場

2025-2029年全球汽車電池測試儀市場