|

市場調查報告書

商品編碼

1750623

蜘蛛式升降機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Spider Lift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

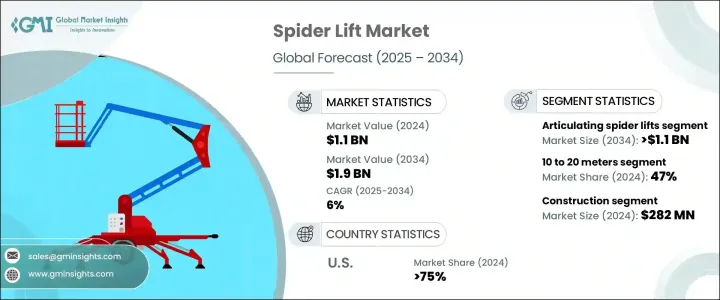

2024年,全球蜘蛛式升降機市場規模達11億美元,預計到2034年將以6%的複合年成長率成長,達到19億美元,這得益於物聯網整合、遠端資訊處理和自動化等技術的快速進步。這些創新技術能夠實現更精準的即時追蹤、預測性維護和簡化操作,從而提高效率和安全性。受日益嚴格的環境法規以及城市和室內應用對低排放設備需求的影響,混合動力和電動蜘蛛式升降機設計的發展勢頭日益強勁。

隨著建築工程對更高通行高度的要求越來越高,各行各業都在尋求能夠在複雜環境下兼顧提升和穩定性的解決方案,對長臂蜘蛛式升降機的需求也顯著成長。這些升降機如今已成為大型專案的關鍵組成部分,而傳統高空作業設備在這些專案中顯得力不從心,尤其是在高層建築維護、外部建築工程和公用設施安裝方面。長臂蜘蛛式升降機能夠在狹窄或難以觸及的區域作業,使其成為當今現代化施工現場不可或缺的工具。為了滿足這些需求,製造商專注於設計堅固耐用、靈活多變的升降機型號,在不影響安全性和易操作性的情況下提供更大的作業範圍。為了滿足不斷變化的監管環境,各公司正在整合智慧安全和監控系統,包括負載感測技術、自動控制和先進的遠端資訊處理等功能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 11億美元 |

| 預測值 | 19億美元 |

| 複合年成長率 | 6% |

鉸接式蜘蛛式升降機佔據了51%的市場佔有率,預計到2034年將創造11億美元的價值,其緊湊的設計、輕巧的構造以及跨行業的多功能性使其備受青睞。它們能夠在狹窄空間內通行並適應不平坦的地形,這使其在具有挑戰性的環境中更加重要。隨著製造商不斷改進型號以滿足獨特的應用需求,維護、安裝和城市公用事業項目的需求激增。其靈活的臂架和精確的機動性使其特別適合在交通不便的地區開展項目,而其便攜性使其能夠在各個場地高效部署。

2024年,平台高度在10公尺至20公尺之間的蜘蛛式升降機佔據了47%的市場佔有率,這得益於對可及性和移動性的平衡需求。這一高度範圍為園林綠化、輕型建築和公共設施維護等任務提供了理想的可用性。防滑平台、緊急下降系統和自動過載保護等增強型安全功能正在成為標準配置,幫助操作員在密集或高流量環境中更自信地工作。隨著工作場所安全法規的日益嚴格,這些功能正成為必不可少的要求。

美國蜘蛛式升降機市場規模達3.338億美元,佔2024年市場佔有率的75%,這得益於工業的快速發展、商業建築的激增以及基礎設施升級投資的增加。聯邦和州政府對永續發展的大力推動加速了向電動和混合動力蜘蛛式升降機的轉變,這些設備現場零排放,並且在敏感區域或室內區域運行更安靜。在北美,隨著各城市實施更嚴格的排放標準和噪音限制,承包商和租賃公司紛紛轉向電池供電或混合動力蜘蛛升降機。

塑造產業格局的關鍵參與者包括 CTE SpA、Dinolift、Platform Basket、Cela、山東托羅斯機械股份有限公司、奧什科甚集團、特雷克斯、Niftylift、Imer 和湖北高曼重工科技。領先企業正優先考慮策略合作夥伴關係和產品創新。許多公司在研發方面投入巨資,設計出配備先進控制系統的輕量化、緊湊型、環保車型。透過區域分銷網路和經銷商合作夥伴關係進行的全球擴張,正在幫助他們開拓新興市場。各公司也正在加強售後服務,並提供靈活的租賃和融資方案,以滿足租賃業務和大型車隊營運商的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原料和零件供應商

- 技術提供者

- 製成品

- 經銷商

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 策略產業反應

- 供應鏈重組

- 對貿易的影響

- 定價和產品策略

- 技術與創新格局

- 自動化和機器人技術

- 環保電力系統

- 物聯網與遠端資訊處理的整合

- 先進的控制系統與安全機制

- 專利分析

- 監管格局

- 用例

- 重要新聞和舉措

- 成本分解分析

- 首次購買

- 維護和維修

- 營運成本

- 運輸

- 折舊

- 價格趨勢分析

- 產品

- 地區

- 監管格局

- 對部隊的影響

- 成長動力

- 建築和基礎設施項目對高空作業平台的需求不斷成長

- 技術進步和安全性能的改進

- 工人安全法規意識不斷增強

- 租賃設備需求不斷成長

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 法規遵從性和安全標準

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 伸縮式蜘蛛升降機

- 鉸接式蜘蛛升降機

- 履帶式蜘蛛升降機

- 電動或混合動力蜘蛛式升降機

第6章:市場估計與預測:依平台高度,2021 - 2034 年

- 主要趨勢

- 10米以下

- 10至20米

- 20至25米

- 25米以上

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 政府

- 電信和公用事業

- 工業和製造公司

- 設施管理公司

- 租賃

- 娛樂和媒體製作

第8章:市場估計與預測:按地區,2021 - 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Airo

- Almac

- Cela

- CMC Lift

- CTE

- Dinolift

- Easy Lift

- Falcon Lift

- HINOWA

- Imer

- JLG Industries

- Niftylift

- Omme Lift

- Palazzani Industrie

- Platform Basket

- SHANDONG HIMOR MACHINERY

- Socageworld

- Teejan Equipment

- Terex Corporation

- Teupen

The Global Spider Lift Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 1.9 billion by 2034, driven by rapid technological advancements, including IoT integration, telematics, and automation. These innovations allow for better real-time tracking, predictive maintenance, and simplified operation, improving efficiency and safety. There is a growing momentum around hybrid and electric spider lift designs, influenced by increasingly stringent environmental regulations and the need for low-emission equipment in urban and indoor applications.

With construction projects requiring heights of greater access, longer-reach spider lifts are seeing a noticeable rise in demand as industries seek solutions that offer both elevation and stability in complex environments. These lifts are now a critical part of large-scale projects where conventional access equipment falls short, especially in high-rise maintenance, exterior building work, and utility installation. The ability of longer-reach spider lifts to operate in confined or difficult-to-reach areas makes them indispensable for today's modern job sites. In response to these needs, manufacturers focus on engineering robust and flexible lift models that offer greater reach without compromising safety or ease of operation. To meet the evolving regulatory landscape, companies are integrating intelligent safety and monitoring systems, including features like load-sensing technology, automated controls, and advanced telematics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 6% |

Articulating spider lifts segment held 51% share and is projected to generate USD 1.1 billion in value by 2034, favored by their compact design, lightweight build, and versatility across industries. Their ability to navigate narrow spaces and adapt to uneven terrain has increased their relevance in challenging environments. As manufacturers continue to refine models to meet unique application needs, demand has surged across maintenance, installation, and urban utility projects. Their flexible arms and precise maneuverability make them especially suitable for projects in areas with limited access, while their portability enables efficient deployment across sites.

Spider lifts with platform heights ranging from 10 to 20 meters held a 47% share in 2024, driven by the balanced need for reach and mobility. This height range offers ideal usability for tasks across landscaping, light construction, and public facility maintenance. Enhanced safety features such as anti-slip platforms, emergency descent systems, and automatic overload protection are becoming standard, helping operators work more confidently in dense or high-traffic environments. With stricter regulations around workplace safety, these features are becoming essential requirements.

United States Spider Lift Market generated USD 333.8 million, accounting for a 75% share in 2024, driven by rapid industrial development, a surge in commercial construction, and increased investments in infrastructure upgrades. The push for sustainability across federal and state levels accelerates the shift toward electric and hybrid spider lifts, which produce zero on-site emissions and operate more quietly in sensitive or indoor areas. In North America, contractors and rental companies turn to battery-powered or hybrid units as cities enforce stricter emissions standards and noise restrictions.

Key players shaping the industry include CTE SpA, Dinolift, Platform Basket, Cela, Shandong Toros Machinery Corporation, Oshkosh Corporation, Terex, Niftylift, Imer, and Hubei Goman Heavy Industry Technology. Leading companies are prioritizing strategic partnerships and product innovation. Many invest heavily in R&D to design lightweight, compact, eco-friendly models with advanced control systems. Global expansion through regional distribution networks and dealer partnerships is helping them tap into emerging markets. Companies are also enhancing after-sales services and offering flexible leasing and financing options to cater to rental businesses and large fleet operators.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material and component suppliers

- 3.1.1.2 Technology providers

- 3.1.1.3 Manufactures

- 3.1.1.4 Distributors

- 3.1.1.5 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Automation and robotics

- 3.4.2 Eco-Friendly power systems

- 3.4.3 Integration of IoT and telematics

- 3.4.4 Advanced control systems and safety mechanisms

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Cost break-down analysis

- 3.9.1 Initial purchase

- 3.9.2 Maintenance & repairs

- 3.9.3 Operational costs

- 3.9.4 Transportation

- 3.9.5 Depreciation

- 3.10 Price trend analysis

- 3.10.1 Product

- 3.10.2 Region

- 3.11 Regulatory landscape

- 3.12 Impact on forces

- 3.12.1 Growth drivers

- 3.12.1.1 Rising demand for aerial work platforms in construction and infrastructure projects

- 3.12.1.2 Technological advancements and improved safety features

- 3.12.1.3 Growing awareness of worker safety regulations

- 3.12.1.4 Growing demand for rental equipment

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 High initial investment and maintenance costs

- 3.12.2.2 Regulatory compliance and safety standards

- 3.12.1 Growth drivers

- 3.13 Growth potential analysis

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Telescopic spider lifts

- 5.3 Articulating spider lifts

- 5.4 Crawler-based spider lifts

- 5.5 Electric or hybrid spider lifts

Chapter 6 Market Estimates & Forecast, By Platform Height, 2021 - 2034 ($Mn Units)

- 6.1 Key trends

- 6.2 Below 10 meters

- 6.3 10 to 20 meters

- 6.4 20 to 25 meters

- 6.5 Above 25 meters

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Government

- 7.3 Telecommunications & utility

- 7.4 Industrial and manufacturing firms

- 7.5 Facility management companies

- 7.6 Rental

- 7.7 Entertainment & media production

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 North America

- 8.1.1 U.S.

- 8.1.2 Canada

- 8.2 Europe

- 8.2.1 UK

- 8.2.2 Germany

- 8.2.3 France

- 8.2.4 Italy

- 8.2.5 Spain

- 8.2.6 Russia

- 8.3 Asia Pacific

- 8.3.1 China

- 8.3.2 India

- 8.3.3 Japan

- 8.3.4 Australia

- 8.3.5 South Korea

- 8.3.6 Southeast Asia

- 8.4 Latin America

- 8.4.1 Brazil

- 8.4.2 Mexico

- 8.4.3 Argentina

- 8.5 MEA

- 8.5.1 South Africa

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

Chapter 9 Company Profiles

- 9.1 Airo

- 9.2 Almac

- 9.3 Cela

- 9.4 CMC Lift

- 9.5 CTE

- 9.6 Dinolift

- 9.7 Easy Lift

- 9.8 Falcon Lift

- 9.9 HINOWA

- 9.10 Imer

- 9.11 JLG Industries

- 9.12 Niftylift

- 9.13 Omme Lift

- 9.14 Palazzani Industrie

- 9.15 Platform Basket

- 9.16 SHANDONG HIMOR MACHINERY

- 9.17 Socageworld

- 9.18 Teejan Equipment

- 9.19 Terex Corporation

- 9.20 Teupen

2025年堆高機全球市場報告2025年全球電動堆高機市場報告

2025年堆高機全球市場報告2025年全球電動堆高機市場報告 全球堆高機市場

全球堆高機市場 全球卡車和堆高機市場 - 2025 年至 2030 年預測

全球卡車和堆高機市場 - 2025 年至 2030 年預測 堆高機市場-全球產業規模、佔有率、趨勢、機會及預測(依動力源、類別、最終用途、地區及競爭情況分類,2020-2030 年預測)堆高機座椅市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(機械懸浮座椅、空氣懸浮座椅)、按應用(小型堆高機、貨櫃堆高機)、按地區和競爭細分,2020-2030 年

堆高機市場-全球產業規模、佔有率、趨勢、機會及預測(依動力源、類別、最終用途、地區及競爭情況分類,2020-2030 年預測)堆高機座椅市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(機械懸浮座椅、空氣懸浮座椅)、按應用(小型堆高機、貨櫃堆高機)、按地區和競爭細分,2020-2030 年 日本堆高機市場規模、佔有率、趨勢及預測(按產品類型、技術、類別、應用和地區),2025 年至 2033 年窄通道卡車(VNA卡車)市場機會、成長動力、產業趨勢分析及2025年至2034年預測全球氫燃料電池堆高機市場規模(按燃料電池功率、起重能力、最終用戶、區域覆蓋範圍和預測)全球窄通道卡車(VNA卡車)市場:市場規模(按類型、應用和地區)、未來預測

日本堆高機市場規模、佔有率、趨勢及預測(按產品類型、技術、類別、應用和地區),2025 年至 2033 年窄通道卡車(VNA卡車)市場機會、成長動力、產業趨勢分析及2025年至2034年預測全球氫燃料電池堆高機市場規模(按燃料電池功率、起重能力、最終用戶、區域覆蓋範圍和預測)全球窄通道卡車(VNA卡車)市場:市場規模(按類型、應用和地區)、未來預測