|

市場調查報告書

商品編碼

1750620

救護車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Ambulance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

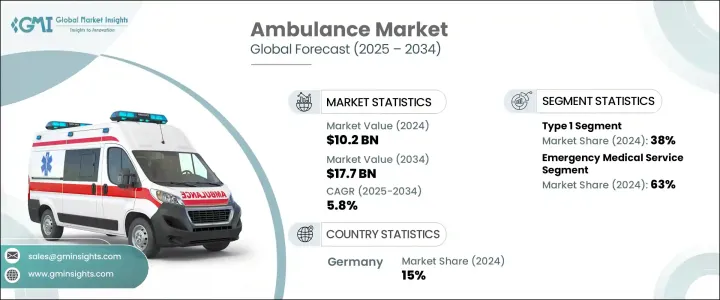

2024年,全球救護車市場規模達102億美元,預計到2034年將以5.8%的複合年成長率成長,達到177億美元,這得益於醫療保健支出的成長和緊急醫療服務(EMS)日益成長的重要性。政府和私營部門正在大力投資擴充救護車隊、縮短反應時間並升級醫療技術。這些投資有助於確保救護車能夠更好地應對緊急情況,並改善轉運過程中的病患照護。因此,越來越多的救護車配備了先進的醫療設備,例如呼吸機、自動心肺復甦裝置和先進的除顫器,以便在轉運過程中處理危重病情。

對氣道管理和呼吸器日益成長的重視進一步支撐了救護車市場的成長。呼吸器對於穩定呼吸窘迫患者病情至關重要,確保在心臟驟停或嚴重創傷等緊急情況下有效輸送氧氣。這些設備具有可調節壓力和容量控制等先進功能,可幫助醫護人員在前往醫療機構的途中提供重症監護。隨著越來越多的醫療系統認知到高品質急救服務的價值,對裝備更精良、更專業的救護車的需求持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 102億美元 |

| 預測值 | 177億美元 |

| 複合年成長率 | 5.8% |

2024年,1型救護車佔據市場主導地位,佔38%。這類車輛通常採用卡車底盤,為醫療設備和人員提供耐用的平台和額外的空間。 1型救護車日益受到青睞,是因為它們能夠應對緊急情況,包括大型事故或自然災害,並且能夠運送多名患者或大型設備。

2024年,緊急醫療服務(EMS)領域佔據63%的市場佔有率,這得益於醫療服務提供者優先考慮快速、可靠地轉運重症患者。遠距醫療和行動醫療解決方案的進步進一步提升了緊急醫療服務(EMS)的能力,使護理人員能夠遠端諮詢醫生,並在患者抵達醫院之前最佳化護理方案。這些創新預計將增加對更先進的救護車的需求,這些救護車能夠在轉運過程中提供更遠距離、更高品質的護理。

2024年,德國救護車市場佔了15%的市場佔有率,這得益於強力的監管支持,包括對環境永續性的支持以及電動救護車的日益普及。德國正積極採取措施減少碳足跡,電動救護車也因此越來越受歡迎。隨著歐洲各地環境法規的收緊,德國已開始採用包括救護車在內的電動車,以滿足嚴格的排放標準並改善空氣品質。此舉符合德國對永續發展的更廣泛承諾,並使其成為向環保緊急醫療服務 (EMS) 轉型的領導者。

全球救護車市場的主要參與者包括 Braun Industries、NAFFCO、Toyota、Demers Ambulances 和 Crestline Ambulance。為了擴大市場影響力,各公司正在投資電動救護車,以實現永續發展目標並降低營運成本。他們將即時遠距醫療和先進監控系統等尖端技術融入車輛中。與醫療服務提供者和政府機構合作,改善服務交付和車隊管理,有助於各公司提升競爭優勢。此外,進軍醫療基礎設施快速發展的新興市場,也使各公司得以挖掘新的收入來源。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 技術提供者

- 製造商

- 經銷商

- 最終用途

- 利潤率分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 其他國家的報復措施

- 對產業的影響

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 展望與未來考慮

- 對貿易的影響

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 慢性病和創傷病例增加

- 醫療支出不斷上漲

- 救護車技術的進步

- 全球醫療保健領域的投資不斷成長

- 產業陷阱與挑戰

- 營運和維護成本高

- 交通堵塞和反應時間延遲

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 類型 1

- 類型 2

- 類型 3

- 中型

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 緊急醫療服務

- 消防救護車

- 其他

第7章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第8章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 柴油引擎

- 汽油

- 電動車

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- Auto Ribeiro

- BAUS AT

- Bollanti

- Braun Industries

- Crestline Ambulance

- Demers Ambulances

- Excellence

- Frazer Ltd

- JCBL Group

- Life Line Emergency Vehicles

- Medicop

- Medix Specialty Vehicles

- Miller Coach Company

- NAFFCO

- O&H Vehicle Technology

- Osage Ambulances

- Profile Vehicles Oy

- REV Group

- Toyota

- WAS

The Global Ambulance Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 17.7 billion by 2034, driven by the increased healthcare spending and the rising importance of emergency medical services (EMS). Government and private sectors are investing significantly in expanding ambulance fleets, improving response times, and upgrading medical technology. These investments help ensure that ambulances are better equipped to handle emergencies, improving patient care during transport. As a result, ambulances are increasingly equipped with advanced medical equipment, such as ventilators, automated CPR devices, and advanced defibrillators, to manage critical conditions during transit.

The growing emphasis on airway management and ventilators further supports the ambulance market's growth. Ventilators are crucial in stabilizing patients with respiratory distress, ensuring oxygen is delivered effectively during emergencies such as cardiac arrest or severe trauma. With advanced features like adjustable pressure and volume control, these devices help paramedics provide critical care while en route to medical facilities. As more healthcare systems recognize the value of high-quality EMS, demand for better-equipped and specialized ambulances continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 5.8% |

In 2024, Type 1 ambulances led the market, accounting for 38% share. These vehicles, typically built on a truck chassis, provide a durable platform and additional space for medical equipment and personnel. The growing preference for Type 1 ambulances is driven by their ability to handle emergencies, including large-scale accidents or natural disasters, and their capacity to transport multiple patients or larger equipment.

The EMS segment held a 63% share in 2024, driven by healthcare providers prioritizing rapid, reliable transport of critically ill patients. Advances in telemedicine and mobile health solutions have further improved EMS capabilities, enabling paramedics to consult with doctors remotely and optimize care before patients arrive at the hospital. These innovations are expected to increase the demand for more advanced ambulances capable of longer-distance, high-level care during transport.

Germany Ambulance Market held a 15% share in 2024, fueled by strong regulatory support for environmental sustainability and the growing adoption of electric ambulances. The country is taking proactive steps to reduce its carbon footprint, making electric ambulances an increasingly popular choice. As environmental regulations tighten across Europe, Germany has embraced electric vehicles, including ambulances, to meet stringent emission standards and contribute to cleaner air. This move aligns with the nation's broader commitment to sustainability and has positioned it as a leader in the transition toward eco-friendly emergency medical services (EMS).

Key players in the Global Ambulance Market include Braun Industries, NAFFCO, Toyota, Demers Ambulances, and Crestline Ambulance. To expand their market footprint, companies are investing in electric ambulances to meet sustainability goals and reduce operational costs. They integrate cutting-edge technologies like real-time telemedicine and advanced monitoring systems into their vehicles. Collaborations with healthcare providers and government agencies to improve service delivery and fleet management are helping companies enhance their competitive advantage. Additionally, expanding into emerging markets where healthcare infrastructure is rapidly developing has allowed companies to tap into new revenue streams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Technology providers

- 3.2.3 Manufacturers

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise in chronic diseases and trauma cases

- 3.9.1.2 Rising healthcare expenditure

- 3.9.1.3 Advancements in ambulance technology

- 3.9.1.4 Growing investments in the healthcare sector across the globe

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High operational and maintenance cost

- 3.9.2.2 Traffic congestion and delayed response times

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Type 1

- 5.3 Type 2

- 5.4 Type 3

- 5.5 Medium-duty

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Emergency medical service

- 6.3 Fire ambulances

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Diesel

- 8.3 Gasoline

- 8.4 Electric vehicles

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Auto Ribeiro

- 10.2 BAUS AT

- 10.3 Bollanti

- 10.4 Braun Industries

- 10.5 Crestline Ambulance

- 10.6 Demers Ambulances

- 10.7 Excellence

- 10.8 Frazer Ltd

- 10.9 JCBL Group

- 10.10 Life Line Emergency Vehicles

- 10.11 Medicop

- 10.12 Medix Specialty Vehicles

- 10.13 Miller Coach Company

- 10.14 NAFFCO

- 10.15 O&H Vehicle Technology

- 10.16 Osage Ambulances

- 10.17 Profile Vehicles Oy

- 10.18 REV Group

- 10.19 Toyota

- 10.20 WAS

緊急醫療服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、醫療等級、服務提供者和付款方式分類)

緊急醫療服務市場:2026-2032年全球市場預測(依服務類型、車輛類型、醫療等級、服務提供者和付款方式分類) 緊急醫療服務市場規模、佔有率、趨勢和預測:按運輸車輛、緊急服務、設備和地區分類,2026-2034 年

緊急醫療服務市場規模、佔有率、趨勢和預測:按運輸車輛、緊急服務、設備和地區分類,2026-2034 年 救護車服務市場規模、佔有率和成長分析:按運輸方式、服務類型、應用和地區分類-2026-2033年產業預測

救護車服務市場規模、佔有率和成長分析:按運輸方式、服務類型、應用和地區分類-2026-2033年產業預測 全球救護車服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球救護車服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2025年全球緊急服務市場報告

2025年全球緊急服務市場報告 救護車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛、類型、應用、設備類型、地區和競爭細分,2020-2030 年

救護車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛、類型、應用、設備類型、地區和競爭細分,2020-2030 年 救護車市場:按車輛類型、設備等級和地區分類

救護車市場:按車輛類型、設備等級和地區分類 全球救護車市場

全球救護車市場 全球救護車服務市場分析與預測(至2034年):類型、產品、服務、技術、組件、應用、最終用戶、形式、設備、解決方案救護車市場:按車輛類型、按救護車類型、按配置、按地區

全球救護車服務市場分析與預測(至2034年):類型、產品、服務、技術、組件、應用、最終用戶、形式、設備、解決方案救護車市場:按車輛類型、按救護車類型、按配置、按地區