|

市場調查報告書

商品編碼

1750614

手術圈套器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Surgical Snares Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

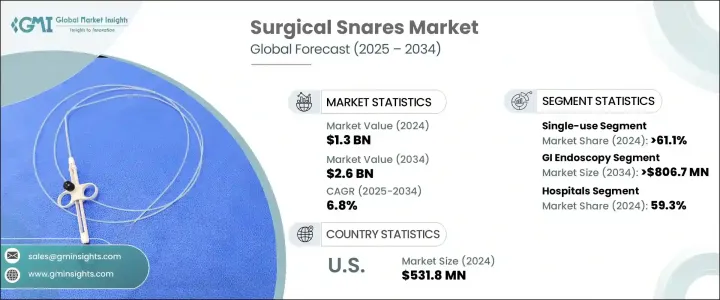

2024年,全球手術圈套器市場規模達13億美元,預計到2034年將以6.8%的複合年成長率成長,達到26億美元。這得歸功於胃腸道疾病的增加、人們對微創手術的日益青睞、內視鏡技術的進步以及全球醫療保健支出的不斷成長。人口老化加劇以及現代醫療工具的普及,進一步推動了手術圈套器需求的成長。隨著醫療保健系統越來越注重更有效率、更低風險的手術解決方案,這些器械在世界各地醫療機構的內視鏡應用中變得越來越重要。

手術圈套器是一種軟性線圈,是各種內視鏡手術中用於切除異常組織或異物的關鍵工具。這些裝置廣泛應用於大腸鏡檢查和支氣管鏡檢查等操作,能夠安全切除息肉、異常組織和異物,從而支持診斷和治療。它們無需進行侵入性手術即可進行精確切除,從而縮短了恢復時間並最大程度地減輕了患者不適,因此在門診和微創環境中具有很高的價值。手術圈套器旨在與現代內視鏡平台無縫整合,從而提高手術過程中的可視性、控制力和準確性。這種相容性不僅提高了手術效率,還減少了併發症並改善了患者預後。隨著醫療保健提供者擴大採用先進的內視鏡工具,手術圈套器已成為各種臨床環境中管理胃腸道和肺部疾病不可或缺的工具。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 26億美元 |

| 複合年成長率 | 6.8% |

2024年,一次性產品佔據市場佔有率的61.1%,佔據市場主導地位。一次性套圈器因其降低污染風險、提高手術效率和成本效益等優勢,正獲得強勁的市場吸引力。這些即用型、預先消毒的工具減少了對消毒基礎設施的依賴,並消除了重複使用醫療器材所帶來的風險。此外,監管機構和安全機構強調一次性醫療器材的使用,以最大限度地減少醫院內感染。這種偏好的轉變在高手術量和高風險的手術環境中尤其重要。

2024年,醫院內視鏡手術市佔率達到59.3%,這得益於對先進外科手術能力日益成長的需求,這些能力可用於處理複雜的胃腸道病例。醫院通常有更完善的基礎設施和尖端技術,因此成為外科圈套器的主要消費場所。在息肉切除術和組織切除術中,外科圈套器的使用率尤其高。此外,醫院內視鏡手術的保險覆蓋範圍也支持這些器械的更廣泛應用。

受微創技術的廣泛應用以及對高效、高精度手術器械日益成長的需求推動,美國手術圈套器市場規模在2024年達到5.318億美元。美國醫療保健產業重視病患恢復時間、手術精準度和病患舒適度,因此手術圈套器在內視鏡和腹腔鏡檢查中至關重要。先進手術中心的普及以及病患意識的提升,持續推動對這些器械的需求。

全球外科圈套器市場的領導公司包括奧林巴斯、庫克、康美德、泰利福、Merit Medical Systems、Hill-Rom Holdings、Avalign Technologies、美敦力、STERIS、EndoMed Systems、波士頓科學公司、Aspen Surgical、GPC Medical、Medline 和 Sklar Surgical Instruments。為了鞏固市場地位,各公司正在投資產品創新,專注於人體工學設計和更高的切割精度。與醫療機構的策略合作有助於製造商開發針對特定外科手術需求的客製化解決方案。許多公司正在透過收購和投資先進材料來擴展其產品組合,以提高設備的安全性和性能。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病盛行率不斷上升

- 內視鏡檢查數量激增

- 提高大腸直腸癌篩檢意識

- 微創手術日益受到青睞

- 產業陷阱與挑戰

- 使用圈套器的臨床併發症

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 2024年定價分析

- 報銷場景

- 應用潛力

- 差距分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按可用性,2021 - 2034 年

- 主要趨勢

- 一次使用

- 可重複使用的

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 胃腸內視鏡檢查

- 腹腔鏡檢查

- 膀胱鏡檢查

- 關節鏡檢查

- 支氣管鏡檢查

- 婦科內視鏡檢查

- 其他應用

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- aspen surgical

- Avalign Technologies

- Boston Scientific Corporation

- ConMed

- Cook

- EndoMed Systems

- GPC Medical

- Hill-Rom Holdings

- Medline

- Medtronic

- Merit Medical Systems

- Olympus

- Sklar Surgical Instruments

- STERIS

- Teleflex

The Global Surgical Snares Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 2.6 billion by 2034 due to an increase in gastrointestinal disorders, growing preference for minimally invasive procedures, advancements in endoscopic technologies, and rising global healthcare spending. A rapidly aging population and improved access to modern healthcare tools further contribute to the rising demand for surgical snares. With healthcare systems focusing on more efficient, lower-risk surgical solutions, these instruments are becoming increasingly vital in endoscopic applications across medical facilities worldwide.

Surgical snares, designed as flexible wire loops, are critical tools used during various endoscopic interventions to remove abnormal tissue or foreign bodies. These devices are widely utilized in procedures such as colonoscopy and bronchoscopy, supporting both diagnostic and therapeutic functions by enabling the safe removal of polyps, abnormal tissues, and foreign objects. Their ability to perform precise excisions without invasive surgery reduces recovery time and minimizes patient discomfort, making them highly valuable in outpatient and minimally invasive settings. Surgical snares are designed to seamlessly integrate with modern endoscopic platforms, allowing for improved visibility, control, and accuracy during procedures. This compatibility not only enhances procedural efficiency but also reduces complications and improves patient outcomes. As healthcare providers increasingly adopt advanced endoscopic tools, surgical snares have become indispensable in managing gastrointestinal and pulmonary conditions across various clinical environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 6.8% |

In 2024, the single-use segment led the market with a share of 61.1%. Disposable snares are gaining strong market traction due to benefits such as reduced contamination risk, improved surgical efficiency, and cost-effectiveness. These ready-to-use, pre-sterilized tools reduce reliance on sterilization infrastructure and eliminate risks associated with reusing medical instruments. Additionally, regulatory agencies and safety bodies emphasize disposable medical tools to minimize hospital-acquired infections. This shift in preference is especially significant in high-volume and high-risk surgical environments.

The hospital segment held a 59.3% share in 2024, driven by the growing need for advanced surgical capabilities to manage complex gastrointestinal cases. Hospitals typically offer better infrastructure and access to cutting-edge technologies, making them primary consumers of surgical snares. Their usage is particularly high in procedures involving polypectomy and tissue resection. Moreover, insurance coverage for hospital-based endoscopic procedures supports broader adoption of these devices.

United States Surgical Snares Market reached USD 531.8 million in 2024, driven by the widespread adoption of minimally invasive technologies and growing demand for efficient, high-precision surgical tools. The healthcare sector in the country emphasizes recovery time, surgical accuracy, and patient comfort, making surgical snares essential in endoscopy and laparoscopy. Availability of advanced surgical centers and increased patient awareness continue to push demand for these instruments.

Leading companies in the Global Surgical Snares Market include Olympus, Cook, ConMed, Teleflex, Merit Medical Systems, Hill-Rom Holdings, Avalign Technologies, Medtronic, STERIS, EndoMed Systems, Boston Scientific Corporation, Aspen Surgical, GPC Medical, Medline, and Sklar Surgical Instruments. To reinforce market position, companies are investing in product innovation, focusing on ergonomic designs and enhanced cutting precision. Strategic collaborations with healthcare institutions help manufacturers develop customized solutions tailored to specific surgical needs. Many are expanding their portfolios through acquisitions and investing in advanced materials to enhance device safety and performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic conditions

- 3.2.1.2 Surging number of endoscopies

- 3.2.1.3 Increasing awareness of colorectal cancer screening

- 3.2.1.4 Rising preference for minimally invasive surgeries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Clinical complications involved in the usage of snares

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Pricing analysis, 2024

- 3.8 Reimbursement scenario

- 3.9 Application potential

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Future market trends

- 3.14 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single-use

- 5.3 Reusable

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 GI endoscopy

- 6.3 Laparoscopy

- 6.4 Cystoscopy

- 6.5 Arthroscopy

- 6.6 Bronchoscopy

- 6.7 Gynecology endoscopy

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 aspen surgical

- 9.2 Avalign Technologies

- 9.3 Boston Scientific Corporation

- 9.4 ConMed

- 9.5 Cook

- 9.6 EndoMed Systems

- 9.7 GPC Medical

- 9.8 Hill-Rom Holdings

- 9.9 Medline

- 9.10 Medtronic

- 9.11 Merit Medical Systems

- 9.12 Olympus

- 9.13 Sklar Surgical Instruments

- 9.14 STERIS

- 9.15 Teleflex

手術勒除器市場:按產品類型、能源來源、應用和最終用戶分類 - 全球市場預測 2026-2032

手術勒除器市場:按產品類型、能源來源、應用和最終用戶分類 - 全球市場預測 2026-2032 全球外科勒除器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球外科勒除器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球外科圈套器市場報告

2026年全球外科圈套器市場報告 2032 年手術勒除器市場預測:按產品類型、圈套類型、材料、技術、應用、最終用戶和地區進行的全球分析

2032 年手術勒除器市場預測:按產品類型、圈套類型、材料、技術、應用、最終用戶和地區進行的全球分析 手術圈套器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按可用性、應用、最終用途、地區和競爭細分,2020-2030 年預測

手術圈套器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按可用性、應用、最終用途、地區和競爭細分,2020-2030 年預測 手術勒除器市場規模、佔有率、趨勢分析報告:按應用、最終用途、地區和細分市場預測,2025 年至 2030 年

手術勒除器市場規模、佔有率、趨勢分析報告:按應用、最終用途、地區和細分市場預測,2025 年至 2030 年 手術圈套器市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

手術圈套器市場,按類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測