|

市場調查報告書

商品編碼

1750581

食品乳化劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Food Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

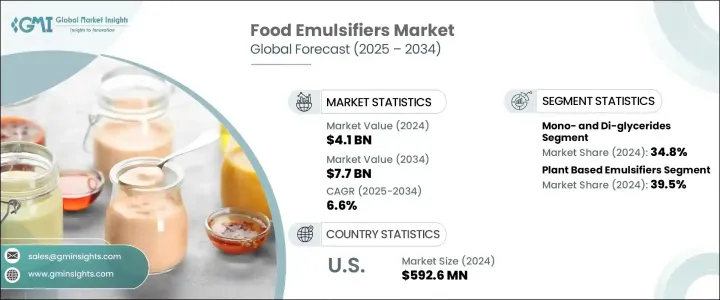

2024年,全球食品乳化劑市場規模達41億美元,預計到2034年將以6.6%的複合年成長率成長,達到77億美元,這主要得益於對簡便食品、植物性配料和清潔標籤產品日益成長的需求。乳化劑在改善食品結構、穩定性和保存期限方面發揮著至關重要的作用,廣泛應用於烘焙食品、乳製品、冷凍甜點、飲料、加工肉類、即食食品和嬰幼兒營養品等各個食品領域。隨著消費者擴大轉向清潔標籤和純素食,卵磷脂、葵花籽油和大豆油等天然和植物性乳化劑正日益受到青睞。此外,由於單甘油酯和雙甘油酯用途廣泛、經濟高效,且在功能性食品和簡便食品中應用廣泛,其需求仍將持續佔據主導地位。

就區域成長而言,由於飲食偏好的變化和城市化的加快,亞太市場正在快速擴張。歐洲和北美作為成熟市場,對天然、永續和清潔標籤成分的需求仍然強勁。食品安全和標籤透明度日益增強的監管支持也推動了乳化劑混合物的創新,增強了其在現代食品生產過程中的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 41億美元 |

| 預測值 | 77億美元 |

| 複合年成長率 | 6.6% |

單甘油酯和雙甘油酯佔據34.8%的市場佔有率,預計到2034年將以6.4%的複合年成長率成長。這些乳化劑因其多功能性、成本效益以及在烘焙、乳製品、糖果和加工食品等多個領域的廣泛應用而備受推崇。它們能夠作為穩定劑、乳化劑和調質劑,加上其較長的保存期限和良好的穩定性,鞏固了其作為食品行業最常用乳化劑之一的地位。這種廣泛的用途,加上其多功能性,確保了單甘油酯和雙甘油酯仍然是食品製造的主導選擇。

2024年,植物性乳化劑市場佔有39.5%的佔有率,預計到2034年將以6.2%的複合年成長率成長,這得益於消費者偏好明顯轉向天然植物成分,這些成分符合更永續、更注重健康的生活方式。隨著越來越多的消費者尋求環保和清潔標籤產品,對源自大豆、葵花籽和油菜籽的乳化劑的需求也在增加。這些植物性乳化劑因其營養價值、清潔標籤和永續採購而日益受到歡迎,所有這些都與消費者對更健康、更環保的食品選擇日益成長的需求相契合。

由於美國強大的食品加工產業和大量的簡便食品消費,美國食品乳化劑市場在2024年的價值達到5.926億美元。美國強勁的烘焙、乳製品和冷凍甜點產業進一步支撐了對乳化劑的需求。此外,美國消費者日益成長的健康保健趨勢也推動了對更多創新乳化劑的需求,包括植物性和天然替代品。美國完善的供應鏈和行銷體系使其在從本地和國際來源取得原料方面擁有競爭優勢。

全球食品乳化劑市場的領導者,例如嘉吉公司、科比昂公司、阿徹丹尼爾斯米德蘭公司 (ADM)、凱裡集團和禾大國際,正致力於實現產品組合多元化,擴大市場佔有率。這些公司正在大力投資研發,以創造更乾淨的植物性乳化劑,滿足消費者對永續產品日益成長的需求。他們也正在改進生產流程,以提高效率並降低成本。合作、併購是這些公司擴大市場足跡、提升其在全球食品乳化劑領域的競爭地位的關鍵策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 主要出口國(2021-2024年)

- 主要進口國(2021-2024年)

註:以上貿易統計僅針對重點國家。

- 消費者趨勢和偏好

- 清潔標籤運動

- 消費者對乳化劑的看法

- 天然與合成的偏好

- 對產品配方的影響

- 健康與保健趨勢

- 營養問題

- 過敏原考慮

- 飲食限制的影響

- 永續性和道德考慮

- 環境影響意識

- 永續採購偏好

- 包裝考慮

- 植物性純素食趨勢

- 對植物源乳化劑的需求

- 素食認證的影響

- 透明度和可追溯性要求

- 區域消費者偏好差異

- 清潔標籤運動

- 消費者行為分析

- 購買決策因素

- 價格敏感度分析

- 品牌忠誠度模式

- 社群媒體和數位對消費者感知的影響

- 供應鍊和原料分析

- 原料來源分析

- 關鍵原料

- 採購地區

- 採購的永續性

- 生產流程分析

- 製造技術

- 品質控制措施

- 成本結構分析

- 配銷通路分析

- 直接通路與間接通路

- 電子商務的影響

- 分銷挑戰

- 供應鏈挑戰

- 原物料價格波動

- 供應鏈中斷

- 物流挑戰

- 供應鏈最佳化策略

- 永續供應鏈實踐

- 供應鏈技術整合

- 原料來源分析

- 定價分析和成本結構

- 依產品類型進行價格點分析

- 2021-2025年價格趨勢分析

- 2025-2034年價格預測

- 影響定價的因素

- 原料成本

- 生產成本

- 監理合規成本

- 市場競爭

- 區域價格差異

- 主要參與者的定價策略

- 成本結構分析

- 原料成本

- 製造成本

- 分銷成本

- 行銷和銷售成本

- 依產品類別分析獲利能力

- 技術進步與創新

- 近期技術發展

- 乳化劑生產的新興技術

- 酵素修飾

- 微膠囊化

- 奈米科技應用

- 清潔標籤創新

- 天然乳化劑替代品

- 基於酵素的解決方案

- 植物性創新

- 永續生產技術

- 功能改進

- 增強穩定性

- 改善紋理特性

- 延長保存期限的解決方案

- 生產和品質控制中的數位技術

- 專利分析與研發趨勢

- 未來技術路線圖

- 永續性和環境影響

- 乳化劑的環境足跡

- 碳足跡分析

- 用水量評估

- 廢棄物產生和管理

- 永續採購實踐

- 棕櫚油永續性議題

- 大豆採購挑戰

- 替代永續能源

- 生物分解性和生態毒性評估

- 循環經濟方法

- 產業永續發展舉措

- 永續性的監管壓力

- 消費者對永續產品的需求

- 永續實踐的成本效益分析

- 乳化劑的環境足跡

- 市場挑戰與機遇

- 主要市場挑戰

- 健康問題和負面看法

- 監管障礙

- 原物料價格波動

- 清潔標籤配方挑戰

- 市場機會

- 植物性乳化劑的開發

- 新興市場擴張

- 功能性食品應用

- 永續乳化劑解決方案

- 宏觀經濟因素的影響

- 技術機會評估

- 戰略機會圖

- 主要市場挑戰

- 未來市場展望及預測

- 2025-2030 年產品類型市場預測

- 2025-2030年按應用分類的市場預測

- 2025-2030年各地區市場預測

- 新興市場趨勢

- 未來成長動力

- 市場演變情景

- 樂觀情境

- 現實場景

- 悲觀情景

- 投資機會評估

- 未來競爭格局預測

- 策略建議

- 市場進入策略

- 產品開發建議

- 區域擴張機會

- 競爭定位策略

- 永續發展實施路線圖

- 數位轉型策略

- 監理合規策略

- 行銷和品牌建議

- 風險緩解策略

- 投資優先框架

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 飲料產業蓬勃發展或將刺激產品需求

- 加工食品消費量的增加將促進產業成長

- 乳製品消費量成長或將有利於食品乳化劑產業成長

- 產業陷阱與挑戰

- 日益成長的健康問題

- 產品清潔標籤要求

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場規模及預測:依類型 2021 - 2034

- 主要趨勢

- 單甘油酯和雙甘油酯

- 卵磷脂

- 脫水山梨醇酯

- 硬脂醯乳酸酯

- 聚甘油酯

- 聚山梨醇酯

- 其他(DATEM、CSL等)

第6章:市場規模及預測:依來源,2021 - 2034

- 主要趨勢

- 植物性乳化劑

- 大豆衍生

- 向日葵衍生

- 棕櫚衍生

- 其他植物來源

- 動物性乳化劑

- 合成乳化劑

第7章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 烘焙和糖果

- 麵包和捲餅

- 蛋糕和糕點

- 餅乾和曲奇

- 巧克力和糖果

- 乳製品和冷凍甜點

- 冰淇淋和冷凍甜點

- 牛奶和奶油製品

- 乳酪製品

- 優格和發酵乳製品

- 加工肉類和海鮮

- 香腸和加工肉類

- 海鮮產品

- 簡便食品和即食食品

- 湯和醬汁

- 調味品和蛋黃醬

- 即食食品

- 飲料

- 碳酸飲料

- 果汁和果汁飲料

- 酒精飲料

- 植物飲料

- 嬰兒營養和嬰兒食品

- 嬰兒配方奶粉

- 嬰兒食品

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Archer Daniels Midland Company (ADM)

- Cargill, Inc.

- Croda International Plc

- Kerry Group plc

- Corbion NV

- Ingredion Incorporated

- Lasenor Emul, SL

- Palsgaard A/S

- Lonza

- Riken Vitamin

The Global Food Emulsifiers Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 7.7 billion by 2034, driven by the increasing demand for convenience foods, plant-based ingredients, and clean-label products. Emulsifiers play a vital role in improving the structure, stability, and shelf life of food products. They are used across various food sectors such as bakery, dairy, frozen desserts, beverages, processed meats, ready-to-eat meals, and infant nutrition. With an increasing shift toward clean label and vegan-friendly options, natural and plant-based emulsifiers such as lecithin, sunflower, and soy are gaining traction. Moreover, the demand for mono- and diglycerides continues to dominate due to their versatility, cost-effectiveness, and wide application in functional and convenience foods.

In terms of regional growth, the Asia Pacific market is expanding rapidly due to changing dietary preferences and rising urbanization. Europe and North America, while mature markets, continue to maintain strong demand for natural, sustainable, and clean-label ingredients. The growing regulatory support for food safety and label transparency is also driving the innovation of emulsifier blends, strengthening their presence in modern food production processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 6.6% |

The mono- and diglycerides segment holds 34.8% share and is forecasted to grow at a CAGR of 6.4% by 2034. These emulsifiers are highly regarded for their versatility, cost-effectiveness, and wide application across multiple sectors, including bakery, dairy, confectionery, and processed foods. Their ability to act as stabilizers, emulsifiers, and texturizers, combined with their long shelf life and consistency, has cemented their position as one of the most used emulsifiers in the food industry. This widespread usage, coupled with their multifunctionality, ensures that mono and diglycerides remain a dominant choice in food manufacturing.

The plant-based emulsifiers segment held 39.5% share in 2024 and is expected to grow at a CAGR of 6.2% through 2034, driven by a noticeable shift in consumer preferences toward natural, plant-derived ingredients that align with a more sustainable and health-conscious lifestyle. As more consumers seek eco-friendly and clean-label products, the demand for emulsifiers derived from soy, sunflower, and canola is growing. These plant-based emulsifiers are gaining popularity due to their nutritional benefits, clean labeling, and sustainable sourcing, all of which align with the rising consumer demand for healthier and environmentally responsible food options.

U.S. Food Emulsifiers Market was valued at USD 592.6 million in 2024 due to its strong food processing industry and high consumption of convenience foods. The country's robust bakery, dairy, and frozen dessert sectors further support the demand for emulsifiers. Additionally, the growing health and wellness trends among U.S. consumers are driving the need for more innovative emulsifiers, including plant-based and natural alternatives. The well-established supply chains and marketing systems in the U.S. contribute to its competitive advantage in obtaining raw materials from both local and international sources.

Leading players in the Global Food Emulsifiers Market, such as Cargill, Inc., Corbion N.V., Archer Daniels Midland Company (ADM), Kerry Group plc, and Croda International Plc, are focusing on diversifying their product portfolios and expanding their market presence. These companies are investing heavily in research and development to create cleaner, plant-based emulsifiers that meet the growing consumer demand for sustainable products. They are also enhancing their production processes to improve efficiency and reduce costs. Partnerships, mergers, and acquisitions are key strategies used by these companies to expand their market footprint and improve their competitive positioning in the global food emulsifier sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021 - 2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021 - 2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

- 3.4 Consumer trends and preferences

- 3.4.1 Clean label movement

- 3.4.1.1 Consumer perception of emulsifiers

- 3.4.1.2 Natural vs. synthetic preferences

- 3.4.1.3 Impact on product formulation

- 3.4.2 Health and wellness trends

- 3.4.2.1 Nutritional concerns

- 3.4.2.2 Allergen considerations

- 3.4.2.3 Dietary restrictions impact

- 3.4.3 Sustainability and ethical considerations

- 3.4.3.1 Environmental impact awareness

- 3.4.3.2 Sustainable sourcing preferences

- 3.4.3.3 Packaging considerations

- 3.4.4 Plant-based vegan trends

- 3.4.4.1 Demand for plant-derived emulsifiers

- 3.4.4.2 Vegan certification impact

- 3.4.5 Transparency and traceability demands

- 3.4.6 Regional consumer preference variations

- 3.4.1 Clean label movement

- 3.5 Consumer behavior analysis

- 3.5.1 Purchase decision factors

- 3.5.2 Price sensitivity analysis

- 3.5.3 Brand loyalty patterns

- 3.6 Social media and digital influence on consumer perception

- 3.7 Supply chain and raw material analysis

- 3.7.1 Raw material sourcing analysis

- 3.7.1.1 Key raw materials

- 3.7.1.2 Sourcing regions

- 3.7.1.3 Sustainability in sourcing

- 3.7.2 Production process analysis

- 3.7.2.1 Manufacturing technologies

- 3.7.2.2 Quality control measures

- 3.7.2.3 Cost structure analysis

- 3.7.3 Distribution channel analysis

- 3.7.3.1 Direct vs. indirect channels

- 3.7.3.2 E-commerce impact

- 3.7.3.3 Distribution challenges

- 3.7.4 Supply chain challenges

- 3.7.4.1 Raw material price volatility

- 3.7.4.2 Supply chain disruptions

- 3.7.4.3 Logistics challenges

- 3.7.5 Supply chain optimization strategies

- 3.7.6 Sustainable supply chain practices

- 3.7.7 Technology integration in supply chain

- 3.7.1 Raw material sourcing analysis

- 3.8 Pricing analysis and cost structure

- 3.8.1 Price point analysis by product type

- 3.8.2 Price trend analysis 2021–2025

- 3.8.3 Price forecast 2025–2034

- 3.8.4 Factors affecting pricing

- 3.8.4.1 Raw material costs

- 3.8.4.2 Production costs

- 3.8.4.3 Regulatory compliance costs

- 3.8.4.4 Market competition

- 3.8.4.5 Regional price variations

- 3.8.4.6 Pricing strategies of key players

- 3.8.4.7 Cost structure analysis

- 3.8.4.8 Raw material costs

- 3.8.4.9 Manufacturing costs

- 3.8.4.10 Distribution costs

- 3.8.4.11 Marketing and sales costs

- 3.8.5 Profitability analysis by product segment

- 3.9 Technological advancements and innovations

- 3.9.1 Recent technological developments

- 3.9.2 Emerging technologies in emulsifier production

- 3.9.2.1 Enzymatic modification

- 3.9.2.2 Microencapsulation

- 3.9.2.3 Nanotechnology applications

- 3.9.3 Clean label innovations

- 3.9.3.1 Natural emulsifier alternatives

- 3.9.3.2 Enzyme-based solutions

- 3.9.3.3 Plant-based innovations

- 3.9.4 Sustainable production technologies

- 3.9.5 Functional improvements

- 3.9.5.1 Enhanced stability

- 3.9.5.2 Improved texture properties

- 3.9.5.3 Extended shelf life solutions

- 3.9.6 Digital technologies in production and quality control

- 3.9.7 Patent analysis and r&d trends

- 3.9.8 Future technology roadmap

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental footprint of emulsifiers

- 3.10.1.1 Carbon footprint analysis

- 3.10.1.2 Water usage assessment

- 3.10.1.3 Waste generation and management

- 3.10.2 Sustainable sourcing practices

- 3.10.2.1 Palm oil sustainability issues

- 3.10.2.2 Soy sourcing challenges

- 3.10.2.3 Alternative sustainable sources

- 3.10.3 Biodegradability and eco-toxicity assessment

- 3.10.4 Circular economy approaches

- 3.10.5 Industry sustainability initiatives

- 3.10.6 Regulatory pressures for sustainability

- 3.10.7 Consumer demand for sustainable products

- 3.10.8 Cost-benefit analysis of sustainable practices

- 3.10.1 Environmental footprint of emulsifiers

- 3.11 Market challenges and opportunities

- 3.11.1 Key market challenges

- 3.11.1.1 Health concerns and negative perception

- 3.11.1.2 Regulatory hurdles

- 3.11.1.3 Raw material price volatility

- 3.11.1.4 Clean label formulation challenges

- 3.11.2 Market opportunities

- 3.11.2.1 Plant-based emulsifier development

- 3.11.2.2 Emerging markets expansion

- 3.11.2.3 Functional food applications

- 3.11.2.4 Sustainable emulsifier solutions

- 3.11.3 Impact of macro-economic factors

- 3.11.4 Technological opportunity assessment

- 3.11.5 Strategic opportunity mapping

- 3.11.1 Key market challenges

- 3.12 Future market outlook and forecast

- 3.12.1 Market forecast by product type 2025–2030

- 3.12.2 Market forecast by application 2025–2030

- 3.12.3 Market forecast by region 2025–2030

- 3.12.4 Emerging market trends

- 3.12.5 Future growth drivers

- 3.12.6 Market evolution scenarios

- 3.12.6.1 Optimistic scenario

- 3.12.6.2 Realistic scenario

- 3.12.6.3 Pessimistic scenario

- 3.12.7 Investment opportunities assessment

- 3.12.8 Future competitive landscape projection

- 3.13 Strategic recommendations

- 3.13.1 Market entry strategies

- 3.13.2 Product development recommendations

- 3.13.3 Regional expansion opportunities

- 3.13.4 Competitive positioning strategies

- 3.13.5 Sustainability implementation roadmap

- 3.13.6 Digital transformation strategies

- 3.13.7 Regulatory compliance strategies

- 3.13.8 Marketing and branding recommendations

- 3.13.9 Risk mitigation strategies

- 3.13.10 Investment prioritization framework

- 3.14 Supplier landscape

- 3.15 Profit margin analysis

- 3.16 Key news & initiatives

- 3.17 Regulatory landscape

- 3.18 Impact forces

- 3.18.1 Growth drivers

- 3.18.1.1 Growing beverage industry may fuel product demand

- 3.18.1.2 Increasing consumption of processed foods will foster industry growth

- 3.18.1.3 Growth in consumption of dairy products is likely to favor food emulsifier industry growth

- 3.18.2 Industry pitfalls & challenges

- 3.18.2.1 Growing health concerns

- 3.18.2.2 Clean label requirements for the product

- 3.18.1 Growth drivers

- 3.19 Growth potential analysis

- 3.20 Porter’s analysis

- 3.21 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Type 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Mono- and Di-glycerides

- 5.3 Lecithin

- 5.4 Sorbitan esters

- 5.5 Stearoyl lactylates

- 5.6 Polyglycerol esters

- 5.7 Polysorbates

- 5.8 Others (DATEM, CSL, etc.)

Chapter 6 Market Size and Forecast, By Source, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Plant-based emulsifiers

- 6.3 Soy-derived

- 6.4 Sunflower-derived

- 6.5 Palm-derived

- 6.6 Other plant sources

- 6.7 Animal-based emulsifiers

- 6.8 Synthetic emulsifiers

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and confectionery

- 7.2.1 Bread and rolls

- 7.2.2 Cakes and pastries

- 7.2.3 Biscuits and cookies

- 7.2.4 Chocolate and confectionery

- 7.3 Dairy and frozen desserts

- 7.3.1 Ice cream and frozen desserts

- 7.3.2 Milk and cream products

- 7.3.3 Cheese products

- 7.3.4 Yogurt and fermented dairy

- 7.4 Processed meat and seafood

- 7.4.1 Sausages and processed meats

- 7.4.2 Seafood products

- 7.5 Convenience foods and ready meals

- 7.5.1 Soup and sauces

- 7.5.2 Dressings and mayonnaise

- 7.5.3 Ready-to-eat meals

- 7.6 Beverages

- 7.6.1 Carbonated drinks

- 7.6.2 Fruit juices and nectars

- 7.6.3 Alcoholic beverages

- 7.6.4 Plant-based beverage

- 7.7 Infant nutrition and baby food

- 7.7.1 Infant formula

- 7.7.2 Baby food products

- 7.8 Other

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company (ADM)

- 9.2 Cargill, Inc.

- 9.3 Croda International Plc

- 9.4 Kerry Group plc

- 9.5 Corbion N.V.

- 9.6 Ingredion Incorporated

- 9.7 Lasenor Emul, S.L.

- 9.8 Palsgaard A/S

- 9.9 Lonza

- 9.10 Riken Vitamin