|

市場調查報告書

商品編碼

1750561

獸醫 CT 影像市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Veterinary CT Imaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

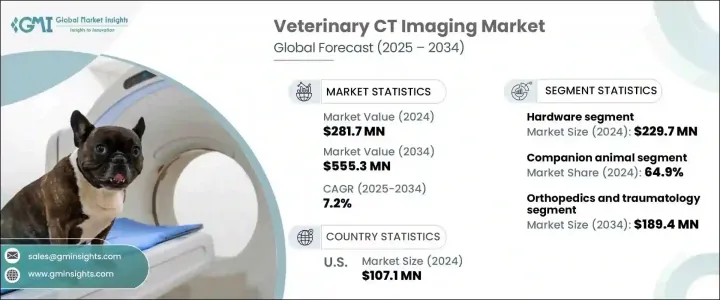

2024年,全球獸醫CT影像市場規模達2.817億美元,預計到2034年將以7.2%的複合年成長率成長,達到5.553億美元。這主要得益於全球動物數量的成長、寵物日益普及、獸醫服務可近性提高以及寵物照護日益受到重視等因素。隨著越來越多的寵物和牲畜被診斷出患有慢性和複雜的疾病,對包括獸醫CT成像在內的先進診斷技術的需求持續成長。這項技術透過提供清晰、細緻的3D動物解剖影像,徹底改變了獸醫評估動物健康狀況的方式,從而實現精準診斷和及時干預。

CT成像除了能夠提供複雜解剖結構的高解析度影像外,還尤其適用於急診。高解析度掃描儀和更快成像技術等創新進一步增強了其診斷能力,使其成為獸醫領域不可或缺的工具。此外,獸醫院和診所的蓬勃發展以及寵物保險的普及,正在推動市場擴張。隨著寵物和牲畜面臨的健康問題(例如腫瘤、骨科損傷和器官異常)日益增多,對CT掃描儀等診斷影像工具的需求將持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.817億美元 |

| 預測值 | 5.553億美元 |

| 複合年成長率 | 7.2% |

伴侶動物領域在2024年佔最大佔有率,達到64.9%,這得益於貓狗等寵物的普及,這些寵物越來越容易患上需要先進診斷工具的疾病。動物健康意識的增強以及專業治療手段的普及,預計將繼續推動獸醫CT影像的需求,尤其是伴侶動物CT影像的需求。新興經濟體可支配收入的增加以及更先進診斷設備的上市將進一步推動這一市場的發展。

2024年,獸用CT成像市場中的硬體部分價值2.297億美元。此部分包括CT掃描器、機架和偵測器等重要組件,這些組件對於獲取詳細的橫斷面影像以實現準確診斷至關重要。隨著獸醫診所和醫院越來越認知到先進診斷技術的重要性,預計對這些硬體解決方案的需求將穩步成長。這些組件對於產生高解析度影像至關重要,使獸醫能夠識別和治療動物的各種疾病。獸醫機構對先進診斷設備的持續投資將推動硬體部分的進一步成長,從而提升獸醫的整體診療能力。

2024年,美國獸醫CT影像市場規模達1.071億美元,這得益於美國寵物擁有率高以及獲得先進獸醫護理服務的機會日益增多。隨著人們對寵物健康的日益關注,寵物主人更傾向於為寵物尋找尖端的診斷工具,從而推動獸醫CT成像系統的普及。此外,寵物保險覆蓋率的提高也降低了這些先進診斷服務的可負擔性,進一步促進了市場成長。美國也受益於完善的基礎設施和成像技術的持續創新,確保市場保持強勁成長勢頭,並有望持續發展。

全球獸醫CT影像產業的公司採取的策略包括影像技術創新、產品組合拓展以及透過合作擴大市場覆蓋範圍。佳能醫療系統公司和西門子醫療等公司專注於開發更高解析度、影像速度更快的先進CT掃描儀,以滿足日益成長的精準診斷需求。通用電氣醫療集團和Hallmarq獸醫影像公司等其他公司則正在投資擴大產品線,並提升其在新興市場的影響力。透過提高獸醫影像解決方案的可近性和可負擔性,這些公司旨在鞏固其市場地位,並滿足獸醫領域對先進診斷工具日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 寵物擁有量和動物保健支出增加

- 動物疾病和傷害的發生率上升

- 成像模式的技術進步

- 已開發經濟體獸醫數量不斷增加

- 產業陷阱與挑戰

- CT掃描儀成本高昂

- 新興市場動物健康意識較低

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 硬體

- 固定式多層CT掃描儀

- 中端

- 高階

- 低階

- 攜帶式CT掃描儀

- 固定式多層CT掃描儀

- 耗材

- 軟體

第6章:市場估計與預測:依動物類型,2021 - 2034 年

- 主要趨勢

- 伴侶動物

- 牲畜

- 其他動物類型

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 骨科和創傷學

- 腫瘤學

- 牙科

- 神經病學

- 其他應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 獸醫醫院和診所

- 診斷影像中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Carestream Health

- Canon Medical Systems Corporation

- Epica International

- GNI ApS

- GE Healthcare

- Hallmarq Veterinary Imaging

- Hitachi

- Isabelle Vets

- Neurologica corporation

- Koninklijke Philips NV

- Siemens Healthineers

- Sound

- Shenzhen Anke High-Tech

- Xoran Technologies

The Global Veterinary CT Imaging Market was valued at USD 281.7 million in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 555.3 million by 2034, driven by factors such as an increasing global animal population, the rising popularity of pets, greater access to veterinary services, and a higher focus on pet care. As more pets and livestock are diagnosed with chronic and complex health conditions, the demand for advanced diagnostic technologies, including veterinary CT imaging, continues to rise. This technology has revolutionized the way veterinarians assess animal health by offering clear, detailed, and three-dimensional images of animal anatomy, allowing for precise diagnostics and timely interventions.

In addition to its ability to provide high-resolution images of complex anatomical structures, CT imaging is particularly beneficial for emergency cases. Innovations like higher resolution scanners and faster imaging techniques have further enhanced its diagnostic capabilities, making it an invaluable tool in the veterinary field. Furthermore, the growth in veterinary hospitals, clinics, and the increasing availability of pet insurance are boosting market expansion. As pets and livestock face a growing number of health issues, such as tumors, orthopedic injuries, and organ abnormalities, the demand for diagnostic imaging tools like CT scanners will continue to increase.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $281.7 Million |

| Forecast Value | $555.3 Million |

| CAGR | 7.2% |

The companion animal segment held the largest share with 64.9% in 2024, driven by the growing adoption of pets such as dogs and cats, which are increasingly prone to diseases that require advanced diagnostic tools. The increasing awareness of animal health and the availability of specialized treatments are expected to continue driving the demand for veterinary CT imaging, particularly for companion animals. The rising disposable income in emerging economies and the launch of more sophisticated diagnostic devices will further propel this market.

The hardware segment within the veterinary CT imaging market accounted for USD 229.7 million in 2024. This segment includes essential components such as CT scanners, gantries, and detectors, all of which are crucial for obtaining the detailed cross-sectional images that enable accurate diagnoses. As veterinary clinics and hospitals increasingly recognize the importance of advanced diagnostic technologies, the demand for these hardware solutions is expected to grow steadily. These components are critical for producing high-resolution images, allowing veterinarians to identify and address a wide range of conditions in animals. The continued investment in sophisticated diagnostic equipment by veterinary facilities will drive further growth in the hardware segment, enhancing the overall capabilities of veterinary medicine.

United States Veterinary CT Imaging Market was valued at USD 107.1 million in 2024, driven by high rates of pet ownership in the country, along with increasing access to advanced veterinary care. With the growing focus on pet health, owners are more inclined to seek out cutting-edge diagnostic tools for their animals, leading to greater adoption of veterinary CT imaging systems. Additionally, the rise in pet insurance coverage has facilitated the affordability of these advanced diagnostic services, further contributing to market growth. The U.S. also benefits from a well-established infrastructure and ongoing innovations in imaging technology, ensuring that the market remains strong and poised for continued development.

Companies in the Global Veterinary CT Imaging Industry employ strategies such as innovation in imaging technology, expanding product portfolios, and increasing market reach through partnerships and collaborations. Companies like Canon Medical Systems Corporation and Siemens Healthineers focus on developing advanced CT scanners with higher resolution and faster imaging capabilities to meet the growing demand for precise diagnostics. Others, like GE Healthcare and Hallmarq Veterinary Imaging, are investing in expanding their product offerings and increasing their presence in emerging markets. By improving the accessibility and affordability of veterinary imaging solutions, these companies aim to strengthen their market position and cater to the increasing demand for advanced diagnostic tools in veterinary medicine.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet ownership and animal health expenditure

- 3.2.1.2 Rising prevalence of animal diseases and injuries

- 3.2.1.3 Technological advancements in imaging modalities

- 3.2.1.4 Rising number of veterinary practitioners in developed economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of CT scanners

- 3.2.2.2 Low animal health awareness in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Stationary multi-slice CT scanner

- 5.2.1.1 Mid end

- 5.2.1.2 High end

- 5.2.1.3 Low end

- 5.2.2 Portable CT scanner

- 5.2.1 Stationary multi-slice CT scanner

- 5.3 Consumables

- 5.4 Software

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animal

- 6.3 Livestock animal

- 6.4 Other animal types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Orthopedics and traumatology

- 7.3 Oncology

- 7.4 Dental

- 7.5 Neurology

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Diagnostic imaging centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Carestream Health

- 10.2 Canon Medical Systems Corporation

- 10.3 Epica International

- 10.4 GNI ApS

- 10.5 GE Healthcare

- 10.6 Hallmarq Veterinary Imaging

- 10.7 Hitachi

- 10.8 Isabelle Vets

- 10.9 Neurologica corporation

- 10.10 Koninklijke Philips N.V.

- 10.11 Siemens Healthineers

- 10.12 Sound

- 10.13 Shenzhen Anke High-Tech

- 10.14 Xoran Technologies

動物影像市場依影像方式、動物類型、最終用戶、產品類型和銷售管道分類-2025-2032年全球預測動物影像市場(按組件、成像方式、動物類型、應用和最終用戶分類)—2025-2032 年全球預測小動物影像市場(按模式、動物類型、應用、最終用戶和組件)—全球預測 2025-2032

動物影像市場依影像方式、動物類型、最終用戶、產品類型和銷售管道分類-2025-2032年全球預測動物影像市場(按組件、成像方式、動物類型、應用和最終用戶分類)—2025-2032 年全球預測小動物影像市場(按模式、動物類型、應用、最終用戶和組件)—全球預測 2025-2032 2025年小動物影像(體內)全球市場報告2025年全球動物診斷影像市場報告獸醫診斷影像市場按產品類型、動物類型、模式、最終用戶、應用和分銷管道分類 - 全球預測 2025-20302025年全球動物影像市場報告

2025年小動物影像(體內)全球市場報告2025年全球動物診斷影像市場報告獸醫診斷影像市場按產品類型、動物類型、模式、最終用戶、應用和分銷管道分類 - 全球預測 2025-20302025年全球動物影像市場報告 全球動物MRI市場

全球動物MRI市場 美國獸醫用CT掃描儀市場:依類型、動物種類、應用、最終用戶、地區、機會及預測,2018-2032

美國獸醫用CT掃描儀市場:依類型、動物種類、應用、最終用戶、地區、機會及預測,2018-2032 獸醫診斷影像市場規模、佔有率、趨勢分析報告:按產品、動物類型、檢查類型、應用、模式、最終用途、地區、細分市場預測,2025-2033

獸醫診斷影像市場規模、佔有率、趨勢分析報告:按產品、動物類型、檢查類型、應用、模式、最終用途、地區、細分市場預測,2025-2033