|

市場調查報告書

商品編碼

1750532

燃料電池堆市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Fuel Cell Stack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

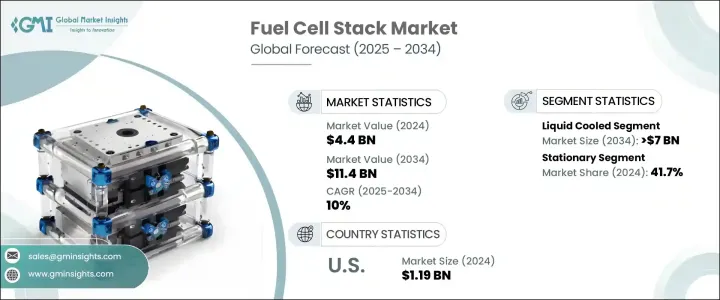

2024 年全球燃料電池堆市場價值為 44 億美元,預計到 2034 年將以 10% 的複合年成長率成長至 114 億美元。這一成長主要得益於支持永續能源技術(包括燃料電池)的監管框架的不斷加強。隨著各國和各產業加強應對氣候變遷和控制溫室氣體排放的力度,燃料電池堆在各種應用領域正獲得顯著發展。世界各國政府正透過稅收優惠、補貼和研究計畫積極推動清潔能源的應用,為市場成長創造有利環境。人們日益意識到傳統能源對環境的影響,促使各行各業轉向零排放解決方案,這進一步刺激了對燃料電池技術的需求。此外,氫能基礎設施的擴建和燃料電池與交通運輸(尤其是高性能和重型車輛)的整合預計將為市場發展開闢新的途徑。旨在提高性能、成本效益和可擴展性的技術進步也在加速市場發展勢頭。

燃料電池堆的需求在很大程度上受到工業、商業和住宅領域持續推動清潔能源替代能源的影響。隨著脫碳成為策略重點,燃料電池在能源系統中的作用日益擴大。它們能夠支援混合電力系統、提高電網可靠性並提供高效的備用電源,使其成為各行各業都極具吸引力的選擇。此外,包括能源公司、研究機構和製造商在內的利害關係人之間的合作正在加速產品創新和部署。透過改進材料和生產技術來簡化製造流程並降低成本的努力預計將提高燃料電池的經濟性和可及性,從而在未來幾年實現更廣泛的應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 44億美元 |

| 預測值 | 114億美元 |

| 複合年成長率 | 10% |

就產品類型而言,市場細分為風冷和液冷燃料電池堆。該產業在2022年達到38億美元,2023年達到41億美元,2024年達到44億美元。其中,液冷市場預計到2034年將超過70億美元。這一成長主要得益於燃料電池在高功率和高負載應用中的日益普及,以及先進的熱管理技術帶來的性能提升。液冷系統支援更穩定的運作條件、更好的散熱性能和更長的使用壽命,使其成為需要穩定可靠電力輸出的行業的理想選擇。液冷系統的不斷發展使其越來越適用於性能和耐用性至關重要的工業和商業備用系統。

根據應用,燃料電池堆市場可分為汽車、固定式、發電和其他。 2024年,固定式燃料電池佔最大佔有率,佔整體市場的41.7%。這種主導地位可歸因於固定式燃料電池系統的進步以及對永續和分散式能源解決方案日益成長的需求。隨著各行各業尋求減少碳足跡,固定式燃料電池系統正被用於為建築物、工廠和偏遠設施供電,以最大限度地降低排放。它們與再生能源的兼容性也支援創建混合系統,以確保能源效率、可靠性和備用能力。

從區域來看,北美在2024年佔據了全球燃料電池電堆市場的28.7%。光是美國市場,其市場規模在2022年就達到10.5億美元,2023年達到11.1億美元,2024年達到11.9億美元。該地區的成長得益於加氫基礎設施的建設和燃料電池汽車的普及。公共和私營部門對加氫分銷網路建設的持續投資預計將進一步增強該地區市場,使北美成為全球燃料電池領域的關鍵參與者。

燃料電池堆市場的競爭格局由成熟企業和新興創新企業共同構成。排名前五的參與者——普拉格能源、巴拉德動力系統、FuelCell Energy、Bloom Energy 和斗山燃料電池——合計佔據了超過 45% 的市場佔有率。雖然主導企業專注於擴大生產規模和降低系統成本,但新創公司則瞄準利基應用,並探索與再生能源技術的整合。隨著企業努力提高製造效率並採用替代材料,提供經濟高效且可擴展的燃料電池解決方案的競爭日益激烈。戰略投資、政府支持以及與清潔能源目標的契合持續重塑著市場動態,促進了整個產業的創新和競爭。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 策略舉措

- 公司市佔率

- 公司標竿分析

- 戰略儀表板

- 創新與技術格局

第5章:市場規模與預測:依類型,2021 年至 2034 年

- 主要趨勢

- 風冷

- 液冷

第6章:市場規模及預測:依產能,2021 年至 2034 年

- 主要趨勢

- <5千瓦

- 5千瓦 – 100千瓦

- >100千瓦 – 200千瓦

- >200千瓦

第7章:市場規模及預測:依應用,2021 年至 2034 年

- 主要趨勢

- 汽車

- 固定式

- 發電

- 其他

第8章:市場規模及預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 菲律賓

- 越南

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 秘魯

第9章:公司簡介

- Advent Technologies Holding

- Ballard Power Systems

- Commonwealth Automation Technologies

- Dana Incorporated

- ElringKlinger

- FuelCell Energy Solutions

- Freudenberg Group

- Horizon Fuel Cell Technologies

- Intelligent Energy Limited

- Nedstack Fuel Cell Technology

- Nuvera Fuel Cells

- PowerCell Sweden

- Plug Power

- Robert Bosch

- Schunk Bahn-und Industrietechnik

- TW Horizon Fuel Cell Technologies

The Global Fuel Cell Stack Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing enforcement of regulatory frameworks that support sustainable energy technologies, including fuel cells. As nations and industries intensify efforts to combat climate change and curb greenhouse gas emissions, fuel cell stacks are gaining significant traction across various applications. Governments around the world are actively promoting clean energy adoption through tax incentives, subsidies, and research initiatives, creating a favorable environment for market growth. Growing awareness of the environmental impact of conventional energy sources is prompting industries to shift toward zero-emission solutions, which is further bolstering the demand for fuel cell technology. Additionally, the expansion of hydrogen infrastructure and the integration of fuel cells into transportation-especially for high-performance and heavy-duty vehicles-are expected to create new avenues for market development. Technological advances aimed at improving performance, cost-efficiency, and scalability are also accelerating market momentum.

The demand for fuel cell stacks is heavily influenced by the continuous push for clean energy alternatives in the industrial, commercial, and residential sectors. As decarbonization becomes a strategic priority, the role of fuel cells in energy systems is expanding. Their ability to support hybrid setups, improve grid reliability, and provide efficient backup power makes them an attractive choice across sectors. Moreover, collaborations among stakeholders-including energy companies, research institutes, and manufacturers-are helping accelerate product innovation and deployment. Efforts to streamline manufacturing processes and reduce costs through improved materials and production techniques are expected to enhance affordability and accessibility, enabling broader adoption in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 10% |

In terms of product type, the market is segmented into air-cooled and liquid-cooled fuel cell stacks. The industry recorded USD 3.8 billion in 2022, USD 4.1 billion in 2023, and USD 4.4 billion in 2024. Among these, the liquid-cooled segment is projected to surpass USD 7 billion by 2034. This growth is being driven by the increasing use of fuel cells in high-power and intensive-duty applications, along with enhanced performance enabled by advanced thermal management. Liquid cooling systems support more stable operating conditions, better heat dissipation, and extended lifespan-making them ideal for sectors that demand consistent and reliable power output. The ongoing development of liquid-cooled systems is making them increasingly suitable for industrial and commercial backup systems where performance and durability are critical.

On the basis of application, the fuel cell stack market is categorized into automotive, stationary, power generation, and others. In 2024, the stationary segment held the largest share, accounting for 41.7% of the overall market. This dominance can be attributed to advancements in stationary fuel cell systems and the growing demand for sustainable and decentralized energy solutions. As industries seek to reduce their carbon footprints, stationary fuel cell systems are being adopted to power buildings, factories, and remote facilities with minimal emissions. Their compatibility with renewable energy sources also supports the creation of hybrid systems that ensure energy efficiency, reliability, and backup capabilities.

Regionally, North America held a 28.7% share of the global fuel cell stack market in 2024. The U.S. market alone was valued at USD 1.05 billion in 2022, USD 1.11 billion in 2023, and USD 1.19 billion in 2024. Growth in this region is supported by the development of hydrogen refueling infrastructure and increased deployment of fuel cell-powered vehicles. Continued public and private investment in building out hydrogen distribution networks is expected to strengthen the regional market further, positioning North America as a key player in the global fuel cell landscape.

The competitive landscape of the fuel cell stack market is marked by a combination of established companies and emerging innovators. The top five players- Plug Power, Ballard Power Systems, FuelCell Energy, Bloom Energy, and Doosan Fuel Cell-collectively contribute over 45% of the total market share. While dominant firms focus on scaling up production and reducing system costs, startups are targeting niche applications and exploring integration with renewable energy technologies. As companies strive to enhance manufacturing efficiency and adopt alternative materials, the race to provide cost-effective and scalable fuel cell solutions is intensifying. Strategic investments, government support, and alignment with clean energy goals continue to reshape market dynamics, encouraging innovation and competition throughout the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic initiatives

- 4.3 Company market share

- 4.4 Company benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Air Cooled

- 5.3 Liquid Cooled

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 <5 kW

- 6.3 5 kW – 100 kW

- 6.4 >100 kW – 200 kW

- 6.5 >200 kW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Stationary

- 7.4 Power generation

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Philippines

- 8.4.6 Vietnam

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Peru

Chapter 9 Company Profiles

- 9.1 Advent Technologies Holding

- 9.2 Ballard Power Systems

- 9.3 Commonwealth Automation Technologies

- 9.4 Dana Incorporated

- 9.5 ElringKlinger

- 9.6 FuelCell Energy Solutions

- 9.7 Freudenberg Group

- 9.8 Horizon Fuel Cell Technologies

- 9.9 Intelligent Energy Limited

- 9.10 Nedstack Fuel Cell Technology

- 9.11 Nuvera Fuel Cells

- 9.12 PowerCell Sweden

- 9.13 Plug Power

- 9.14 Robert Bosch

- 9.15 Schunk Bahn-und Industrietechnik

- 9.16 TW Horizon Fuel Cell Technologies

全球小型空冷式氫燃料電池銷售市場報告、競爭分析及區域商機(2026-2032年)

全球小型空冷式氫燃料電池銷售市場報告、競爭分析及區域商機(2026-2032年) 全球小型空氣冷卻水塔市場展望、詳細分析及至2032年預測

全球小型空氣冷卻水塔市場展望、詳細分析及至2032年預測 可擴展燃料電池模組市場(依產品類型、燃料種類、功率輸出、電壓、應用和最終用戶)-2025-2030 年全球預測

可擴展燃料電池模組市場(依產品類型、燃料種類、功率輸出、電壓、應用和最終用戶)-2025-2030 年全球預測 全球燃料電池堆回收再利用市場

全球燃料電池堆回收再利用市場 氫燃料電池堆市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、按功率、按應用、按地區及競爭分類,2020-2030 年)

氫燃料電池堆市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、按功率、按應用、按地區及競爭分類,2020-2030 年) 全球燃料電池堆市場

全球燃料電池堆市場 燃料電池堆全球市場 -市場佔有率和排名、總收入、需求預測(2025-2031)

燃料電池堆全球市場 -市場佔有率和排名、總收入、需求預測(2025-2031) 2024-2028年氫燃料電池堆全球市場

2024-2028年氫燃料電池堆全球市場 2024-2032年全球燃料電池堆回收再利用市場預測2024-2032年日本燃料電池堆回收再利用市場預測

2024-2032年全球燃料電池堆回收再利用市場預測2024-2032年日本燃料電池堆回收再利用市場預測