|

市場調查報告書

商品編碼

1750502

船舶交通管理市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Vessel Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

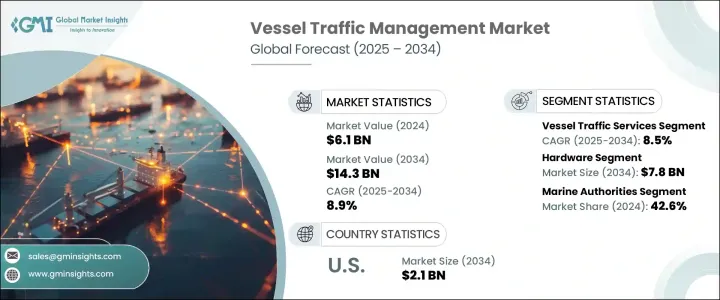

2024年,全球船舶交通管理市場規模達61億美元,預計2034年將以8.9%的複合年成長率成長,達到143億美元。這主要得益於對能夠高效安全地處理日益成長的船舶流量的更智慧交通系統的需求。由於船舶運輸量不斷增加,全球港口基礎設施面臨壓力,促使人們採用高性能系統來增強導航能力、減少瓶頸並提升港口營運效率。國際貿易政策和原物料價格波動引發的產業變革促使企業進行在地化生產,並重新思考其供應鏈策略,以降低地緣政治風險。隨著港口堵塞問題日益嚴重,對能夠簡化營運並確保符合安全法規的技術的需求比以往任何時候都更加重要。

市場深受擁擠海上航線即時船舶監控需求日益成長的影響。融合雷達、甚高頻通訊和自動辨識技術的增強型船舶交通管理系統,對商業和國防海事當局而言都至關重要。這些系統能夠實現無縫協調、態勢感知,並在高密度交通區域實現更安全的航行。船舶交通服務這一細分市場正受到顯著發展,這得益於人們對數位海事基礎設施日益成長的興趣以及對港口安全和監控系統投資的增加。隨著人們專注於降低環境風險和改善海上物流,各地區對智慧互聯技術的需求正在激增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 61億美元 |

| 預測值 | 143億美元 |

| 複合年成長率 | 8.9% |

從組件角度來看,硬體在船舶交通管理生態系統中佔據重要地位,預計到2034年將達到78億美元。這包括各種資料收集和傳輸所需的海事設備,例如感測器、雷達和通訊模組。船舶安全監管的加強持續推動了這項需求。儘管硬體佔據主導地位,但隨著港口尋求包含資料分析、遠端管理和預測性維護的整合解決方案,服務領域有望加速成長。

按最終用途分類,海事部門在2024年佔42.6%,因其在規範航行安全和環境標準方面發揮的關鍵作用而佔據主導地位。這些部門利用船舶交通系統來加強對船舶交通的管控,並確保國內和國際水域的平穩運作。依靠雷達、AIS和綜合通訊系統等即時監控工具,他們能夠主動管理海上風險,緩解堵塞,並迅速應對緊急情況。

預計到2034年,美國船舶交通管理市場規模將達到21億美元,這得益於更嚴格的安全規程和尖端船舶交通管理系統(VTMS)的部署。聯邦政府的授權和海岸防衛隊的舉措加速了現代監控系統在高流量區域的推廣。此外,美國對港口基礎設施升級和人工智慧工具整合的重視,刺激了對智慧船舶交通管理系統(VTM)平台的持續需求。然而,小型港口營運商的預算限制,加上貿易不確定性和地緣政治緊張局勢,仍然是某些地區快速擴張的障礙。

為了鞏固競爭優勢,諾斯羅普·格魯曼公司、萊昂納多公司、康斯伯格集團、新科工程公司和薩博公司等公司正大力投資研發和創新。他們利用人工智慧、物聯網和預測分析技術,提供更智慧、可擴展的船舶交通管理解決方案。為了進入高潛力市場,他們也優先考慮與政府和港務局的合作。許多公司正在透過端到端船舶交通管理系統 (VTMS) 功能增強其服務組合,以應對全球日益成長的營運複雜性和監管需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 生長

- 全球海上貿易量不斷成長

- 港口擁擠加劇,營運效率需求增加

- 人工智慧、機器學習和即時監控技術的進步

- 嚴格的海事安全與環境法規

- 港口基礎建設現代化投資

- 產業陷阱與挑戰

- 安裝和維護成本高

- 傳統系統與現代系統之間的互通性有限

- 生長

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按系統類型,2021 年至 2034 年

- 主要趨勢

- 船舶交通服務(VTS)

- 港口管理系統(PMS)

- 自動辨識系統(AIS)

- 基於雷達的系統

第6章:市場估計與預測:按組件,2021 年至 2034 年

- 主要趨勢

- 硬體

- 軟體

- 服務

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 海事部門

- 港口和海港

- 商業船舶營運商

- 海軍

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Elcome International LLC

- Frequentis

- Furuno

- Hensoldt

- Indra Sistemas

- Japan Radio Co. Ltd.

- Kongsberg Gruppen

- Leonardo SpA

- Marlink AS

- Northrop Grumman Corporation

- Saab

- ST Engineering

- Terma

- Thales Group

- Wartsilä

The Global Vessel Traffic Management Market was valued at USD 6.1 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 14.3 billion by 2034, driven by the demand for smarter traffic systems capable of handling increasing vessel volumes efficiently and safely. Global port infrastructure is under pressure due to growing ship movements, driving the adoption of high-performance systems that enhance navigation, reduce bottlenecks, and boost port operations. Industry shifts caused by international trade policies and material price volatility prompt companies to localize production and rethink their supply chain strategies to reduce geopolitical risks. As ports face rising congestion, the need for technologies that can streamline operations while ensuring compliance with safety regulations is more important than ever.

The market is heavily influenced by the rising need for real-time ship monitoring in congested sea routes. Enhanced vessel traffic management systems that incorporate radar, VHF communications, and automatic identification technologies are becoming essential for both commercial and defense maritime authorities. These systems enable seamless coordination, situational awareness, and safer navigation through high-density traffic zones. One segment, Vessel Traffic Services, is experiencing significant traction due to growing interest in digital maritime infrastructure and increasing investments in port security and surveillance systems. With a focus on minimizing environmental risk and improving maritime logistics, demand for intelligent and connected technologies is surging across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.1 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 8.9% |

From a component standpoint, hardware holds a strong presence in the vessel traffic management ecosystem and is forecasted to hit USD 7.8 billion by 2034. This includes a wide range of maritime equipment necessary for data collection and transmission, such as sensors, radar, and communication modules. Tighter regulatory enforcement for ship safety continues to drive this demand. Although hardware dominates, the services segment is poised for accelerated growth as ports look for integrated solutions that include data analytics, remote management, and predictive maintenance.

Based on end-use, the marine authorities segment accounted for a 42.6% share in 2024, dominating the segment due to their critical role in regulating navigation safety and environmental standards. These authorities turn to vessel traffic systems to enhance control over ship traffic and ensure smooth operations in national and international waters. The reliance on real-time monitoring tools like radar, AIS, and integrated communications systems allows them to proactively manage maritime risks, mitigate congestion, and respond swiftly to emergencies.

U.S. Vessel Traffic Management Market is expected to reach USD 2.1 billion by 2034, supported by the push for stricter safety protocols and cutting-edge VTMS deployments. Federal mandates and Coast Guard initiatives have accelerated the rollout of modern monitoring systems across high-traffic zones. Furthermore, the nation's emphasis on upgrading port infrastructure and integrating AI-driven tools has spurred consistent demand for intelligent VTM platforms. However, budget constraints among smaller port operators, coupled with trade uncertainties and geopolitical tensions, remain barriers to rapid expansion in certain regions.

To solidify their competitive edge, companies like Northrop Grumman Corporation, Leonardo S.p.A., Kongsberg Gruppen, ST Engineering, and Saab AB are investing heavily in research and innovation. They leverage artificial intelligence, IoT, and predictive analytics to deliver smarter, scalable vessel traffic management solutions. Collaborations with governments and port authorities are also prioritized to gain access to high-potential markets. Many players are enhancing their service portfolios with end-to-end VTMS capabilities to address growing operational complexity and regulatory demands globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth

- 3.3.1.1.1 Rising global maritime trade volumes

- 3.3.1.1.2 Increasing port congestion and demand for operational efficiency

- 3.3.1.1.3 Advancements in AI, ML, and real-time monitoring technologies

- 3.3.1.1.4 Stringent maritime safety and environmental regulations

- 3.3.1.1.5 Investments in port infrastructure modernization

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1.1 High installation and maintenance costs

- 3.3.2.1.2 Limited interoperability between legacy and modern systems

- 3.3.1 Growth

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By System Type, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Vessel traffic services (VTS)

- 5.3 Port management systems (PMS)

- 5.4 Automatic identification system (AIS)

- 5.5 Radar-based systems

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Marine authorities

- 7.3 Ports and harbours

- 7.4 Commercial vessel operators

- 7.5 Naval forces

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Elcome International LLC

- 9.2 Frequentis

- 9.3 Furuno

- 9.4 Hensoldt

- 9.5 Indra Sistemas

- 9.6 Japan Radio Co. Ltd.

- 9.7 Kongsberg Gruppen

- 9.8 Leonardo S.p.A.

- 9.9 Marlink AS

- 9.10 Northrop Grumman Corporation

- 9.11 Saab

- 9.12 ST Engineering

- 9.13 Terma

- 9.14 Thales Group

- 9.15 Wartsilä

船舶交通管理市場-2026-2032年全球市場預測

船舶交通管理市場-2026-2032年全球市場預測 海上交通管理市場規模、佔有率和成長分析:按組件、系統類型、部署模式、港口類型、應用和地區分類-2026-2033年產業預測

海上交通管理市場規模、佔有率和成長分析:按組件、系統類型、部署模式、港口類型、應用和地區分類-2026-2033年產業預測 海上交通管理市場報告:趨勢、預測與競爭分析(至2035年)

海上交通管理市場報告:趨勢、預測與競爭分析(至2035年) 2026年全球海洋交通管理市場報告

2026年全球海洋交通管理市場報告 2026-2034年全球海上交通管理市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球海上交通管理市場規模、佔有率、趨勢和成長分析報告 船舶交通管理系統市場規模、佔有率和成長分析(按應用、系統類型、最終用途、部署類型和地區分類)-2026-2033年產業預測

船舶交通管理系統市場規模、佔有率和成長分析(按應用、系統類型、最終用途、部署類型和地區分類)-2026-2033年產業預測 船舶交通管理市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、系統、最終用戶、地區和競爭格局分類,2020-2030 年預測)

船舶交通管理市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、系統、最終用戶、地區和競爭格局分類,2020-2030 年預測) 船舶交通管理系統市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032 年)

船舶交通管理系統市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032 年) 船舶交通管理系統市場,全球 2025-2029

船舶交通管理系統市場,全球 2025-2029