|

市場調查報告書

商品編碼

1750496

汽車座椅市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Seating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

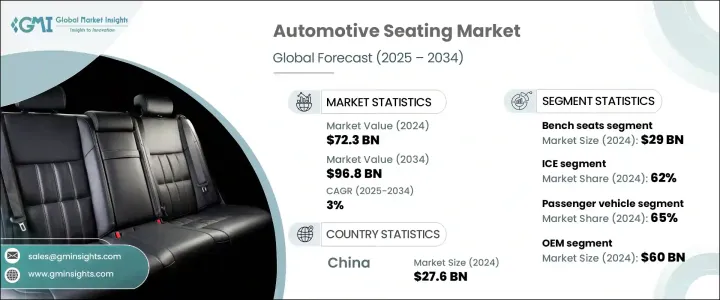

2024年,全球汽車座椅市場規模達723億美元,預計2034年將以3%的複合年成長率成長,達到968億美元。這得益於汽車產量的增加、安全法規的日益嚴格以及消費者對舒適性和便利性的日益成長的期望。汽車製造商正在重新思考座椅系統,不僅要提升美觀和乘客體驗,還要整合智慧技術和永續材料,以滿足不斷變化的標準和買家偏好。

汽車座椅產業一個顯著的轉變是越來越重視人體工學和健康設計。汽車製造商正在增加對先進座椅技術的投資,例如可客製化的腰部支撐、壓力感應系統、姿勢矯正機制以及智慧座椅監控解決方案。這些功能不僅旨在提升駕駛舒適度,還能透過減少疲勞和改善長途旅行中的脊椎矯正來支持長期健康。輕質複合材料擴大被應用於平衡結構強度和減輕車重,從而提高燃油效率和能源效率。這種對智慧人體工學座椅系統的關注,將車內環境轉變為更以使用者為中心的環境,幫助製造商滿足不斷變化的消費者期望。隨著即使在中階車型中,對高階體驗的需求也日益成長,座椅已成為品牌差異化和買家決策的決定性因素。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 723億美元 |

| 預測值 | 968億美元 |

| 複合年成長率 | 3% |

2024年,內燃機 (ICE) 汽車市場佔據了 62% 的市場佔有率,憑藉其在全球汽車產品線中的廣泛佈局,將繼續佔據主導地位。然而,電動車 (EV) 市場正在蓬勃發展,預計在預測期內的複合年成長率約為 4%。雖然 ICE 車型因其多樣性和便利性而廣受歡迎,但電動車製造商也加入了先進的座椅功能,例如腰部調節、通風和按摩功能,以吸引那些精通科技、注重舒適性的消費者。

2024年,長排座椅市場規模將達290億美元。長排座椅之所以受歡迎,源自於其在SUV、廂型車和多用途車中的實用性,而這些車型都注重乘客空間的最大化。這些配置可以增加座位容量並實現靈活的佈局,使其非常適合家庭和車隊用車市場。其流線型結構和經濟實惠的價格,使其在發展中市場和成熟市場都繼續成為可靠的選擇。

2024年,中國汽車座椅市場規模達276億美元,這得益於汽車製造生態系統的蓬勃發展、人們對高科技內飾功能日益成長的偏好,以及對注重客製化化、互聯互通和高階體驗的座椅系統的新需求。隨著電動車和豪華車型的日益普及,通風座椅、電子調節和記憶功能等功能正成為標配。中國汽車製造商正透過快速創新和強化在地化生產來應對這一挑戰,進一步鞏固了中國在區域座椅產業的主導地位。

塑造這一市場的關鍵參與者包括 GRAMMER、RECARO Holding、豐田紡織、李爾、MG Seating Systems、安道拓、麥格納國際、博澤西特、佛吉亞和費希爾公司。為了保持競爭優勢,領先的汽車座椅製造商專注於策略性舉措,例如對永續和人體工學材料的研發投資、與原始設備製造商的合作以及區域製造擴張。許多公司整合了數位技術和人工智慧座椅系統,以提升乘客體驗、增強品牌形象,並與頂級汽車製造商簽訂長期合約。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 材料供應商

- 組件提供者

- 製造商

- 經銷商

- 原始設備製造商

- 技術整合商

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 策略產業反應

- 供應鏈重組

- 對貿易的影響

- 定價和產品策略

- 技術與創新格局

- 當前的技術趨勢

- 智慧座椅技術

- 與車輛系統整合

- 減重技術

- 舒適度增強技術

- 新興技術

- 人工智慧和機器學習應用

- 座椅系統中的物聯網整合

- 生物特徵感測和監測

- 先進材料科學

- 當前的技術趨勢

- 專利分析

- 重要新聞和舉措

- 消費者偏好和行為

- 舒適度期望

- 人口因素對座位偏好的影響

- 消費者對座椅舒適度的看法

- 價格趨勢

- 座位

- 地區

- 成本細分分析

- 監管格局

- 衝擊力

- 成長動力

- 智慧互聯座椅技術的整合

- 輕質和永續材料的進步

- 電動和自動駕駛汽車內裝重新配置的成長

- 透過感測器和安全氣囊整合增強安全功能

- 產業陷阱與挑戰

- 聚氨酯泡沫和複合材料回收的複雜性

- 先進座椅機構的開發成本高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按座位,2021 - 2034

- 主要趨勢

- 折疊座椅

- 桶形座椅

- 長椅座椅

- 分離座椅

- 其他

第6章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 標準

- 供電

- 通風

- 氣候控制

- 按摩

- 其他

第7章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 真皮

- 合成皮革

- 織物

- 永續的

- 回收利用

- 生物基

- 植物衍生

第8章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第9章:市場估計與預測:依組件,2021 - 2034

- 主要趨勢

- 框架

- 泡棉墊

- 座椅調整器

- 頭枕

- 其他

第10章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 內燃機(ICE)

- 電動車(EV)

- 油電混合車

第 11 章:市場估計與預測:按銷售管道,2021 年至 2034 年

- 主要趨勢

- 原始設備製造商 (OEM)

- 售後市場

第 12 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第13章:公司簡介

- Adient

- Brose Sitech

- Camaco-Amvian

- Dura Automotive Systems

- Faurecia

- Fisher and Company

- Freedman Seating

- GRAMMER

- Guelph Manufacturing

- Lear

- Magna International

- MG Seating Systems

- NHK Spring

- RECARO

- TACHI-S

- TM Systems

- Toyota Boshoku

- True Assistive Tech

- TS Tech

- Woodbridge

The Global Automotive Seating Market was valued at USD 72.3 billion in 2024 and is estimated to grow at a CAGR of 3% to reach USD 96.8 billion by 2034, fueled by increasing automobile production, tightening safety regulations, and rising consumer expectations for comfort and convenience. Automakers are rethinking seating systems not only to enhance aesthetics and passenger experience but to integrate smart technologies and sustainable materials that meet evolving standards and buyer preferences.

A noticeable shift in the automotive seating industry is the growing prioritization of ergonomics and health-conscious design. Automakers are ramping up investments in advanced seat technologies such as customizable lumbar support, pressure-sensing systems, posture correction mechanisms, and smart in-seat monitoring solutions. These features are designed not only to elevate driving comfort but also to support long-term health by reducing fatigue and enhancing spinal alignment during extended travel. Lightweight composite materials are increasingly used to balance structural strength with reduced vehicle weight, contributing to greater fuel and energy efficiency. This focus on intelligent, ergonomic seating systems transforms vehicle interiors into more user-centric environments, helping manufacturers meet evolving consumer expectations. As demand rises for premium experiences even in mid-range vehicles, seating has become a defining element of brand distinction and buyer decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $72.3 Billion |

| Forecast Value | $96.8 Billion |

| CAGR | 3% |

The internal combustion engine (ICE) vehicles segment held a 62% share in 2024, continuing to dominate due to their extensive presence across global automotive lineups. However, the electric vehicle (EV) segment is gaining momentum, projected to grow at approximately 4% CAGR through the forecast period. While ICE models remain popular for their variety and accessibility, EV manufacturers incorporate sophisticated seat functionalities, like lumbar adjustments, ventilation, and massage features, to attract tech-savvy, comfort-driven consumers.

In 2024, the bench seats segment will generate USD 29 billion. Their popularity stems from their practicality in SUVs, vans, and multipurpose vehicles, where maximizing passenger space is essential. These configurations allow for increased seating capacity and versatile layouts, making them well-suited for both family and fleet-oriented vehicle segments. Their streamlined construction and affordability continue to make bench seats a reliable choice in both developing and mature markets.

China Automotive Seating Market generated USD 27.6 billion in 2024, driven by the vehicle manufacturing ecosystem, a rising preference for high-tech interior features, and the new demand for seating systems prioritizing customization, connectivity, and premium feel. As electric vehicles and luxury models gain traction, features like ventilated seating, electronic adjustability, and memory functions are becoming standard expectations. China's automakers are responding with rapid innovation and enhanced local production, further reinforcing the country's dominance in the regional seating industry.

Key players shaping this market include GRAMMER, RECARO Holding, Toyota Boshoku, Lear, MG Seating Systems, Adient, Magna International, Brose Sitech, Faurecia, and Fisher and Company. To maintain a competitive edge, leading automotive seating manufacturers focus on strategic moves such as R&D investments in sustainable and ergonomic materials, collaborations with OEMs, and regional manufacturing expansion. Many integrate digital technology and AI-enabled seating systems to elevate passenger experience, strengthen brand identity, and secure long-term contracts with top automakers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Distributors

- 3.1.1.5 OEMs

- 3.1.1.6 Technology integrators

- 3.1.1.7 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 Smart seating technologies

- 3.4.1.2 Integration with vehicle systems

- 3.4.1.3 Weight reduction technologies

- 3.4.1.4 Comfort enhancement technologies

- 3.4.2 Emerging Technologies

- 3.4.2.1 AI and Machine Learning Applications

- 3.4.2.2 IoT integration in seating systems

- 3.4.2.3 Biometric sensing and monitoring

- 3.4.2.4 Advanced material sciences

- 3.4.1 Current technological trends

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Consumer preferences and behavior

- 3.7.1 Comfort expectations

- 3.7.2 Demographic influences on seating preferences

- 3.7.3 Consumer perception of seating comfort

- 3.8 Price trend

- 3.8.1 Seat

- 3.8.2 Region

- 3.9 Cost breakdown analysis

- 3.10 Regulatory landscape

- 3.11 Impacting forces

- 3.11.1 Growth drivers

- 3.11.1.1 Integration of smart and connected seating technologies

- 3.11.1.2 Advancements in lightweight and sustainable materials

- 3.11.1.3 Growth in electric and autonomous vehicle interior reconfigurations

- 3.11.1.4 Enhanced safety features with sensor and airbag integrations

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Complexity in recycling polyurethane foams and composites

- 3.11.2.2 High development costs for advanced seat mechanisms

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seat, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Folding seat

- 5.3 Bucket seat

- 5.4 Bench seat

- 5.5 Split seat

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Standard

- 6.3 Powered

- 6.4 Ventilated

- 6.5 Climate-Controlled

- 6.6 Massage

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Genuine leather

- 7.3 Synthetic leather

- 7.4 Fabric

- 7.5 Sustainable

- 7.5.1 Recycled

- 7.5.2 Bio-based

- 7.5.3 Plant-derived

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCVs)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Frames

- 9.3 Foam padding

- 9.4 Seat adjuster

- 9.5 Headrests

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Internal combustion engine (ICE)

- 10.3 Electric vehicles (EVs)

- 10.4 Hybrid vehicles

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Original equipment manufacturers (OEMs)

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key Trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Southeast Asia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Adient

- 13.2 Brose Sitech

- 13.3 Camaco-Amvian

- 13.4 Dura Automotive Systems

- 13.5 Faurecia

- 13.6 Fisher and Company

- 13.7 Freedman Seating

- 13.8 GRAMMER

- 13.9 Guelph Manufacturing

- 13.10 Lear

- 13.11 Magna International

- 13.12 MG Seating Systems

- 13.13 NHK Spring

- 13.14 RECARO

- 13.15 TACHI-S

- 13.16 TM Systems

- 13.17 Toyota Boshoku

- 13.18 True Assistive Tech

- 13.19 TS Tech

- 13.20 Woodbridge