|

市場調查報告書

商品編碼

1750494

雲端電信 AI 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cloud Telecommunications AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

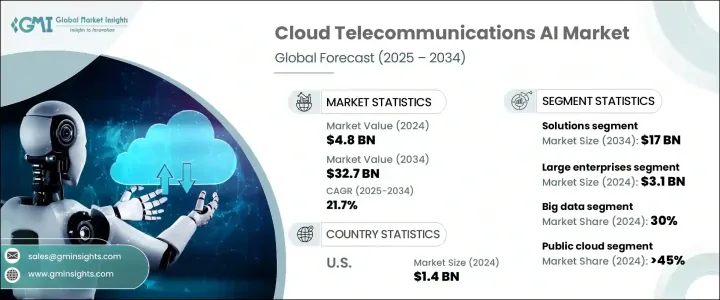

2024年,全球雲端電信人工智慧市場規模達48億美元,預計到2034年將以21.7%的複合年成長率成長,達到327億美元,這得益於電信業人工智慧與雲端技術的融合。隨著網路日益複雜,電信業者紛紛轉向人工智慧雲端解決方案,以更有效率地管理系統、提供無縫連接並最佳化客戶體驗。 5G的持續部署,加上智慧型裝置的廣泛應用,正在加速對智慧可擴展網路的需求。人工智慧雲端平台用於實現關鍵網路功能的自動化、最佳化資源分配,並降低動態網路環境中的延遲。

隨著營運商尋求能夠適應不斷變化的需求的靈活基礎設施,全球對基於雲端的電信人工智慧的投資不斷增加。數位轉型的推動力——以及近期全球疫情的衝擊——凸顯了對高彈性通訊系統的需求。人工智慧整合有助於管理資料密集型營運、預測維護需求並透過自動化降低營運成本。此外,對即時分析和機器學習模型的日益依賴,使得人工智慧成為轉型電信基礎設施以支援未來創新的基石。雲端架構與人工智慧的協同作用重新定義了電信營運商設計、營運和擴展其服務的方式。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 48億美元 |

| 預測值 | 327億美元 |

| 複合年成長率 | 21.7% |

2024年,解決方案細分市場佔據59%的市場佔有率,預計到2034年將達到170億美元。由於對用於增強網路可靠性和簡化內部工作流程的整合AI工具的需求不斷成長,該細分市場正日益受到關注。 AI驅動的平台被部署用於自動檢測故障、管理網路擁塞並即時最佳化頻寬。隨著資料量的增加,電信公司需要能夠解讀複雜流量模式並主動應對潛在中斷的系統。

大型企業細分市場在2024年引領市場,創造了31億美元的收入。企業高度依賴人工智慧技術來管理龐大的網路並支援龐大的用戶群。這些企業需要先進的自動化和預測能力,以提供穩定的性能並最大限度地減少停機時間。人工智慧能夠最佳化資源並更好地規劃基礎設施,尤其是在營運規模龐大且複雜性高的環境中。

2024年,美國雲端電信人工智慧市場佔最大佔有率,達23%。強勁的市場地位促使其對先進電信基礎設施進行大規模投資,尤其是在人工智慧整合和5G部署方面。聯邦機構大力支持數位轉型和智慧網路發展,進一步鞏固了美國的領先地位。公共和私營部門的合作加速了基於雲端的人工智慧技術的採用,重點是提高網路效率、即時分析和服務自動化。

SAP SE、Salesforce、騰訊、IBM、微軟、Nvidia、甲骨文、ATOS、Alphabet 和亞馬遜網路服務等公司正在推動人工智慧在電信領域的應用。該領域的公司正在實施一系列策略性舉措。許多公司正在擴展其全球雲端基礎設施,並提供針對電信應用量身定做的人工智慧即服務 (AI-as-a-service)。與電信業者的合作有助於提供客製化解決方案,以應對特定的網路挑戰。企業也透過收購、合資企業和內部創新來增強人工智慧能力,以強化其產品組合。此外,對邊緣運算、即時分析和跨平台整合的投資有助於這些企業在快速發展的市場環境中保持領先地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 核心AI組件提供者。

- 軟體和平台供應商

- 應用程式提供者

- 最終用戶

- 利潤率分析。

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組。

- 生產成本影響

- 需求面影響(售價)

- 價格傳輸至終端市場。

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 策略產業反應

- 供應鏈重組。

- 對貿易的影響

- 定價和產品策略

- 技術與創新格局

- 當前的技術趨勢

- 人工智慧驅動的網路最佳化

- 基於雲端的統一通訊(UCaaS)

- 5G邊緣運算

- 電信雲端編排和自動化

- 新興技術

- 電信網路的量子計算

- 融合人工智慧的6G網路

- 區塊鏈驅動的網路安全

- 智慧虛擬網路功能

- 先進材料科學

- 當前的技術趨勢

- 定價策略

- 專利分析

- 用例

- 重要新聞和舉措

- 監管格局

- 對部隊的影響

- 成長動力

- 5G網路擴展和人工智慧整合

- 邊緣運算的進步

- 改進的人工智慧預測性維護

- 雲端原生網路功能的進展

- 產業陷阱與挑戰

- 資料品質、治理與安全問題

- 人工智慧開發和部署的複雜性和人才缺口

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 解決方案

- 網路最佳化

- 網路安全

- 客戶分析

- 虛擬助手

- 詐欺偵測

- 預測性維護

- 其他

- 服務

- 專業服務

- 託管服務

- 諮詢與培訓

第6章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 機器學習

- 自然語言處理(NLP)

- 巨量資料

- 深度學習

- 其他

第7章:市場估計與預測:依組織規模,2021 - 2034 年

- 主要趨勢

- 中小企業(SME)

- 大型企業

第8章:市場估計與預測:按部署,2021 - 2034 年

- 主要趨勢

- 公共雲端

- 私有雲端

- 混合雲端

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 電信業者<

- 行動網路營運商 (MNO)

- 固定電話營運商

- 衛星營運商

- 網際網路服務供應商 (ISP)

- 寬頻網際網路服務供應商

- 無線 ISP

- 託管服務提供者 (MSP)

- 雲端服務供應商

- 網路管理供應商

第10章:市場估計與預測:按地區,2021 - 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Alibaba Cloud

- Altair Engineering

- Amazon Web Services (AWS)

- ATOS SE

- Avaamo

- Baidu

- Alphabet Inc

- Hewlett Packard Enterprise Development

- Huawei Cloud Computing Technologies

- IBM

- Intel

- Microsoft

- NICE Ltd.

- Nvidia

- Oracle

- Qualcomm Technologies

- SalesForce

- SAP SE

- Snowflake

- Tencent

The Global Cloud Telecommunications AI Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 32.7 billion by 2034, fueled by the convergence of artificial intelligence and cloud technologies within the telecom industry. As networks become more complex, telecom providers shift to AI cloud solutions to manage systems more efficiently, deliver seamless connectivity, and optimize customer experiences. The ongoing rollout of 5G, coupled with the widespread use of smart devices, is accelerating demand for intelligent, scalable networks. AI-powered cloud platforms are used to automate critical network functions, improve resource allocation, and reduce latency across dynamic network environments.

Global investments in cloud-based AI for telecom have intensified as operators seek flexible infrastructure capable of adapting to shifting demands. The push for digital transformation-amplified by recent global disruptions-has highlighted the need for highly resilient communication systems. AI integration helps manage data-heavy operations, predict maintenance needs, and cut operational costs through automation. Additionally, the growing reliance on real-time analytics and machine learning models makes AI a cornerstone in transforming telecom infrastructure to support future innovations. The synergy between cloud architecture and AI redefines how telecommunications providers design, operate, and scale their services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $32.7 Billion |

| CAGR | 21.7% |

In 2024, the solutions segment represented a 59% share and is projected to generate USD 17 billion by 2034. This segment is gaining traction due to rising demand for integrated AI tools that enhance network reliability and streamline internal workflows. AI-powered platforms are deployed to automate fault detection, manage network congestion, and optimize bandwidth in real time. As data volumes increase, telecoms need systems capable of interpreting complex traffic patterns and proactively addressing potential disruptions.

The large enterprises segment led the market in 2024, generating USD 3.1 billion. Enterprises rely heavily on AI technologies to manage expansive networks and support large user bases. These businesses require advanced automation and predictive capabilities to deliver consistent performance while minimizing downtime. AI enables resource optimization and better infrastructure planning, especially in environments where operational scale is vast and complexity is high.

United States Cloud Telecommunications AI Market held the largest share in 2024, accounting for 23%. This strong market position results in large-scale investments in advanced telecommunications infrastructure, particularly in AI integration and 5G deployment. The country's leadership is further solidified by robust support from federal agencies promoting digital transformation and smart network development. Public and private sector collaboration has accelerated the adoption of cloud-based AI technologies, focusing on enhancing network efficiency, real-time analytics, and service automation.

Companies like SAP SE, Salesforce, Tencent, IBM, Microsoft, Nvidia, Oracle, ATOS, Alphabet, and Amazon Web Services are advancing AI adoption in telecom. Companies in this space are implementing a range of strategic initiatives. Many are expanding their global cloud infrastructure and offering AI-as-a-service tailored for telecom applications. Collaborations with telecom providers are helping deliver customized solutions that address specific network challenges. Firms are also enhancing AI capabilities through acquisitions, joint ventures, and internal innovation to strengthen their offerings. Additionally, investment in edge computing, real-time analytics, and cross-platform integration helps these players stay ahead in a rapidly evolving landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model.

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Core AI component provider.

- 3.1.1.2 Software & platform vendors

- 3.1.1.3 Application provider

- 3.1.1.4 End users

- 3.1.2 Profit margin analysis.

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring.

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets.

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration.

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 AI-powered network optimization

- 3.4.1.2 Cloud-Based Unified Communications (UCaaS)

- 3.4.1.3 5G-enabled edge computing

- 3.4.1.4 Telecom cloud orchestration and automation

- 3.4.2 Emerging Technologies

- 3.4.2.1 Quantum computing for telecom networks

- 3.4.2.2 6G networks with ai integration

- 3.4.2.3 Blockchain-driven network security

- 3.4.2.4 Intelligent virtual network functions

- 3.4.3 Advanced material sciences

- 3.4.1 Current technological trends

- 3.5 Pricing strategies

- 3.6 Patent analysis

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 5G network expansion and ai integration

- 3.10.1.2 Advancements in edge computing

- 3.10.1.3 Improved AI-powered predictive maintenance

- 3.10.1.4 Progress in cloud-native network functions

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Data quality, governance, and security concerns

- 3.10.2.2 Complexity and talent gap in AI development and deployment

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Network optimization

- 5.2.2 Network security

- 5.2.3 Customer analytics

- 5.2.4 Virtual assistants

- 5.2.5 Fraud detection

- 5.2.6 Predictive maintenance

- 5.2.7 Others

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

- 5.3.3 Consulting & training

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Machine learning

- 6.3 Natural Language Processing (NLP)

- 6.4 Big data

- 6.5 Deep learning

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Small & Medium-sized Enterprises (SME)

- 7.3 Large Enterprises

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Public cloud

- 8.3 Private cloud

- 8.4 Hybrid cloud

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Telecom Operators<

- 9.2.1 Mobile Network Operators (MNOs)

- 9.2.2 Fixed line operators

- 9.2.3 Satellite operators

- 9.3 Internet Service Providers (ISPs)

- 9.3.1 Broadband ISPs

- 9.3.2 Wireless ISPs

- 9.4 Managed Service Providers (MSPs)

- 9.4.1 Cloud service providers

- 9.4.2 Network management providers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Sweden

- 10.2.8 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Alibaba Cloud

- 11.2 Altair Engineering

- 11.3 Amazon Web Services (AWS)

- 11.4 ATOS SE

- 11.5 Avaamo

- 11.6 Baidu

- 11.7 Alphabet Inc

- 11.8 Hewlett Packard Enterprise Development

- 11.9 Huawei Cloud Computing Technologies

- 11.10 IBM

- 11.11 Intel

- 11.12 Microsoft

- 11.13 NICE Ltd.

- 11.14 Nvidia

- 11.15 Oracle

- 11.16 Qualcomm Technologies

- 11.17 SalesForce

- 11.18 SAP SE

- 11.19 Snowflake

- 11.20 Tencent

機器學習即服務 (MLaaS) 市場分析及至 2035 年預測:按類型、產品、服務、技術、組件、應用、部署模式、最終用戶、解決方案和功能分類

機器學習即服務 (MLaaS) 市場分析及至 2035 年預測:按類型、產品、服務、技術、組件、應用、部署模式、最終用戶、解決方案和功能分類 機器學習即服務 (MLaaS):市場佔有率分析、產業趨勢與統計、成長預測 (2026-2031)

機器學習即服務 (MLaaS):市場佔有率分析、產業趨勢與統計、成長預測 (2026-2031) 全球機器學習服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球機器學習服務市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球雲端人工智慧(AI)市場,2025-2029年

全球雲端人工智慧(AI)市場,2025-2029年 全球雲端通訊人工智慧市場,2025-2029年

全球雲端通訊人工智慧市場,2025-2029年 機器學習即服務 (MaaS) 市場規模、佔有率和成長分析(按組件、組織規模、應用、最終用戶和地區分類)—2026-2033 年行業預測

機器學習即服務 (MaaS) 市場規模、佔有率和成長分析(按組件、組織規模、應用、最終用戶和地區分類)—2026-2033 年行業預測 機器學習即服務市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、組織規模、最終用戶、地區和競爭格局分類,2020-2030 年預測)

機器學習即服務市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、組織規模、最終用戶、地區和競爭格局分類,2020-2030 年預測) 2025-2029年全球人工智慧雲端解決方案市場

2025-2029年全球人工智慧雲端解決方案市場 2025-2029年全球雲端客服中心解決方案人工智慧市場

2025-2029年全球雲端客服中心解決方案人工智慧市場 全球電信業 AI 雲端基礎設施市場:預測(2024-2030年)

全球電信業 AI 雲端基礎設施市場:預測(2024-2030年)