|

市場調查報告書

商品編碼

1750480

敗血症治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Sepsis Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

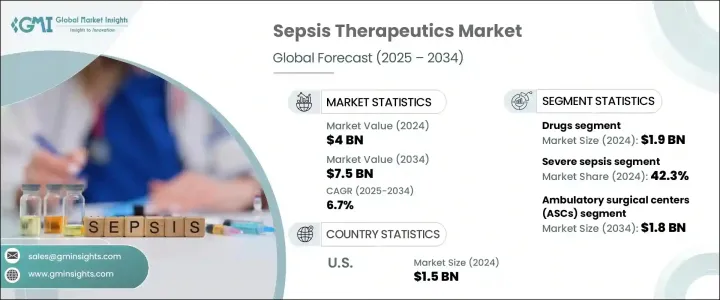

2024年,全球敗血症治療市場規模達40億美元,預計年複合成長率將達6.7%,2034年將達75億美元。敗血症是一種危及生命的疾病,由不受控制的感染免疫反應引發,需要立即進行針對性的醫療治療。當人體的防禦系統失控時,可能會損害健康組織並導致嚴重的器官衰竭。隨著全球醫院內感染負擔的不斷加重以及人口老化,對下一代療法的需求日益迫切。

全球醫療保健系統日益面臨提供及時精準敗血症治療的壓力,加劇了對下一代治療方案的追求。隨著敗血症發病率持續上升,製藥和生技公司正在加強研發投入,以期發現突破性療法。這種創新浪潮尤其體現在不斷成長的生物製劑和免疫療法研發管線中,這些藥物旨在調節人體免疫反應並提高患者存活率。由於傳統抗生素因抗菌素抗藥性而面臨局限性,對新型藥物和精準療法的需求空前高漲。臨床認知的進步,加上監管環境的支持,正在進一步加速敗血症治療策略的演變。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 40億美元 |

| 預測值 | 75億美元 |

| 複合年成長率 | 6.7% |

2024年,藥品領域收入達19億美元。抗生素、抗病毒藥物、抗真菌藥物、血管收縮劑和免疫調節劑仍然是敗血症管理的基礎。及時使用廣譜抗生素對於在治療早期對抗病原體至關重要。包括皮質類固醇和血管加壓素在內的支持療法可以穩定患者病情並減少全身性發炎。由於抗藥性導致膿毒症病例日益複雜,藥物開發商正致力於開發更具針對性的療法,以期取得更佳的臨床療效。

2024年,嚴重敗血症佔比42.3%。許多病例會迅速進展至這一關鍵階段,其特徵是廣泛的發炎和器官衰竭。這些臨床表現日益複雜,尤其是在抗藥性感染威脅日益加劇的背景下,這凸顯了對更有效、多標靶治療方案的需求。醫療保健提供者強調早期診斷和個人化醫療,以防止病情惡化並改善患者預後。

2024年,美國敗血症治療市場規模達15億美元。這一強勁成長得益於多種因素,包括老齡人口成長、醫院內感染率高以及醫療服務水平的持續改善。將人工智慧和機器學習融入敗血症診斷領域正日益受到關注,從而能夠更快、更準確地識別高風險患者。此外,積極的研發項目和對產品線拓展的高度重視鞏固了美國在該領域的領先地位。這些發展正在塑造一個未來,精準驅動、技術賦能的醫療服務將在敗血症管理中扮演核心角色。

在全球敗血症治療市場,各公司正採取以創新、臨床合作和產品線拓展為重點的策略,以鞏固其市場地位。北美和歐洲的參與者強調研究聯盟,以開發先進的生物製劑、下一代抗生素和免疫療法。輝瑞、羅氏和西普拉等公司正在投資新型給藥系統和人工智慧整合診斷平台,以加快敗血症的檢測和介入速度。許多公司,尤其是在亞太市場,正在進行II期和III期臨床試驗,以挖掘新興需求。在拉丁美洲、中東和非洲等敗血症治療缺口仍然巨大的市場,許可協議、合併和區域製造能力也日益受到關注。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 敗血症發生率上升

- 院內感染(HAI)的盛行率不斷上升

- 診斷和治療方案的技術進步

- 產業陷阱與挑戰

- 治療費用高昂

- 嚴格的法規核准

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按治療類型,2021 - 2034 年

- 主要趨勢

- 藥物

- 抗生素

- 抗病毒/抗真菌

- 其他藥物

- 靜脈輸液

- 氧氣療法

- 手術

- 其他治療類型

第6章:市場估計與預測:依疾病類型,2021 - 2034 年

- 主要趨勢

- 輕度敗血症

- 嚴重敗血症

- 感染性休克

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診所

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- Adrenomed

- Astellas Pharma

- Aurobindo Pharmaceuticals

- Aurora St. Luke's Medical Center

- Azurity Pharmaceuticals

- Bosch Pharmaceuticals

- Christiana hospitals

- Cipla

- Drive DeVilbiss Healthcare

- F. Hoffmann La Roche

- Medical Services Company

- Pfizer

- Torrent Pharmaceuticals

- West Virginia University Hospital

The Global Sepsis Therapeutics Market was valued at USD 4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 7.5 billion by 2034, driven by a life-threatening condition triggered by an unregulated immune reaction to infection, which requires immediate and targeted medical attention. When the body's defense system spirals out of control, it can damage healthy tissues and lead to severe organ failure. With the rising global burden of hospital-acquired infections and an aging population, there is an urgent need for next-generation therapies.

Healthcare systems worldwide are increasingly strained by the need to deliver timely and precise sepsis care, intensifying the push for next-generation treatment options. As the incidence of sepsis continues to rise, pharmaceutical and biotech companies are stepping up investments in research and development to discover breakthrough therapies. This surge in innovation is especially apparent in the growing pipeline of biologics and immunotherapies that aim to modulate the body's immune response and improve patient survival rates. With traditional antibiotics facing limitations due to antimicrobial resistance, the demand for novel drug classes and precision-based therapies has never been higher. Advancements in clinical understanding, combined with supportive regulatory environments, are further accelerating the evolution of sepsis treatment strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 6.7% |

In 2024, the drug segment generated USD 1.9 billion. Antibiotics, antivirals, antifungals, vasoconstrictors, and immunomodulators continue to be the foundation of sepsis management. Prompt administration of broad-spectrum antibiotics is essential to combat pathogens early in treatment. Supportive therapies, including corticosteroids and vasopressors, stabilize patients and reduce systemic inflammation. With sepsis cases becoming more complex due to drug resistance, pharmaceutical developers are focusing on more targeted therapies that can offer greater clinical outcomes.

In 2024, the severe sepsis segment held a 42.3% share. Many cases progress rapidly to this critical stage, characterized by extensive inflammation and organ failure. The increasing complexity of these clinical presentations, especially amid the growing threat of drug-resistant infections, underscores the need for more potent, multi-targeted therapeutic solutions. Healthcare providers emphasize early-stage diagnostics and personalized medicine to prevent escalation and improve patient outcomes.

United States Sepsis Therapeutics Market generated USD 1.5 billion in 2024. Several factors contribute to this robust performance, including a rising elderly population, a high rate of hospital-acquired infections, and continuous improvements in healthcare delivery. Integrating AI and machine learning in sepsis diagnostics is gaining traction, allowing for faster, more accurate identification of at-risk patients. Additionally, active R&D programs and a strong focus on expanding product pipelines reinforce the country's leadership in the field. These developments are shaping a future where precision-driven, technology-enabled care plays a central role in sepsis management.

In the Global Sepsis Therapeutics Market companies are adopting strategies focused on innovation, clinical partnerships, and pipeline expansion to solidify their position. Players in North America and Europe emphasize research alliances to develop advanced biologics, next-gen antibiotics, and immunotherapies. Firms such as Pfizer, F. Hoffmann-La Roche, and Cipla are investing in novel drug delivery systems and AI-integrated diagnostic platforms to speed up sepsis detection and intervention. Many companies are progressing through Phase II and III clinical trials, especially in the Asia Pacific market, to tap into emerging demand. Licensing agreements, mergers, and regional manufacturing capabilities are also gaining traction in markets like Latin America and the Middle East & Africa, where the sepsis treatment gap remains wide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidences of sepsis

- 3.2.1.2 Growing prevalence of hospital-acquired infections (HAIs)

- 3.2.1.3 Technological advancement in diagnostics and treatment options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antibiotics

- 5.2.2 Anti-viral/ Anti-fungal

- 5.2.3 Other drugs

- 5.3 I.V fluids

- 5.4 Oxygen therapy

- 5.5 Surgery

- 5.6 Other treatment types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Mild sepsis

- 6.3 Severe sepsis

- 6.4 Septic shock

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Adrenomed

- 9.3 Astellas Pharma

- 9.4 Aurobindo Pharmaceuticals

- 9.5 Aurora St. Luke’s Medical Center

- 9.6 Azurity Pharmaceuticals

- 9.7 Bosch Pharmaceuticals

- 9.8 Christiana hospitals

- 9.9 Cipla

- 9.10 Drive DeVilbiss Healthcare

- 9.11 F. Hoffmann La Roche

- 9.12 Medical Services Company

- 9.13 Pfizer

- 9.14 Torrent Pharmaceuticals

- 9.15 West Virginia University Hospital