|

市場調查報告書

商品編碼

1750452

軍用機器狗市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Military Robot Dogs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

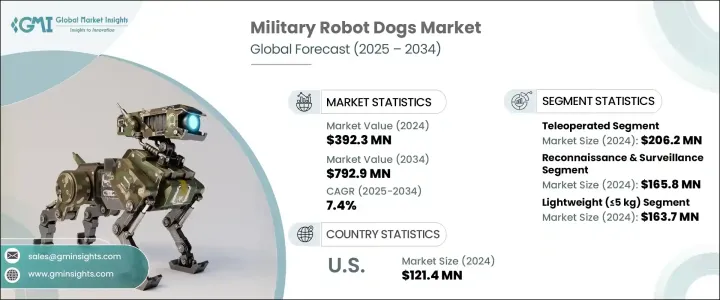

2024年,全球軍用機器狗市場價值為3.923億美元,預計到2034年將以7.4%的複合年成長率成長,達到7.929億美元,這得益於全球國防預算的不斷增加,以及對增強士兵安全和部隊防護技術日益成長的需求。軍用機器狗的研發備受關注,因為這些機器人可以執行偵察、監視和爆炸物處理 (EOD) 等關鍵任務。它們能夠在城市廢墟或化學-生物-放射-核 (CBRN) 區域等危險環境中行動,為軍事人員帶來巨大益處。

市場也受到貿易緊張等地緣政治因素的影響,導致某些海外零件的生產成本上升。這些干擾促使製造商考慮將生產轉移回國內並調整採購策略。由於國防承包商面臨著提陞技術能力的壓力,軍用機器狗開發商正專注於自主解決方案和針對特定任務的設計,以滿足現代戰爭不斷變化的需求。人們對網路中心戰日益成長的興趣進一步推動了機器狗的應用,這些機器狗可以整合到更大型的軍事系統中,從而實現戰場上的即時通訊和協調。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.923億美元 |

| 預測值 | 7.929億美元 |

| 複合年成長率 | 7.4% |

遙控系統在軍用機器狗市場佔據主導地位,2024 年市場價值達 2.062 億美元。這些系統提供手動控制,使操作員能夠在炸彈探測、人質救援和其他危險任務等高風險情況下遠端管理機器狗。這種能力降低了傷亡的可能性,確保了士兵在關鍵任務期間的安全。此外,與完全自主的機器狗相比,遙控機器狗的開發速度更快、成本更低,使其成為尋求經濟高效可靠方案的國防部隊的實用解決方案。它們能夠快速部署並用於即時作戰,這是它們仍然是軍事應用首選的主要原因之一,尤其是在快速反應至關重要的環境中。

就功能而言,軍用機器狗的偵察和監視領域在2024年創造了1.658億美元的市場規模。這些機器人配備了尖端技術,包括LiDAR、夜視技術和人工智慧光學系統,從而增強了它們即時探測和分析潛在威脅的能力。軍用機器狗能夠發現敵人的動向、簡易爆炸裝置或狙擊手,這在戰術行動中發揮著不可估量的作用。由於噪音低且視覺特徵清晰,它們具有隱蔽性,非常適合隱蔽行動,因為在隱蔽行動中,避免被發現至關重要。

2024年,德國軍用機器狗市場產值達2,220萬美元。德國的國防現代化戰略與北約的目標和歐洲國防合作一致,正在顯著推動機器人系統的普及。軍用機器狗擴大被用於邊境監視、跨境行動和快速反應任務,因為它們在具有挑戰性的地形中具有更強的機動性和多功能性。德國致力於技術創新和在PESCO和歐洲防務基金(EDF)等項目下的防務合作,為機器人解決方案在其國防行動中的整合創造了有利環境。

全球軍用機器狗產業的主要參與者包括波士頓動力公司 (Boston Dynamics)、宇樹機器人公司 (Unitree Robotics)、Addverb Technologies、Ghost Robotics 和 Deep Robotics。這些公司專注於增強機器人性能,整合尖端感測器,並提高其在惡劣環境下的可靠性和耐用性。此外,許多製造商正在強調自主任務專用系統,這些系統可以增強兵力,改善排爆作業 (EOD) 並支援後勤任務。透過投資研發並與國防機構合作,AeroArc 和西安超音速航空技術公司等公司正在鞏固其市場地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 關鍵零件價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 全球軍費開支不斷增加

- 人工智慧與機器視覺的融合

- 對士兵安全和部隊保護的需求不斷成長

- 城市戰爭場景的成長

- 增強戰術機動性

- 產業陷阱與挑戰

- 網路安全與駭客風險

- 電池壽命和續航限制

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按控制模式,2021 年至 2034 年

- 主要趨勢

- 遙控

- 完全自主

- 半自主

第6章:市場估計與預測:依酬載容量,2021 年至 2034 年

- 主要趨勢

- 輕便(≤5公斤)

- 中等體重(5-10公斤)

- 重型(>10 公斤)

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 偵察和監視

- 夜間巡邏

- 前瞻性觀察

- 在敵對地形進行隱身監視

- 戰鬥支援

- 搜救

- 爆炸物處理(EOD)

- 地雷探測

- CBRN環境評估

- 其他

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Addverb Technologies

- AeroArc

- Boston Dynamics

- Deep Robotics

- Edith Defense Systems

- Ghost Robotics

- Svaya Robotics

- Unitree Robotics

- Xian Supersonic Aviation Technology

The Global Military Robot Dogs Market was valued at USD 392.3 million in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 792.9 million by 2034, driven by the increasing defense budgets worldwide and the growing demand for technologies that enhance soldier safety and force protection. The development of military robot dogs has gained significant attention, as these robots can perform critical tasks such as reconnaissance, surveillance, and explosive ordnance disposal (EOD) operations. Their ability to operate in hazardous environments, including urban ruins or chemical-biological-radiological-nuclear (CBRN) zones, offers substantial benefits to military personnel.

The market is also influenced by geopolitical factors such as trade tensions, which have led to higher production costs for certain components sourced from overseas. These disruptions have prompted manufacturers to consider reshoring production and adjusting procurement strategies. As defense contractors are under pressure to enhance their technological capabilities, military robot dog developers are focusing on autonomous solutions and mission-specific designs to meet the evolving demands of modern warfare. The growing interest in network-centric warfare has further propelled the adoption of robot dogs that can be integrated into larger military systems, allowing for real-time communication and coordination on the battlefield.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $392.3 Million |

| Forecast Value | $792.9 Million |

| CAGR | 7.4% |

Teleoperated control systems dominate the military robot dogs market, valued at USD 206.2 million in 2024. These systems provide manual control, enabling operators to remotely manage robot dogs in high-risk situations like bomb detection, hostage rescue, and other hazardous missions. This capability reduces the potential for human casualties, ensuring soldiers' safety during critical tasks. Additionally, teleoperated robot dogs are quicker and more affordable to develop compared to their fully autonomous counterparts, making them a practical solution for defense forces looking for cost-effective and reliable options. Their ability to be swiftly deployed and used in real-time operations is one of the main reasons they remain the preferred choice for military applications, particularly in environments where rapid response is essential.

In terms of functionality, the reconnaissance and surveillance segment in military robot dogs generated USD 165.8 million in 2024. These robots are equipped with cutting-edge technologies, including LiDAR, night vision, and AI-powered optics, that enhance their ability to detect and analyze potential threats in real time. Military robot dogs can spot enemy movements, IEDs, or snipers, making them invaluable in tactical operations. Their stealthy nature, due to their low noise and visual signature, makes them perfect for covert operations, where avoiding detection is paramount.

Germany Military Robot Dogs Market generated USD 22.2 million in 2024. Germany's defense modernization strategy, in line with NATO's objectives and European defense collaborations, is significantly driving the adoption of robotic systems. Military robot dogs are increasingly being used for border surveillance, cross-border operations, and rapid-response missions, as they offer enhanced mobility and versatility in challenging terrains. Germany's commitment to technological innovation and defense cooperation under programs like PESCO and the European Defence Fund (EDF) has created a favorable environment for the integration of robotic solutions in its defense operations.

Key players in the Global Military Robot Dogs Industry include Boston Dynamics, Unitree Robotics, Addverb Technologies, Ghost Robotics, and Deep Robotics. These companies are focusing on enhancing robot capabilities, integrating cutting-edge sensors, and improving reliability and durability in harsh environments. Additionally, many manufacturers are emphasizing autonomous mission-specific systems that can provide force multiplication, improve EOD operations, and support logistics tasks. By investing in R&D and collaborating with defense organizations, companies like AeroArc and Xian Supersonic Aviation Technology are strengthening their positions in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising military expenditures globally

- 3.3.1.2 Integration of AI and machine vision

- 3.3.1.3 Growing demand for soldier safety and force protection

- 3.3.1.4 Growth in urban warfare scenarios

- 3.3.1.5 Enhanced tactical mobility

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Cybersecurity and hacking risks

- 3.3.2.2 Battery life and endurance limitations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Control Mode, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Teleoperated

- 5.3 Fully autonomous

- 5.4 Semi-autonomous

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Lightweight (≤5 kg)

- 6.3 Medium weight (5–10 kg)

- 6.4 Heavy duty (>10 kg)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Reconnaissance and surveillance

- 7.2.1 Night-time patrols

- 7.2.2 Forward observation

- 7.2.3 Stealth surveillance in hostile terrain

- 7.3 Combat Support

- 7.4 Search and rescue

- 7.5 Explosive ordnance disposal (EOD)

- 7.5.1 Mine detection

- 7.5.2 CBRN environment assessment

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Addverb Technologies

- 9.2 AeroArc

- 9.3 Boston Dynamics

- 9.4 Deep Robotics

- 9.5 Edith Defense Systems

- 9.6 Ghost Robotics

- 9.7 Svaya Robotics

- 9.8 Unitree Robotics

- 9.9 Xian Supersonic Aviation Technology

消費機器人市場:依產品類型、應用程式、最終用戶和通路分類-2026-2032年全球預測

消費機器人市場:依產品類型、應用程式、最終用戶和通路分類-2026-2032年全球預測 2026-2030年全球機器寵物狗市場

2026-2030年全球機器寵物狗市場 消費機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形狀、材質及最終用戶分類

消費機器人市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形狀、材質及最終用戶分類 2025-2029年全球人工智慧機器狗市場人工智慧仿生機器狗市場:按組件、自主程度、分銷管道、行動類型、應用和最終用戶分類——2026-2032年全球預測

2025-2029年全球人工智慧機器狗市場人工智慧仿生機器狗市場:按組件、自主程度、分銷管道、行動類型、應用和最終用戶分類——2026-2032年全球預測 消費機器人市場規模、佔有率和成長分析(按類型、組件、應用、連接方式和地區分類)-2026-2033年產業預測

消費機器人市場規模、佔有率和成長分析(按類型、組件、應用、連接方式和地區分類)-2026-2033年產業預測 全球人工智慧(AI)機器狗市場

全球人工智慧(AI)機器狗市場 全球消費機器人市場:市場規模(按類型、應用、連結方式和地區)、未來預測

全球消費機器人市場:市場規模(按類型、應用、連結方式和地區)、未來預測 消費機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、連接性、類型、地區和競爭,2019-2029F

消費機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、連接性、類型、地區和競爭,2019-2029F 2024-2028年全球消費機器人市場

2024-2028年全球消費機器人市場