|

市場調查報告書

商品編碼

1750360

前葡萄膜炎治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Anterior Uveitis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

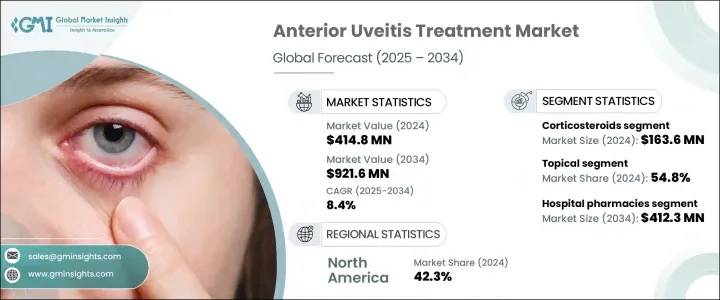

2024年,全球前葡萄膜炎治療市場規模達4.148億美元,預計到2034年將以8.4%的複合年成長率成長,達到9.216億美元。這得益於對前葡萄膜炎自體免疫和發炎機制的深入了解,這凸顯了早期和有針對性的醫療干預的必要性。診斷工具和影像技術的進步正在幫助臨床醫生做出更快、更準確的評估,從而加速治療決策。患者群體的擴大,加上自體免疫疾病和傳染病的增多,進一步刺激了對可靠治療方法的需求。

基因檢測和人工智慧輔助診斷等技術的進步正在為更個人化的治療方案鋪平道路,為醫療服務提供者和製造商帶來新的機會。這些創新能夠更準確地辨識患者的具體需求,進而改善治療效果。此外,全球人口老化,尤其是在美國,導致發炎性眼部疾病的發生率上升,這反過來又刺激了對老年患者需求的專門治療的需求。這種人口結構的變化凸顯了開發針對性治療方案以應對此類疾病日益成長的盛行率的重要性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.148億美元 |

| 預測值 | 9.216億美元 |

| 複合年成長率 | 8.4% |

2024年,皮質類固醇市場收入達1.636億美元。其強大的抗發炎特性和快速緩解症狀的能力,鞏固了其作為治療眼部發炎和預防危及視力併發症的一線治療藥物的地位。這些藥物用途廣泛,有全身性用藥和局部用藥兩種劑型,可根據發炎的嚴重程度和部位進行選擇。全身性用藥通常用於治療嚴重或後段炎症,而局部用藥仍是局部性前段疾病的首選方案。數十年的療效資料支持其廣泛的臨床應用,使其成為眼科護理的基石。

2024年,局部用皮質類固醇藥物的市佔率達到54.8%,反映出其在醫療保健提供者和患者中的日益普及。局部給藥具有局部治療效果,全身性吸收極少,與口服或注射劑型相比,顯著降低了不良反應的風險。這種給藥方式尤其適用於前葡萄膜炎和其他眼前部發炎性疾病,使用方便、緩解較快,且患者遵從性較高。各種劑量選擇和劑型(例如軟膏、凝膠和眼藥水)的出現,進一步提升了用藥的便利性,有助於提高依從性並改善患者療效。

2024年,美國前葡萄膜炎治療市場規模達1.595億美元。該國強大的醫療基礎設施和高發生率的自體免疫疾病,加劇了人們對眼部疾病的關注。皮質類固醇、免疫抑制劑和生物製劑等藥物仍然是治療方案的核心,而臨床研究也擴大探索基於生物製劑的新型治療方案。監管部門對遠距醫療和數位化工具的開放性,最佳化了患者獲得早期評估和持續護理的管道,增強了該地區的整體治療管道。

全球前葡萄膜炎治療市場的主要參與者包括輝瑞、Aldeyra Therapeutics、Tarsier Pharma、諾華、Clearside Biomedical、UCB、艾伯維、安進、Kiora Pharmaceuticals、愛爾康、EyePoint Pharmaceuticals、太陽製藥和參天製藥。為了鞏固其在前葡萄膜炎治療市場的地位,Clearside Biomedical、愛爾康和參天製藥等公司正在大力投資研發,以期更快地將創新療法推向市場。 EyePoint Pharmaceuticals 和安進等公司優先考慮先進的給藥技術,以提高治療效果並方便患者使用。包括輝瑞和諾華在內的大型製藥公司與生技創新者之間的合作已成為擴大治療組合的策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 提高對葡萄膜炎相關併發症的認知

- 診斷工具的技術進步

- 生物製劑和生物相似藥的開發

- 產業陷阱與挑戰

- 先進治療方案成本高昂

- 發展中地區醫療保健服務有限

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按治療類型,2021-2034

- 主要趨勢

- 皮質類固醇

- 睫狀肌麻痺劑

- 抗TNF藥物

- 免疫抑制劑

- 其他治療類型

第6章:市場估計與預測、管理途徑,2021-2034

- 主要趨勢

- 口服

- 外用

- 注射劑

第7章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 醫院藥房

- 零售藥局

- 網路藥局

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- AbbVie

- Alcon

- Aldeyra Therapeutics

- Amgen

- Clearside Biomedical

- EyePoint Pharmaceuticals

- Kiora Pharmaceuticals

- Novartis

- Pfizer

- Santen Pharmaceutical

- Sun Pharmaceutical Industries

- Tarsier Pharma

- UCB

The Global Anterior Uveitis Treatment Market was valued at USD 414.8 million in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 921.6 million by 2034, driven by deeper insights into the autoimmune and inflammatory underpinnings of anterior uveitis, which underscore the need for early and targeted medical intervention. Advancements in diagnostic tools and imaging technologies are helping clinicians make faster and more accurate assessments, which is accelerating treatment decisions. The expanding patient pool, linked to rising autoimmune and infectious diseases, further fuels demand for reliable therapeutic approaches.

Advancements in technologies such as genetic testing and AI-assisted diagnostics are paving the way for more personalized treatment options, offering new opportunities for both healthcare providers and manufacturers. These innovations allow for more accurate identification of specific patient needs, enhancing treatment outcomes. Furthermore, the aging global population, especially in the U.S., is driving a higher incidence of inflammatory eye conditions, which in turn is fueling the demand for specialized therapies tailored to meet the needs of older patients. This demographic shift underscores the importance of developing targeted treatments to address the growing prevalence of such conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $414.8 Million |

| Forecast Value | $921.6 Million |

| CAGR | 8.4% |

The corticosteroids segment generated USD 163.6 million in 2024. Their potent anti-inflammatory properties and ability to deliver rapid symptom relief have cemented their role as the first-line therapy for managing ocular inflammation and preventing vision-threatening complications. These drugs are versatile, available in systemic and topical formulations, and are selected based on the severity and location of inflammation. Systemic corticosteroids are commonly used for severe or posterior segment inflammation, while topical agents remain the go-to option for more localized anterior segment conditions. Their widespread clinical use is supported by decades of efficacy data, making them a cornerstone in ophthalmic care.

The topical corticosteroid segment held a 54.8% share in 2024, reflecting its growing preference among healthcare providers and patients. Topical administration offers a localized therapeutic effect with minimal systemic absorption, significantly lowering the risk of adverse reactions compared to oral or injectable forms. This delivery method is especially suitable for anterior uveitis and other front-of-eye inflammatory disorders, offering ease of use, faster relief, and better patient compliance. The availability of various dosing options and formulations, such as ointments, gels, and eye drops, has further enhanced convenience, contributing to higher adherence rates and improved patient outcomes.

United States Anterior Uveitis Treatment Market reached USD 159.5 million in 2024. The country's strong healthcare infrastructure and high prevalence of autoimmune disorders have amplified attention to ocular diseases. Pharmaceuticals such as corticosteroids, immunosuppressants, and biologics remain central to therapeutic protocols, while clinical research increasingly explores novel biologic-based options. Regulatory openness toward telehealth and digital tools optimizes patient access to early evaluations and ongoing care, strengthening the overall treatment pipeline in the region.

Prominent players active in the Global Anterior Uveitis Treatment Market include Pfizer, Aldeyra Therapeutics, Tarsier Pharma, Novartis, Clearside Biomedical, UCB, AbbVie, Amgen, Kiora Pharmaceuticals, Alcon, EyePoint Pharmaceuticals, Sun Pharmaceutical Industries, and Santen Pharmaceutical. To strengthen their position in the anterior uveitis treatment market, companies such as Clearside Biomedical, Alcon, and Santen Pharmaceutical are heavily investing in research and development to bring innovative therapies to market faster. Players like EyePoint Pharmaceuticals and Amgen prioritize advanced drug delivery technologies to boost treatment efficacy and patient convenience. Collaborations between large pharma firms, including Pfizer and Novartis, with biotech innovators have emerged as a strategy to expand therapeutic portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness about uveitis-related complications

- 3.2.1.2 Technological advancements in diagnostic tools

- 3.2.1.3 Development of biologics and biosimilars

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment options

- 3.2.2.2 Limited access to healthcare in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Cycloplegic agents

- 5.4 Anti-TNF agents

- 5.5 Immunosuppressants

- 5.6 Other treatment types

Chapter 6 Market Estimates and Forecast, Route of Administration, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Topical

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Alcon

- 9.3 Aldeyra Therapeutics

- 9.4 Amgen

- 9.5 Clearside Biomedical

- 9.6 EyePoint Pharmaceuticals

- 9.7 Kiora Pharmaceuticals

- 9.8 Novartis

- 9.9 Pfizer

- 9.10 Santen Pharmaceutical

- 9.11 Sun Pharmaceutical Industries

- 9.12 Tarsier Pharma

- 9.13 UCB