|

市場調查報告書

商品編碼

1750352

醫療設備校準服務市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Medical Equipment Calibration Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

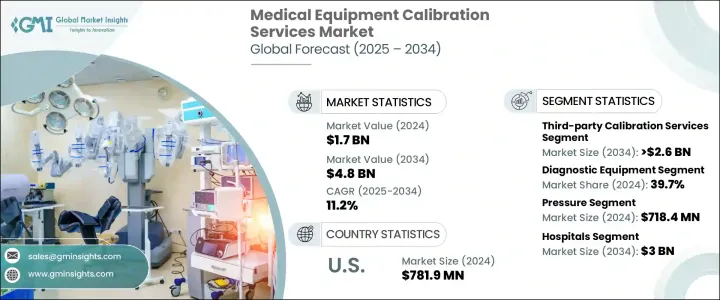

2024年,全球醫療設備校準服務市場規模達17億美元,預計到2034年將以11.2%的複合年成長率成長,達到48億美元。這主要得益於醫療設備對精度的迫切需求,以及醫療服務提供者在遵守不斷演變的監管標準方面面臨的日益成長的壓力。隨著高性能診斷和治療設備的使用日益廣泛,醫院和診所將校準視為優先事項,以保持可靠性並減少潛在錯誤。確保醫療工具的精準性能直接有助於改善患者治療效果,並滿足監管機構強制執行的品質基準。

隨著全球慢性病發病率持續上升,長期照護領域對經過適當校準的設備的需求也隨之激增。用於病患監護和疾病管理的設備必須性能卓越,因此校準服務對於減少診斷失誤至關重要。校準不足會危及病人安全,因此及時維護不僅是技術上的必要,也是醫療保健領域的策略要務。此外,影像和監護系統的進步需要更複雜的校準流程來維持功能並確保安全,從而提升了專業服務的價值。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 17億美元 |

| 預測值 | 48億美元 |

| 複合年成長率 | 11.2% |

第三方服務提供者因其無需內部能力即可提供靈活、經濟高效的解決方案而日益受到青睞。 2034年,第三方校準市場規模將達26億美元,複合年成長率達12.2%。許多醫療機構更傾向於與外部供應商合作,因為他們能夠為各種設備提供客製化的校準服務,同時幫助醫療機構遵守監管機構制定的準則。透過採用多供應商外包模式,醫療機構可以提高服務效率並簡化維護作業。

2024年,診斷設備佔最大佔有率,達39.7%。醫學影像領域對高精度系統的日益依賴,也提升了校準的需求。診斷設備需要頻繁且精確的調整才能保持最佳功能。監管要求進一步強調了校準的重要性,尤其是在醫療技術日益複雜,並整合了先進的軟體和自動化功能的情況下。

2024年,美國醫療設備校準服務市場規模達7.819億美元,其領先地位源自於嚴格的合規規範和先進醫療技術的廣泛應用。新設備的頻繁推出以及完善的監管框架,使得校準服務對於醫院、診斷實驗室和研究機構的持續臨床運作至關重要。

全球醫療設備校準服務市場的主要參與者——包括 Trescal、Fluke Biomedical、Transcat、Tektronix 和 SIMCO Electronics——正在推行多項策略舉措,以增強競爭優勢。許多公司透過收購和合作擴大地域覆蓋範圍,使其能夠提供在地化服務,同時滿足國際品質標準。各公司投資基於人工智慧的校準技術和自動追蹤系統,以提高準確性和效率。透過提供捆綁維護套餐和全天候服務契約,他們旨在深化客戶關係,並在服務密集型行業中脫穎而出。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 對醫療器材準確性和可靠性的要求日益提高

- 設備校準和合規性的嚴格監管要求

- 醫療機構擴大採用先進的醫療設備

- 醫療器材預防性維護計劃的成長

- 產業陷阱與挑戰

- 校準服務成本高昂,尤其是先進設備

- 校準任務所需的熟練人員有限

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 差距分析

- 波特的分析

- PESTEL分析

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按服務類型,2021 - 2034 年

- 主要趨勢

- 第三方校準服務

- 現場校準服務

- 實驗室校準服務

- OEM校準服務

第6章:市場估計與預測:按設備類型,2021 - 2034 年

- 主要趨勢

- 診斷設備

- 實驗室設備

- 治療設備

- 其他設備類型

第7章:市場估計與預測:按校準類型,2021 - 2034 年

- 主要趨勢

- 壓力

- 溫度

- 流動

- 其他校準類型

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診斷中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Advanced Instruments

- Agilent Technologies

- Allied Biomedical Services

- Ametek Test & Calibration

- Calibrationhouse

- Calyx

- Essco Calibration Lab

- Fluke Biomedical

- JM Test Systems

- MedEquip Biomedical

- SIMCO Electronics

- Technical Maintenance Inc.

- Tektronix

- Transcat

- Trescal

The Global Medical Equipment Calibration Services Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 11.2% to reach USD 4.8 billion by 2034, driven by the critical need for accuracy in medical devices and the increasing pressure on healthcare providers to remain compliant with evolving regulatory standards. With greater use of high-performance diagnostic and therapeutic equipment, hospitals and clinics are prioritizing calibration to maintain reliability and reduce potential errors. Ensuring precise performance in medical tools directly contributes to enhancing patient outcomes and meeting quality benchmarks enforced by regulatory authorities.

As the incidence of chronic illnesses continues to rise globally, the demand for properly calibrated devices used in long-term care also surges. Equipment used in patient monitoring and disease management must deliver performance, making calibration services vital in mitigating diagnostic mistakes. Inadequate calibration can compromise patient safety, which makes timely maintenance not only a technical necessity but also a strategic healthcare imperative. Moreover, advances in imaging and monitoring systems require more sophisticated calibration processes to maintain functionality and ensure safety, driving up the value of specialized services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 11.2% |

Third-party service providers are gaining popularity for offering flexible, cost-effective solutions without in-house capabilities. The third-party calibration segment generated USD 2.6 billion by 2034, growing at a CAGR of 12.2%. Many healthcare facilities prefer to work with external vendors, as they provide customized calibration for a wide range of devices while helping facilities stay compliant with guidelines set by regulatory bodies. By adopting a multi-vendor outsourcing model, healthcare organizations can enhance service efficiency and simplify their maintenance operations.

The diagnostic equipment held the largest share at 39.7% in 2024. Increasing reliance on high-precision systems in medical imaging has elevated the demand for calibration. Equipment used in diagnostic settings requires frequent and precise adjustments to maintain optimal function. Regulatory mandates further reinforce the importance of calibration, especially as medical technology becomes more complex and integrated with advanced software and automation features.

United States Medical Equipment Calibration Services Market generated USD 781.9 million in 2024, as the leadership stems from strict compliance norms and widespread adoption of advanced healthcare technologies. The frequent introduction of new devices and an established regulatory framework make calibration services essential for ongoing clinical operations across hospitals, diagnostic labs, and research institutions.

Key players in the Global Medical Equipment Calibration Services Market-including Trescal, Fluke Biomedical, Transcat, Tektronix, and SIMCO Electronics-are pursuing several strategic initiatives to enhance their competitive edge. Many are expanding their geographic presence through acquisitions and partnerships, enabling them to offer localized services while meeting international quality standards. Companies invest in AI-based calibration technologies and automated tracking systems to improve accuracy and efficiency. By offering bundled maintenance packages and 24/7 service contracts, they aim to deepen customer relationships and differentiate themselves in a service-intensive industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for accuracy and reliability in medical devices

- 3.2.1.2 Stringent regulatory requirements for device calibration and compliance

- 3.2.1.3 Rising adoption of advanced medical equipment in healthcare facilities

- 3.2.1.4 Growth in preventive maintenance programs for medical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of calibration services especially for advanced equipment

- 3.2.2.2 Limited availability of skilled personnel for calibration tasks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Service Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Third-party calibration services

- 5.3 On-site calibration services

- 5.4 Laboratory calibration services

- 5.5 OEM calibration services

Chapter 6 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic equipment

- 6.3 Laboratory equipment

- 6.4 Therapeutic equipment

- 6.5 Other equipment types

Chapter 7 Market Estimates and Forecast, By Calibration Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pressure

- 7.3 Temperature

- 7.4 Flow

- 7.5 Other calibration types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Instruments

- 10.2 Agilent Technologies

- 10.3 Allied Biomedical Services

- 10.4 Ametek Test & Calibration

- 10.5 Calibrationhouse

- 10.6 Calyx

- 10.7 Essco Calibration Lab

- 10.8 Fluke Biomedical

- 10.9 JM Test Systems

- 10.10 MedEquip Biomedical

- 10.11 SIMCO Electronics

- 10.12 Technical Maintenance Inc.

- 10.13 Tektronix

- 10.14 Transcat

- 10.15 Trescal

醫療設備校準服務市場-2026-2032年全球市場預測

醫療設備校準服務市場-2026-2032年全球市場預測 醫療設備校準服務市場規模、佔有率和成長分析:按服務類型、設備類型、應用、最終用戶、校準標準、服務供應商和地區分類-2026-2033年產業預測

醫療設備校準服務市場規模、佔有率和成長分析:按服務類型、設備類型、應用、最終用戶、校準標準、服務供應商和地區分類-2026-2033年產業預測 生命科學市場的驗證、校準和標準化

生命科學市場的驗證、校準和標準化 醫療設備校準服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、流程、最終用戶、安裝類型分類

醫療設備校準服務市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、流程、最終用戶、安裝類型分類 2025年全球醫療設備校準服務市場報告

2025年全球醫療設備校準服務市場報告 全球醫療設備第三方校準服務市場

全球醫療設備第三方校準服務市場 醫療設備校準服務市場(按服務類型、最終用戶和地區)

醫療設備校準服務市場(按服務類型、最終用戶和地區) 醫療設備第三方校準服務市場規模、佔有率、趨勢分析報告:按應用、按地區、細分市場預測,2024-2030 年

醫療設備第三方校準服務市場規模、佔有率、趨勢分析報告:按應用、按地區、細分市場預測,2024-2030 年