|

市場調查報告書

商品編碼

1750299

飛機窗戶與擋風玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Aircraft Windows and Windshields Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

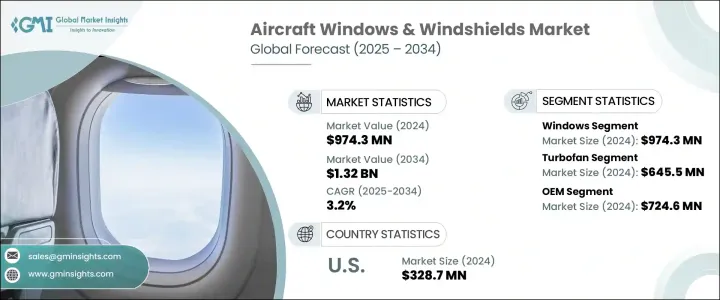

2024年,全球飛機窗和擋風玻璃市場價值達9.743億美元,預計到2034年將以3.2%的複合年成長率成長,達到13.2億美元。這得益於商用和公務飛機產量和部署量的不斷成長,以及對先進窗系統持續成長的需求。新型飛機平台和改裝正在推動向輕量化、抗衝擊材料的轉變,而乘客舒適度和能源效率仍然是新產品開發的重要考量。隨著產業適應更嚴格的監管準則,材料創新和不斷發展的空氣動力學正在塑造下一代設計。

近年來,貿易政策影響了製造業的策略。對鋁和特殊玻璃等關鍵原料徵收關稅導致生產成本上漲高達15%,尤其是在北美。這些轉變促使全球供應鏈重新調整,並為一些國際製造商創造了成本優勢。此外,售後市場供應商因依賴進口零件而面臨成本壓力。這種地緣政治緊張局勢加劇了整個供應和分銷網路的成本敏感性。材料科學的進步正在推動優質飛機窗戶和擋風玻璃的研發。聚碳酸酯層壓板、電致變色調光系統和石墨烯塗層等技術因能夠提高極端條件下的性能而日益受到重視。自修復薄膜、嵌入式感測器和智慧著色功能在最佳化能源利用的同時,也改變了客艙體驗。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 9.743億美元 |

| 預測值 | 13.2億美元 |

| 複合年成長率 | 3.2% |

按產品類別細分,飛機窗戶細分市場在2024年創造了9.743億美元的市場規模。這些部件不僅注重可視性,還能應付極端壓力差、溫度變化和衝擊等情況。該行業正在穩步轉向先進的聚碳酸酯基替代品,以減輕飛機重量並提高燃油效率,同時又不損害結構彈性。儘管由於航空管理局的嚴格標準,這項轉型需要高昂的研發和認證成本,但這些投資因其性能、生命週期可靠性和法規合規性的提升而物有所值。

2024年,飛機窗戶和擋風玻璃市場中的渦輪扇引擎市場價值為6.455億美元,因為高性能多層窗戶能夠承受劇烈的溫度梯度、高海拔壓力以及潛在的鳥類撞擊。許多新一代飛機都使用內建除冰和溫度調節功能的先進擋風玻璃,以確保飛行員的視野和駕駛艙的安全。隨著機隊規模的擴大,原始設備製造商(OEM)的出貨量正在成長,而由於舊機型擋風玻璃更換和升級的需求不斷成長,售後市場仍然活躍。

由於關鍵製造中心、龐大的機隊以及完善的維護、維修和大修 (MRO) 生態系統,美國飛機窗和擋風玻璃市場規模在 2024 年達到 3.287 億美元。軍事採購計劃以及嚴格的聯邦航空管理局 (FAA) 合規標準,持續推動國防和商業領域對耐用、輕質、技術先進的材料的需求。

全球飛機窗與擋風玻璃市場的領導者包括聖戈班航太、NORDAM 集團、GENTEX 公司、GKN航太和 PPG 工業公司。飛機窗與擋風玻璃市場的主要參與者正在透過技術合作、設施擴建和材料創新來鞏固其地位。各公司大力投資可提高舒適度和性能的智慧窗系統,尤其是在高階和防禦領域。與 OEM 的策略合作有助於確保產品儘早整合到新平台中,而開發抗衝擊、輕量化解決方案的努力有助於滿足嚴格的 FAA 和 EASA 要求。主要製造商本地化供應鏈以減輕關稅影響並縮短交貨時間。研發仍然是一項核心策略,公司專注於電光升級、防冰增強和新型複合結構,以降低生命週期成本和重量。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 增加飛機交付量和擴大機隊規模

- 材料和塗層的技術進步

- 國防和軍用飛機現代化程度不斷提高

- 售後市場需求受車隊老化和維護、修理和大修 (MRO) 成長推動

- 產業陷阱與挑戰

- 認證成本高

- 供應鏈中斷

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 視窗

- 擋風玻璃

第6章:市場估計與預測:依飛機類型,2021-2034

- 主要趨勢

- 渦輪螺旋槳

- 渦輪風扇

- 渦輪噴射

- 渦輪軸

第7章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- OEM

- 售後市場

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Control Logistics Inc

- GENTEX CORPORATION

- GKN Aerospace

- Lee Aerospace

- Llamas Plastics Inc.

- LP Aero Plastics Inc.

- Perkins Aircraft Windows

- PPG Industries, Inc.

- Saint-Gobain Aerospace

- The NORDAM Group LLC

The Global Aircraft Windows and Windshields Market was valued at USD 974.3 million in 2024 and is estimated to grow at a CAGR of 3.2% to reach USD 1.32 billion by 2034, driven by the rising production and deployment of both commercial and business aircraft with sustained demand for advanced window systems. New aircraft platforms and retrofits are driving the shift toward lightweight, impact-resistant materials, while passenger comfort and energy efficiency remain essential considerations in new product development. As the industry adapts to stricter regulatory guidelines, material innovations and evolving aerodynamics are shaping next-generation designs.

Trade policies have influenced manufacturing strategies in recent years. The introduction of tariffs on critical raw materials like aluminium and specialty glass led to production cost hikes of up to 15%, particularly in North America. These shifts prompted a realignment of global supply chains and created cost advantages for some international manufacturers. Additionally, aftermarket vendors saw cost pressures due to their reliance on imported components. Such geopolitical tensions have intensified cost sensitivities across the supply and distribution network. Advancements in material science are propelling the development of superior aircraft windows and windshields. Technologies such as polycarbonate laminates, electrochromic dimming systems, and graphene-infused coatings are gaining prominence for enhancing performance in extreme conditions. Self-healing films, embedded sensors, and smart-tinting functions transform cabin experiences while optimizing energy use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $974.3 Million |

| Forecast Value | $1.32 Billion |

| CAGR | 3.2% |

In the product category breakdown, the aircraft windows segment generated USD 974.3 million in 2024. These components are engineered not only for visibility but also to handle extreme pressure differentials, temperature shifts, and impact scenarios. The industry is steadily shifting toward advanced polycarbonate-based alternatives to lighten aircraft weight and enhance fuel efficiency, without compromising structural resilience. While the transition demands high R&D and certification costs due to strict aviation authority standards, these investments are justified by improvements in performance, lifecycle reliability, and regulatory compliance.

The turbofan segment in the aircraft windows & windshields market was valued at USD 645.5 million in 2024 as high-performance, multi-layered windows withstand severe thermal gradients, high-altitude pressures, and potential bird impacts. Many new-generation aircraft use advanced windshields with built-in de-icing and thermal regulation features to ensure pilot visibility and cockpit safety. As fleets expand, OEM shipments are gaining momentum, while the aftermarket remains active due to increasing demand for windshield replacements and upgrades in older airframes.

United States Aircraft Windows & Windshields Market reached USD 328.7 million in 2024, owing to key manufacturing hubs, large aircraft fleets, and a solid maintenance, repair, and overhaul (MRO) ecosystem. Military procurement programs, along with rigorous FAA compliance standards, continue to drive the demand for durable, lightweight, and technically advanced materials across both defense and commercial sectors.

Leading players in the Global Aircraft Windows & Windshields Market include Saint-Gobain Aerospace, The NORDAM Group LLC, GENTEX Corporation, GKN Aerospace, and PPG Industries, Inc. Key players in the aircraft windows & windshields market are strengthening their positions through technology partnerships, facility expansions, and material innovation. Companies invest heavily in smart window systems that enhance comfort and performance, especially in the premium and defense segments. Strategic collaborations with OEMs help ensure early integration of products into new platforms, while efforts to develop impact-resistant, lightweight solutions help meet strict FAA and EASA requirements. Major manufacturers localize supply chains to mitigate tariff impacts and improve lead times. R&D remains a core strategy, with firms focusing on electro-optic upgrades, anti-icing enhancements, and new composite structures that reduce lifecycle costs and weight.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing aircraft deliveries and fleet expansion

- 3.3.1.2 Technological advancements in materials and coatings

- 3.3.1.3 Rising defense and military aircraft modernization

- 3.3.1.4 Aftermarket demand driven by aging fleets and MRO growth

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High certification costs

- 3.3.2.2 Supply chain disruptions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Windows

- 5.3 Windshields

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Turboprop

- 6.3 Turbofan

- 6.4 Turbojet

- 6.5 Turboshaft

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Control Logistics Inc

- 9.2 GENTEX CORPORATION

- 9.3 GKN Aerospace

- 9.4 Lee Aerospace

- 9.5 Llamas Plastics Inc.

- 9.6 LP Aero Plastics Inc.

- 9.7 Perkins Aircraft Windows

- 9.8 PPG Industries, Inc.

- 9.9 Saint-Gobain Aerospace

- 9.10 The NORDAM Group LLC