|

市場調查報告書

商品編碼

1750285

土聚物水泥市場機會、成長動力、產業趨勢分析及2025-2034年預測Geopolymer Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

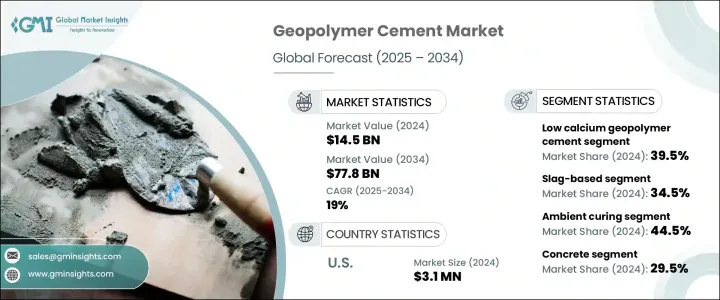

2024 年全球土聚物水泥市場規模為 145 億美元,預計到 2034 年將以 19% 的複合年成長率成長至 778 億美元。隨著建築業轉向環保實踐,低排放材料的吸引力持續成長。這一趨勢在很大程度上受到應對氣候變遷和遵守不斷發展的環境法規日益緊迫的影響。隨著各國政府推出更嚴格的永續發展規定,各行各業都在積極尋求更乾淨、更高性能的傳統建築材料替代品。土聚物水泥因其低碳足跡而脫穎而出,與傳統波特蘭水泥相比,其碳排放量可減少高達 90%。它不僅提供了更永續的解決方案,還具有卓越的機械和化學性能,使其成為基礎設施建設的首選。各行各業都在推動脫碳,這推動了對支持長期生態目標的創新材料的需求,而土聚物水泥憑藉其能源效率和減少對原始原料的依賴而符合這一要求。

除了監管壓力之外,全球城市化進程的加速也推動了對耐用且經濟高效的建築材料的需求。隨著世界各地,尤其是發展中國家的快速發展,對交通網路、商業空間和住宅項目的投資也激增。土聚物水泥因其滿足現代建築的技術和環境要求而日益受到市場青睞。其耐極端天氣條件和持久耐用性使其特別適用於高應力應用。永續建築規範的日益普及以及綠建築激勵措施的訂定,進一步支持了市場擴張。隨著各行各業和政府尋求符合循環經濟目標的可靠替代方案,土聚物水泥正逐漸成為市場領跑者。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 145億美元 |

| 預測值 | 778億美元 |

| 複合年成長率 | 19% |

成本效益是該材料日益普及的關鍵因素。土聚物水泥利用粉煤灰和高爐礦渣等工業廢料,降低了總生產成本,同時最大限度地減少了生產過程中的能耗。這些原料通常來自其他工業流程,從而形成了一個支持永續發展目標的閉迴路系統。除了較低的生產成本外,該材料還具有出色的耐熱性和耐化學性,使其成為滿足各種建築需求的經濟環保的選擇。

2024年,低鈣土聚物水泥佔了最高的市場佔有率,佔全球收入的39.5%。此類水泥主要來自粉煤灰,以其優異的耐熱性、化學穩定性和較低的環境影響而聞名。這些特性使其成為極端條件下高性能應用的首選。在原料方面,粉煤灰基和礦渣基水泥合計佔據了整個市場的34.5%。這些材料不僅易於獲取,而且具有優異的抗壓強度和長期耐久性。利用這些材料有助於減少垃圾掩埋和溫室氣體排放,符合全球永續發展目標。

固化技術顯著影響土聚物水泥的性能和適用性。 2024年,常溫固化佔據主導地位,市佔率為44.5%。這種方法因其能耗低、工藝簡便而備受青睞,是一般建築和維護工作的理想選擇。對於時間緊迫或結構要求高的項目,熱固化是首選,因為它可以提高強度並縮短凝固時間。這兩種技術都可根據項目規格靈活調整,從而拓寬了材料在各個領域的適用性。

從應用角度來看,混凝土以29.5%的市佔率領先市場。土聚物混凝土具有優異的強度、低收縮性和高耐化學性,使其成為大型專案的首選材料。其符合綠色建築標準,這增加了對尋求LEED認證或類似永續發展資質的承包商和開發商的吸引力。建築和施工產業是2024年最大的終端使用產業,佔了整個市場的34.5%。它在住宅、商業和工業環境中的廣泛應用凸顯了該材料的適應性以及在環保建築實踐中日益成長的重要性。

從地區來看,美國已成為領先市場,2024 年市場規模達 310 億美元,佔全球佔有率的 80% 以上。美國強勁的市場地位得益於不斷成長的基礎設施投資、嚴格的環境準則以及對永續發展日益成長的承諾。粉煤灰和礦渣等原料的便利取得也支持了美國國內的生產和應用,從而減少了供應鏈挑戰並降低了碳排放。由於優惠的政策和永續建築材料的技術進步,美國市場持續成長。

土聚物水泥市場的領導者正大力投入研發,以改善配方並提升產品性能。這些企業專注於專有技術和新一代製造程序,旨在提供一致的品質並提升應用靈活性。他們不斷創新,同時拓展分銷網路,這使其能夠滿足多樣化的客戶需求,並在不斷變化的全球格局中保持競爭優勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 市場介紹

- 川普政府關稅的影響—結構化概述

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳輸至終端市場。

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計資料(HS 編碼) 註:以上貿易統計僅提供重點國家。

- 主要出口國

- 主要進口國

- 產業價值鏈分析

- 利潤率分析

- 產品概述

- 地質聚合物化學與形成

- 與波特蘭水泥的比較

- 環境效益和碳足跡

- 機械性能和性能特徵

- 耐久性和抵抗性

- 凝固時間和可加工性

- 限制和挑戰

- 市場動態

- 市場促進因素

- 環境法規和永續發展措施。

- 基礎設施建設不斷成長,尤其是在新興經濟體。

- 與傳統水泥相比具有成本優勢,包括減少二氧化碳排放和能源消耗。

- 市場限制

- 煤炭、鋼鐵等重點業經營狀況下滑。

- 某些應用領域的技術限制,限制了更廣泛的使用。

- 承包商和建築商缺乏意識和技術知識。

- 市場機會

- 越來越重視綠建築材料。

- 對耐用和高效能基礎設施解決方案的需求不斷成長。

- 地質聚合物配方的技術進步。

- 市場挑戰

- 標準化和認證問題。

- 來自現有水泥類型的競爭。

- 與傳統水泥具有成本競爭力。

- 市場促進因素

- 產業衝擊力

- 成長潛力分析

- 產業陷阱與挑戰

- 監管框架和標準

- 建築規範及施工標準

- 環境法規

- 碳定價與排放交易

- 綠建築認證

- 廢棄物利用政策

- 製造流程分析

- 原料準備

- 鹼性活化劑生產

- 混合和配方

- 固化方法

- 品質控制程式

- 原料分析與採購策略

- 定價分析

- 永續性和環境影響評估

- 杵分析

- 波特五力分析

第4章:競爭格局

- 市佔率分析

- 戰略框架

- 併購

- 合資與合作

- 新產品開發

- 擴張策略

- 競爭基準測試

- 供應商格局

- 競爭定位矩陣

- 戰略儀表板

- 專利分析與創新評估

- 新參與者的市場進入策略

- 研發強度分析

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 低鈣土聚水泥

- 高鈣土聚水泥

- 磷酸鹽基土聚物水泥

- 矽酸鹽基土聚物水泥

- 其他

第6章:市場估計與預測:依原料來源,2021 - 2034 年

- 主要趨勢

- 粉煤灰基

- F級粉煤灰

- C類粉煤灰

- 其他粉煤灰類型

- 礦渣基

- 磨細粒化高爐礦渣(GGBFS)

- 其他礦渣類型

- 偏高嶺土基

- 天然鋁矽酸鹽基

- 赤泥基

- 混合系統

- 其他

第7章:市場估計與預測:按固化方法,2021 - 2034 年

- 主要趨勢

- 室溫固化

- 熱固化

- 蒸氣養護

- 其他

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 具體的

- 預拌混凝土

- 預製混凝土

- 其他具體應用

- 砂漿和灌漿

- 預製構件

- 積木和磚塊

- 板材和板坯

- 管道和柱子

- 其他預製構件

- 路面和覆蓋層

- 修復與康復

- 廢物封裝和固定化

- 其他應用

第9章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 建築與施工

- 住宅

- 商業的

- 工業的

- 基礎設施

- 道路和橋樑

- 水壩和水資源管理

- 機場和港口

- 其他基礎設施

- 石油和天然氣

- 礦業

- 海洋與水下建築

- 核與廢料管理

- 其他

第10章:市場估計與預測:按性能屬性,2021 - 2034 年

- 主要趨勢

- 高強度

- 耐化學性

- 防火

- 低收縮

- 快速設定

- 其他性能屬性

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第12章:公司簡介

- Alchemy Geopolymer Solutions, LLC

- Banah UK Ltd.

- BASF SE

- CEMEX SAB de CV

- Ceratech Inc.

- Concrete Canvas Ltd.

- Dow Chemical Company

- GCP Applied Technologies Inc.

- Geobeton Pty Ltd.

- Geopolymer Products

- Geopolymer Solutions, LLC

- Halliburton

- Imerys SA

- Kiran Global Chems Limited

- LafargeHolcim Ltd.

- Metna Co.

- Milliken Infrastructure Solutions, LLC

- Nu-Core

- PCI Augsburg GmbH

- Pyromeral Systems

- Reno Refractories, Inc.

- Rocla Pty Limited

- Schlumberger Limited

- Sika AG

- Siloxo Pty Ltd.

- Tech-Crete Processors Ltd.

- Uretek Worldwide

- Wagners

- Wollner GmbH

- Zeobond Pty Ltd.

The Global Geopolymer Cement Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 19% to reach USD 77.8 billion by 2034. As the construction industry shifts toward environmentally responsible practices, the appeal of low-emission materials continues to grow. This trend is largely influenced by the increasing urgency to combat climate change and comply with evolving environmental regulations. As governments introduce stricter sustainability mandates, industries are actively seeking cleaner, high-performance alternatives to traditional construction materials. Geopolymer cement stands out in this regard due to its low carbon footprint, generating up to 90% fewer carbon emissions compared to conventional Portland cement. It offers not only a more sustainable solution but also superior mechanical and chemical properties, making it a preferred choice in infrastructure development. The push for decarbonization across sectors is driving demand for innovative materials that support long-term ecological goals, and geopolymer cement fits the bill with its energy efficiency and reduced reliance on virgin raw materials.

In addition to regulatory pressures, rising global urbanization is fueling the need for durable and cost-effective building materials. As development accelerates in various parts of the world, especially in growing economies, investment in transport networks, commercial spaces, and residential projects is surging. Geopolymer cement is gaining market traction as it meets both the technical and environmental demands of modern construction. Its resistance to extreme weather conditions and long-lasting durability make it particularly suitable for high-stress applications. The increasing adoption of sustainable building codes and incentives for green construction is further supporting market expansion. As industries and governments seek reliable alternatives that align with circular economy goals, geopolymer cement is emerging as a frontrunner.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $77.8 Billion |

| CAGR | 19% |

Cost efficiency plays a crucial role in the material's growing popularity. Geopolymer cement leverages industrial waste products like fly ash and blast furnace slag, which reduces the overall production cost while also minimizing energy consumption during manufacturing. These raw materials are often sourced from other industrial processes, creating a closed-loop system that supports sustainability goals. Alongside its lower production expenses, the material delivers excellent resistance to heat and chemicals, making it an economically and environmentally viable option for a wide range of construction needs.

In 2024, low calcium geopolymer cement captured the highest market share, accounting for 39.5% of global revenue. This type is primarily derived from fly ash and is recognized for its strong thermal resistance, chemical stability, and reduced environmental impact. These attributes make it a preferred choice in applications requiring high performance under extreme conditions. On the raw material front, the combined share of fly ash-based and slag-based segments reached 34.5% of the total market. These materials are not only readily accessible but also deliver excellent compressive strength and long-term durability. Their utilization contributes to reducing landfill waste and greenhouse gas emissions, aligning with global sustainability targets.

Curing techniques significantly influence the performance and applicability of geopolymer cement. In 2024, ambient curing held the dominant position, with a market share of 44.5%. This method is favored for its low energy requirement and simplified process, which makes it ideal for general construction and maintenance work. For time-sensitive or structurally demanding projects, heat curing is preferred as it enhances strength and reduces setting time. Both techniques offer flexibility depending on project specifications, broadening the material's applicability across sectors.

From an application perspective, concrete led the market with a 29.5% share. Geopolymer concrete offers excellent strength, low shrinkage, and high chemical resistance, making it a go-to material for large-scale projects. Its compliance with green building standards adds to its appeal among contractors and developers seeking LEED certifications or similar sustainability credentials. The building and construction sector represented the largest end-use industry in 2024, holding 34.5% of the total market. Its widespread use in residential, commercial, and industrial settings highlights the material's adaptability and growing importance in eco-conscious construction practices.

Regionally, the United States emerged as the leading market, valued at USD 3.1 million in 2024 and accounting for over 80% of the global share. The country's strong position is supported by rising infrastructure investment, strict environmental guidelines, and a growing commitment to sustainable development. Easy access to raw materials such as fly ash and slag also supports domestic production and adoption, reducing supply chain challenges and lowering carbon impact. The US market continues to grow due to favorable policies and technological advancements in sustainable building materials.

Leading companies in the geopolymer cement market are investing heavily in research and development to refine formulations and improve product performance. By focusing on proprietary technologies and next-generation manufacturing methods, these players aim to deliver consistent quality and enhance application flexibility. Their efforts to innovate while expanding distribution networks are enabling them to address varied customer needs and maintain a competitive edge in an evolving global landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Methodology

- 1.2 Research Objectives

- 1.3 Market Definition and Scope

- 1.4 Market Segmentation

- 1.5 Data Sources

- 1.5.1 Primary Research

- 1.5.2 Secondary Research

- 1.6 Market Estimation Approach

- 1.7 Research Assumptions and Limitations

- 1.8 Base Year and Forecast Period

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Segment Highlights

- 2.3 Competitive Landscape Snapshot

- 2.4 Regional Market Outlook

- 2.5 Key Market Trends

- 2.6 Future Market Outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets.

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Industry value chain analysis

- 3.5 Profit margin analysis

- 3.6 Product overview

- 3.6.1 Geopolymer chemistry & formation

- 3.6.2 Comparison with Portland cement

- 3.6.3 Environmental benefits & carbon footprint

- 3.6.4 Mechanical properties & performance characteristics

- 3.6.5 Durability & resistance properties

- 3.6.6 Setting time & workability

- 3.6.7 Limitations & challenges

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Environmental regulations and sustainability initiatives.

- 3.7.1.2 Growing infrastructure development, particularly in emerging economies.

- 3.7.1.3 Cost advantages over traditional cement, including reduced CO2 emissions and energy consumption.

- 3.7.2 Market restraints

- 3.7.2.1 Declining operations in key industries like coal and steel.

- 3.7.2.2 Technical limitations in certain applications, restricting wider use.

- 3.7.2.3 Lack of awareness and technical knowledge among contractors and builders.

- 3.7.3 Market opportunities

- 3.7.3.1 Increasing focus on green building materials.

- 3.7.3.2 Rising demand for durable and high-performance infrastructure solutions.

- 3.7.3.3 Technological advancements in geopolymer formulations.

- 3.7.4 Market challenges

- 3.7.4.1 Standardization and certification issues.

- 3.7.4.2 Competition from established cement types.

- 3.7.4.3 Cost competitiveness with conventional cement.

- 3.7.1 Market drivers

- 3.8 Industry impact forces

- 3.8.1 Growth potential analysis

- 3.8.2 Industry pitfalls & challenges

- 3.9 Regulatory framework & standards

- 3.9.1 Building codes & construction standards

- 3.9.2 Environmental regulations

- 3.9.3 Carbon Pricing & Emissions Trading

- 3.9.4 Green building certifications

- 3.9.5 Waste material utilization policies

- 3.10 Manufacturing process analysis

- 3.10.1 Raw material preparation

- 3.10.2 Alkaline activator production

- 3.10.3 Mixing & formulation

- 3.10.4 Curing methods

- 3.10.5 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Research & development intensity analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Low calcium geopolymer cement

- 5.3 High calcium geopolymer cement

- 5.4 Phosphate-based geopolymer cement

- 5.5 Silicate-based geopolymer cement

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Raw Material Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fly Ash-Based

- 6.2.1 Class F fly ash

- 6.2.2 Class C fly ash

- 6.2.3 Other fly ash types

- 6.3 Slag-Based

- 6.3.1 Ground granulated blast furnace slag (GGBFS)

- 6.3.2 Other slag types

- 6.4 Metakaolin-based

- 6.5 Natural aluminosilicate-based

- 6.6 Red mud-based

- 6.7 Hybrid & blended systems

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Curing Method, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ambient curing

- 7.3 Heat curing

- 7.4 Steam curing

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Concrete

- 8.2.1 Ready-mix concrete

- 8.2.2 Precast concrete

- 8.2.3 Other concrete applications

- 8.3 Mortar & grouts

- 8.4 Precast elements

- 8.4.1 Blocks & bricks

- 8.4.2 Panels & slabs

- 8.4.3 Pipes & columns

- 8.4.4 Other precast elements

- 8.5 Pavements & overlays

- 8.6 Repair & rehabilitation

- 8.7 Waste encapsulation & immobilization

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Building & construction

- 9.2.1 Residential

- 9.2.2 Commercial

- 9.2.3 Industrial

- 9.3 Infrastructure

- 9.3.1 Roads & bridges

- 9.3.2 Dams & water management

- 9.3.3 Airports & ports

- 9.3.4 Other infrastructure

- 9.4 Oil & gas

- 9.5 Mining

- 9.6 Marine & underwater construction

- 9.7 Nuclear & waste management

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 High strength

- 10.3 Chemical resistance

- 10.4 Fire resistance

- 10.5 Low shrinkage

- 10.6 Rapid setting

- 10.7 Other performance attributes

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Alchemy Geopolymer Solutions, LLC

- 12.2 Banah UK Ltd.

- 12.3 BASF SE

- 12.4 CEMEX S.A.B. de C.V.

- 12.5 Ceratech Inc.

- 12.6 Concrete Canvas Ltd.

- 12.7 Dow Chemical Company

- 12.8 GCP Applied Technologies Inc.

- 12.9 Geobeton Pty Ltd.

- 12.10 Geopolymer Products

- 12.11 Geopolymer Solutions, LLC

- 12.12 Halliburton

- 12.13 Imerys S.A.

- 12.14 Kiran Global Chems Limited

- 12.15 LafargeHolcim Ltd.

- 12.16 Metna Co.

- 12.17 Milliken Infrastructure Solutions, LLC

- 12.18 Nu-Core

- 12.19 PCI Augsburg GmbH

- 12.20 Pyromeral Systems

- 12.21 Reno Refractories, Inc.

- 12.22 Rocla Pty Limited

- 12.23 Schlumberger Limited

- 12.24 Sika AG

- 12.25 Siloxo Pty Ltd.

- 12.26 Tech-Crete Processors Ltd.

- 12.27 Uretek Worldwide

- 12.28 Wagners

- 12.29 Wollner GmbH

- 12.30 Zeobond Pty Ltd.

2026年高容量飛灰混凝土全球市場報告

2026年高容量飛灰混凝土全球市場報告 無機聚合物材料市場:依原料、產品類型、製造流程和應用分類-2026年至2032年全球市場預測2026年全球無機聚合物混凝土市場報告2026年全球無機聚合物水泥市場報告

無機聚合物材料市場:依原料、產品類型、製造流程和應用分類-2026年至2032年全球市場預測2026年全球無機聚合物混凝土市場報告2026年全球無機聚合物水泥市場報告 無機聚合物:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

無機聚合物:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球無機聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球無機聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 無機聚合物市場報告:按應用、最終用途產業和地區分類(2026-2034 年)2026年全球無機聚合物市場報告日本無機聚合物市場規模、佔有率、趨勢及預測(按應用、終端用戶產業及地區分類),2026-2034年

無機聚合物市場報告:按應用、最終用途產業和地區分類(2026-2034 年)2026年全球無機聚合物市場報告日本無機聚合物市場規模、佔有率、趨勢及預測(按應用、終端用戶產業及地區分類),2026-2034年 無機聚合物市場規模、佔有率和成長分析(按產品類型、應用、物理形態、最終用途和地區分類)-2026-2033年產業預測

無機聚合物市場規模、佔有率和成長分析(按產品類型、應用、物理形態、最終用途和地區分類)-2026-2033年產業預測