|

市場調查報告書

商品編碼

1750272

持續性膀胱沖洗設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Continuous Bladder Irrigation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

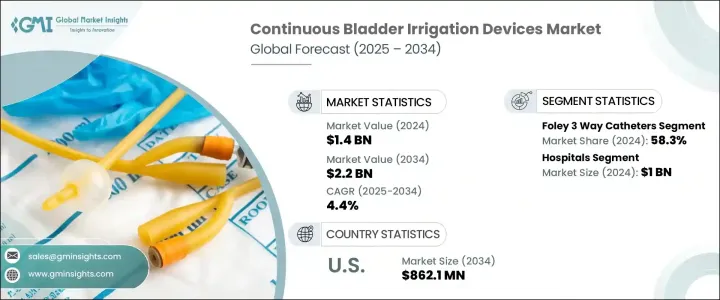

2024年,全球持續性膀胱沖洗裝置市場規模達14億美元,預計到2034年將以4.4%的複合年成長率成長,達到22億美元,這主要得益於膀胱癌、血尿和良性前列腺增生 (BPH) 等泌尿系統疾病的日益流行。醫療保健提供者致力於減少併發症並改善患者康復,持續膀胱沖洗系統 (CBI) 已成為醫院和臨床環境中不可或缺的設備。這些系統在泌尿外科手術後的術後護理中尤其重要,因為它們有助於預防血栓形成並維持導管功能。

導管材料、設計和沖洗輸送系統的技術進步顯著改變了持續性膀胱沖洗 (CBI) 設備的功能和可靠性。防扭結導管、壓力控制流動機制以及改進的球囊設計等創新技術提高了患者的安全性,並方便了臨床醫生的使用。這些進步有助於更好地控制尿流、減少導管阻塞並提高血塊管理的有效性。此外,現代 CBI 系統還融入了可最大限度降低污染風險的功能,從而支持醫院減少導管相關尿路感染 (CAUTI) 的努力。如今,醫療保健方案高度重視標準化的沖洗操作,因此,先進的 CBI 設備已成為術後和長期泌尿科護理中維持患者預後的關鍵組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 22億美元 |

| 複合年成長率 | 4.4% |

2024年,Foley三通導尿管佔據最大市場佔有率,達58.3%,反映出其在術後出血管理和導管通暢維護方面的廣泛應用。這些導尿管具有沖洗、球囊擴張和尿液引流功能,是治療複雜泌尿系統疾病不可或缺的工具。除了術後應用外,這些導尿管還用於治療創傷性膀胱損傷、化療引起的膀胱炎和其他尿瀦留併發症,從而擴大了其在全球醫療保健領域的應用。

2024年,醫院領域在持續膀胱沖洗設備市場中佔據最大佔有率,因為膀胱腫瘤切除術和前列腺手術等手術頻率較高,需要持續沖洗以防止血栓滯留。隨著對減少導管相關泌尿道感染 (CAUTI) 的關注度日益提高,醫院正在增加對先進持續性膀胱沖洗系統 (CBI) 的投資,以確保病患安全和手術成功率。持續膀胱沖洗在最大程度減少術後併發症方面發揮著重要作用,已成為住院泌尿科護理的標準操作。

美國持續性膀胱沖洗設備市場規模預計將在2024年達到5.693億美元,這主要得益於美國老齡人口的成長,前列腺肥大、膀胱癌和血尿的發病率不斷上升,而這些疾病通常需要長期沖洗。這一人口趨勢直接導致了膀胱相關手術(例如經尿道手術)的增加,這些手術需要可靠的術後沖洗。醫院和外科中心優先考慮耐用、抗感染且易於維護的高品質沖洗系統。

康德樂 (Cardinal Health)、CR Bard、Sterimed、百特 (Baxter)、Advin Health Care、Teleflex、Angiplast、HEMC、Medline、Bactiguard、波士頓科學 (Boston Scientific)、Coloplast、AdvaCare、B. Braun 和 Vogt Medical 等主要參與者正在採取有針對性的策略來提升市場有佔有率。這些策略包括導管材料的產品創新、與醫療機構的策略合作以及向新興市場的擴張。各公司也強調感染控制功能,提供可客製化的解決方案,並投資研發以滿足監管標準並改善護理效果。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 泌尿系統疾病盛行率上升

- 導管材料和灌溉技術的進步

- 微創泌尿外科手術的採用日益增多

- 老年人口不斷增加

- 產業陷阱與挑戰

- 導管相關泌尿道感染的風險

- 中低收入國家缺乏認知,獲得先進泌尿科護理的機會有限

- 成長動力

- 成長潛力分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 川普政府關稅的前景和未來考慮

- 對貿易的影響

- 未來市場趨勢

- 監管格局

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 競爭儀錶板

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- Foley三通導管

- 矽膠導管

- 乳膠導管

- 配件

- 灌溉套裝

- 滾輪夾

- 奧特萊斯包

- 灌溉袋

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 長期照護機構

- 其他最終用途

第7章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- AdvaCare

- Advin Health Care

- Angiplast

- B. Braun

- Bactiguard

- Baxter

- Boston Scientific

- CR Bard

- Cardinal Health

- Coloplast

- HEMC

- Medline

- Sterimed

- Teleflex

- Vogt Medical

The Global Continuous Bladder Irrigation Devices Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 2.2 billion by 2034, driven by the increasing prevalence of urological conditions such as bladder cancer, hematuria, and benign prostatic hyperplasia (BPH). As healthcare providers aim to reduce complications and improve patient recovery, CBI systems have become essential in hospitals and clinical settings. These systems are particularly vital during post-operative care following urologic surgeries, as they help prevent clot formation and maintain catheter function.

Technological progress in catheter materials, design, and irrigation delivery systems has significantly transformed the functionality and reliability of continuous bladder irrigation (CBI) devices. Innovations such as anti-kink tubing, pressure-controlled flow mechanisms, and improved balloon designs have enhanced patient safety and clinician ease-of-use. These advancements contribute to better control of urine flow, reduced catheter blockages, and more effective clot management. Additionally, modern CBI systems incorporate features that minimize the risk of contamination, supporting hospitals' efforts to reduce catheter-associated urinary tract infections (CAUTIs). Healthcare protocols now place a strong emphasis on standardized irrigation practices, as a result, advanced CBI devices have become a critical component in maintaining patient outcomes in post-operative and long-term urological care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 4.4% |

Foley 3-way catheters held the largest market share at 58.3% in 2024, reflecting their widespread adoption in managing post-surgical bleeding and maintaining catheter patency. These catheters are capable of irrigation, balloon inflation, and urine drainage, making them indispensable in treating complex urological conditions. Beyond their post-operative use, these catheters are also utilized in trauma-related bladder injuries, chemotherapy-induced cystitis, and other urinary retention complications, which have widened their application in healthcare worldwide.

The Hospitals segment in the continuous bladder irrigation devices market held the largest share in 2024 due to the high frequency of procedures like bladder tumor resections and prostate surgeries, which require consistent irrigation to prevent blood clot retention. With an increasing focus on reducing catheter-associated urinary tract infections (CAUTIs), hospitals are investing more in advanced CBI systems that support patient safety and surgical success. The role of continuous bladder irrigation in minimizing post-surgical complications has made it a standard element in inpatient urological care.

United States Continuous Bladder Irrigation Devices Market is expected to reach USD 569.3 million in 2024, driven by the country's expanding elderly population is experiencing higher rates of prostate enlargement, bladder cancer, and hematuria-conditions that often require long-term irrigation solutions. This demographic trend has directly contributed to an increase in bladder-related surgeries, such as transurethral procedures, which require reliable post-surgical irrigation. Hospitals and surgical centers prioritize high-quality irrigation systems that offer durability, infection resistance, and ease of maintenance.

Key players such as Cardinal Health, C. R. Bard, Sterimed, Baxter, Advin Health Care, Teleflex, Angiplast, HEMC, Medline, Bactiguard, Boston Scientific, Coloplast, AdvaCare, B. Braun, and Vogt Medical are adopting focused strategies to enhance market presence. These include product innovation in catheter materials, strategic partnerships with healthcare institutions, and expansion into emerging markets. Companies are also emphasizing infection-control features, offering customizable solutions, and investing in R&D to meet regulatory standards and improve care outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of urological disorders

- 3.2.1.2 Advancements in catheter materials and irrigation technologies

- 3.2.1.3 Growing adoption of minimally invasive urological procedures

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of catheter-associated urinary tract infections

- 3.2.2.2 Lack of awareness and limited access to advanced urological care in LMICs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations trump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive dashboard

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Foley 3 way catheters

- 5.2.1 Silicone catheters

- 5.2.2 Latex catheters

- 5.3 Accessories

- 5.3.1 Irrigation set

- 5.3.2 Roller clamp

- 5.3.3 Outlet bags

- 5.4 Irrigation bags

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Long term care facilities

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Mexico

- 7.5.2 Brazil

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AdvaCare

- 8.2 Advin Health Care

- 8.3 Angiplast

- 8.4 B. Braun

- 8.5 Bactiguard

- 8.6 Baxter

- 8.7 Boston Scientific

- 8.8 C. R. Bard

- 8.9 Cardinal Health

- 8.10 Coloplast

- 8.11 HEMC

- 8.12 Medline

- 8.13 Sterimed

- 8.14 Teleflex

- 8.15 Vogt Medical