|

市場調查報告書

商品編碼

1750270

半導體整流器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Semiconductor Rectifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

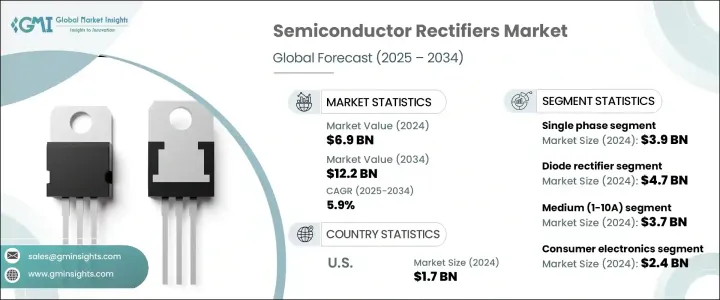

2024年,全球半導體整流器市場規模達69億美元,預計到2034年將以5.9%的複合年成長率成長,達到122億美元,這得益於全球消費性電子產品消費的成長以及再生能源部署的激增。清潔能源系統中產生直流電的設備需要將直流電轉換為交流電——而整流器在電源逆變器和轉換器中發揮至關重要的作用。

然而,貿易政策——尤其是川普政府時期對從中國進口的半導體元件徵收的關稅——給全球供應鏈帶來了巨大的動盪。這些關稅不僅增加了進口成本,還對整個產業產生了連鎖反應,包括定價不一致、產品部署週期延長以及利潤率壓縮。為此,許多製造商開始多元化其供應商網路,並探索近岸外包策略以最大限度地降低風險。雖然其目的是刺激國內生產並減少對進口的依賴,但短期後果是市場波動加劇,市場勢頭放緩,生產計劃也變得複雜。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 69億美元 |

| 預測值 | 122億美元 |

| 複合年成長率 | 5.9% |

根據產品細分,單相整流器市場在2024年創造了39億美元的市場規模。由於其處理低功耗轉換的效率高、體積小巧,並且易於整合到標準化電路設計中,單相整流器在消費性電子產品和家用電器中得到了廣泛的應用。其價格實惠、靈活性高,使其成為大眾市場應用的理想選擇,這些應用注重成本和簡潔性,同時又不犧牲性能。

同時,二極體整流器以其類型領先,2024 年估值達 47 億美元。由於其簡約的設計和高能效,這些元件仍然是各種中低功率系統不可或缺的一部分。它們在再生能源基礎設施(包括太陽能逆變器和電動車充電器)中的應用日益廣泛,凸顯了它們在擴展需要可靠性和空間效率的下一代電源解決方案方面發揮的作用。

2024年,美國半導體整流器市場產值達17億美元,這得益於其成熟的工業基礎,支撐著航太、國防和電信等依賴高性能、長壽命電子元件的產業。聯邦政府推出的激勵措施進一步鞏固了美國半導體製造業的領先地位,旨在增強關鍵技術領域的自力更生能力,並緩解地緣政治供應中斷的影響。

全球半導體整流器市場的主要參與者,包括德州儀器、安森美半導體、意法半導體、英飛凌科技、瑞薩電子和東芝,正在採取多管齊下的策略來鞏固其市場地位。這些公司投資研發,以提高整流器技術的效率並縮小其尺寸。在貿易條件有利的地區,製造能力的擴張也正在進行中。 ABB 和恩智浦半導體等公司正在進行策略合作,以拓寬其應用組合,而微芯科技和 IXYS 則正在探索人工智慧整合電源解決方案。此外,羅姆半導體和三菱電機等公司專注於垂直整合和地理多元化,以降低供應鏈風險並確保在高需求領域穩定交付。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 關鍵零件價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 消費性電子產品需求不斷成長

- 汽車電氣化日益發展

- 擴大再生能源基礎設施

- 5G和下一代通訊網路

- 資料中心和雲端運算的激增

- 產業陷阱與挑戰

- 先進整流器的初始成本較高

- 熱管理和可靠性問題

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 單相

- 三相

第6章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 二極體整流器

- 閘流管整流器

第7章:市場估計與預測:按功率等級,2021 - 2034 年

- 主要趨勢

- 低(小於 1 A)

- 中(1-10 A)

- 高(超過 10 A)

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 汽車

- 消費性電子產品

- 電力和公用事業

- IT和電信

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- ABB

- ASI semiconductor

- Infineon technologies

- IXYS

- Microchip technology

- Mitsubishi electric

- NXP semiconductor

- ON semiconductor

- Renesas electronics

- Rohm semiconductor

- STMicroelectronics

- Taiwan semiconductor

- Texas instruments

- Toshiba

The Global Semiconductor Rectifiers Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 12.2 billion by 2034, fueled by increasing global consumption of consumer electronics and a surge in renewable energy deployment. Devices generating direct current in clean energy systems require conversion to alternating current-an area where rectifiers play a crucial role in power inverters and converters.

However, trade policies- notably the tariffs imposed on semiconductor components imported from China during the Trump administration-introduced substantial turbulence into the global supply chain. These tariffs not only increased import costs but also caused ripple effects across the industry, including inconsistent pricing, prolonged product deployment cycles, and squeezed profit margins. As a response, many manufacturers began diversifying their supplier networks and exploring nearshoring strategies to minimize risk. While the intent was to stimulate domestic production and reduce reliance on imports, the short-term consequence was a period of volatility that slowed market momentum and complicated production planning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.9% |

Based on product segmentation, single-phase rectifiers segment generated USD 3.9 billion in 2024. Their extensive use in consumer electronics and residential setups stems from their efficiency in handling low-power conversions, compact footprint, and ease of integration into standardized circuit designs. Their affordability and flexibility make them an ideal fit for mass-market applications that prioritize cost and simplicity without sacrificing performance.

Meanwhile, diode rectifiers led by type with a valuation of USD 4.7 billion in 2024. These components remain integral to a broad range of low-to-mid power systems due to their minimalistic design and high energy efficiency. Their growing use in renewable energy infrastructure, including solar power inverters and electric vehicle chargers, underscores their role in scaling next-generation power solutions that demand reliability and space efficiency.

United States Semiconductor Rectifiers Market generated USD 1.7 billion in 2024, attributed to a mature industrial base that supports sectors like aerospace, defense, and telecommunications-industries that depend on high-performance and long-lasting electronic components. Further boosting this leadership are federal incentives promoting domestic semiconductor fabrication, which aim to enhance self-reliance in critical technology areas and mitigate geopolitical supply disruptions.

Key players in the Global Semiconductor Rectifiers Market, including Texas Instruments, ON Semiconductor, STMicroelectronics, Infineon Technologies, Renesas Electronics, and Toshiba, are adopting multi-pronged strategies to reinforce their market position. These companies invest in R&D to enhance efficiency and reduce form factor in rectifier technologies. Expansion of manufacturing capacities in regions with favorable trade conditions is also underway. Firms like ABB and NXP Semiconductor are entering strategic collaborations to broaden their application portfolios, while Microchip Technology and IXYS are exploring AI-integrated power solutions. Additionally, players like Rohm Semiconductor and Mitsubishi Electric focus on vertical integration and geographic diversification to mitigate supply chain risks and ensure stable delivery in high-demand sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for consumer electronics

- 3.3.1.2 Growing electrification of automobiles

- 3.3.1.3 Expansion of renewable energy infrastructure

- 3.3.1.4 5G and next-gen communication networks

- 3.3.1.5 Surge in data centres and cloud computing

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial cost of advanced rectifiers

- 3.3.2.2 Thermal management and reliability issues

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Billion & Billion Units)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Billion Units)

- 6.1 Key trends

- 6.2 Diode rectifiers

- 6.3 Thyristor rectifiers

Chapter 7 Market Estimates and Forecast, By Power Rating, 2021 - 2034 (USD Billion & Billion Units)

- 7.1 Key trends

- 7.2 Low (less than 1 A)

- 7.3 Medium (1-10 A)

- 7.4 High (over 10 A)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Billion Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Power and utility

- 8.5 It and telecom

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Billion Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 ASI semiconductor

- 10.3 Infineon technologies

- 10.4 IXYS

- 10.5 Microchip technology

- 10.6 Mitsubishi electric

- 10.7 NXP semiconductor

- 10.8 ON semiconductor

- 10.9 Renesas electronics

- 10.10 Rohm semiconductor

- 10.11 STMicroelectronics

- 10.12 Taiwan semiconductor

- 10.13 Texas instruments

- 10.14 Toshiba

整流變壓器組市場:以相數、冷卻方式、頻率、輸出電壓、額定功率、應用和最終用戶分類-全球預測,2026-2032年SiC肖特基二極體市場按應用、額定電壓、額定電流、封裝和最終用途分類,全球預測(2026-2032年)乾式移相整流變壓器市場按冷卻方式、相數、類型、額定電壓、最終用戶和應用分類-全球預測,2026-2032年

整流變壓器組市場:以相數、冷卻方式、頻率、輸出電壓、額定功率、應用和最終用戶分類-全球預測,2026-2032年SiC肖特基二極體市場按應用、額定電壓、額定電流、封裝和最終用途分類,全球預測(2026-2032年)乾式移相整流變壓器市場按冷卻方式、相數、類型、額定電壓、最終用戶和應用分類-全球預測,2026-2032年 感應爐整流變壓器市場規模、佔有率和成長分析:按變壓器類型、額定功率、冷卻方式、電壓等級、爐容量、應用和地區分類-2026-2033年產業預測矽肖特基二極體整流器市場(依元件類型、額定電壓、額定電流、封裝類型和應用分類)-全球預測,2026-2032年

感應爐整流變壓器市場規模、佔有率和成長分析:按變壓器類型、額定功率、冷卻方式、電壓等級、爐容量、應用和地區分類-2026-2033年產業預測矽肖特基二極體整流器市場(依元件類型、額定電壓、額定電流、封裝類型和應用分類)-全球預測,2026-2032年 裸晶晶片碳化矽肖特基二極體市場規模、佔有率和成長分析:按產品類型、晶粒尺寸、應用、終端用戶產業和地區分類-2026-2033年產業預測

裸晶晶片碳化矽肖特基二極體市場規模、佔有率和成長分析:按產品類型、晶粒尺寸、應用、終端用戶產業和地區分類-2026-2033年產業預測 半導體整流器市場規模、佔有率、成長及全球產業分析:依類型、額定電壓、最終用途、應用和地區劃分的洞察與預測(2026-2034年)SiC肖特基整流二極體市場按元件類型、封裝類型、額定電流、額定電壓、分配通道、材料類型、晶圓尺寸和最終用途行業分類 - 全球預測 2026-2032整流變壓器市場:按相數、輸出類型、冷卻方式、容量範圍和應用分類 - 全球預測(2026-2032 年)肖特基整流二極體市場按類型、極性、額定電流、正向電壓和應用分類-2026年至2032年全球預測

半導體整流器市場規模、佔有率、成長及全球產業分析:依類型、額定電壓、最終用途、應用和地區劃分的洞察與預測(2026-2034年)SiC肖特基整流二極體市場按元件類型、封裝類型、額定電流、額定電壓、分配通道、材料類型、晶圓尺寸和最終用途行業分類 - 全球預測 2026-2032整流變壓器市場:按相數、輸出類型、冷卻方式、容量範圍和應用分類 - 全球預測(2026-2032 年)肖特基整流二極體市場按類型、極性、額定電流、正向電壓和應用分類-2026年至2032年全球預測