|

市場調查報告書

商品編碼

1750267

真空卡車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Vacuum Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

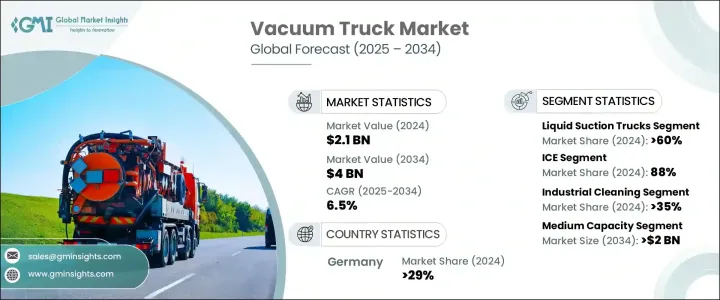

2024年,全球真空卡車市場價值為21億美元,預計到2034年將以6.5%的複合年成長率成長,達到40億美元,這得益於城鎮化進程加快和工業快速發展,尤其是在新興經濟體。這些車輛對於處理固體和液體廢物、下水道維護以及各行各業的清潔作業至關重要。隨著城市發展和基礎設施擴張,公共和私人實體擴大使用真空卡車來有效清除廢物並進行衛生清潔。採礦、建築和能源等工業部門也依賴真空卡車來處理洩漏物、污泥和危險材料,這進一步凸顯了該車輛在現代廢棄物管理生態系統中的重要性。

全球範圍內訂定的更嚴格的環境法規促使市政當局和各行各業紛紛採用真空吸污車來滿足污染控制要求。這些車輛提供了一種安全運輸危險和非危險材料的方法,不會污染環境。它們在確保化學品、公用事業和石油等行業的安全合規性方面發揮著日益重要的作用。隨著環境標準的不斷發展,人們對技術先進、性能更佳、排放更低、安全性更高的真空吸污車的興趣日益濃厚。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 21億美元 |

| 預測值 | 40億美元 |

| 複合年成長率 | 6.5% |

液體吸污卡車市場在2024年佔據了60%的市場佔有率,預計到2034年將達到20億美元。這一成長主要得益於先進技術的採用,包括即時資料監控、物聯網整合和遠端資訊處理。這些智慧增強功能可以實現更好的路線最佳化,減少非計劃停機時間,並支援預測性維護策略,從而提高車隊營運的成本效益和可靠性。此外,液壓部件和真空泵系統的創新使卡車具有更高的吸力和更低的噪音水平,從而提高了營運效率,同時符合更嚴格的環保法規。

就燃料類型而言,2024 年內燃機 (ICE) 真空吸污車佔據市場主導地位,佔 88%。儘管佔據主導地位,但隨著人們對清潔燃料替代品的興趣日益濃厚,人們正朝著永續發展的方向轉變。再生天然氣 (RNG)(通常從農業或垃圾掩埋場甲烷中獲取)和液化天然氣 (LNG) 正逐漸成為傳統柴油的熱門替代品,它們不僅碳排放更低,而且在監管方面也更具優勢。氫動力內燃機作為過渡解決方案,也越來越受到青睞,它填補了傳統柴油引擎與純電動或零排放車之間的空白。

2024年,歐洲真空吸污車市場佔據29%的市場佔有率,這得益於該地區嚴格的環境法規強制推行高效的廢棄物處理和污染控制技術,使得真空吸污車成為公共事業、建築和工業清潔領域的必備設備。這些車輛廣泛用於維護下水道系統、處理危險廢物以及管理基礎設施建設項目產生的垃圾。歐洲持續的城市化進程和對綠色基礎設施的投資進一步推動了對技術先進、低排放真空吸污車日益成長的需求。隨著對永續性和市政清潔的日益重視,預計該地區公共和私營部門的需求都將保持強勁。

為了維持並鞏固市場地位,主要公司正在投資創新和永續發展。 Amphitec BV、Federal Signal、GapVax、東正教專用車、DISAB Vacuum Technology、Alamo Group、福龍馬集團、Cappellotto、貝克休斯和Super Products等公司正在整合更清潔的燃油系統,推進真空技術,並擴大其地理覆蓋範圍。他們還專注於與市政當局和工業營運商建立戰略合作夥伴關係,以確保長期合約和可靠的服務管道。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- OEM製造商

- 零件供應商

- 底盤和引擎供應商

- 租賃和車隊服務提供者

- 系統整合商和客製化製造商

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 主要材料價格波動

- 供應鏈重組

- 價格傳導至終端市場

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 對貿易的影響

- 利潤率分析

- 技術與創新格局

- 重要新聞和舉措

- 成本細分分析

- 定價分析

- 產品

- 地區

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 都市化進程加快,城市垃圾管理需求增加

- 石油天然氣和採礦業務的擴張

- 更嚴格的環境和安全法規

- 技術進步和自動化

- 產業陷阱與挑戰

- 高昂的資本和維護成本

- 發展中地區基礎建設有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 吸液車

- 乾吸卡車

- 組合卡車

第6章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 冰

- 電的

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 工業清潔

- 挖掘

- 市政

- 常規清潔

- 其他

第8章:市場估計與預測:依產能,2021 - 2034 年

- 主要趨勢

- 容量小(最多 5 立方米)

- 中等容量(5-10 m³)

- 容量大(10m³以上)

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Alamo Group

- Amphitec BV

- Cappellotto

- DISAB Vacuum Technology

- Dongzheng Special Purpose Vehicle

- Federal Signal

- Fulongma Group

- GapVax

- Gradall Industries

- Guzzler Manufacturing

- Hi-Vac Corporation

- Kanematsu Engineering

- Keith Huber

- KOKS Group

- Ledwell & Son

- Rivard

- Sewer Equipment

- Super Products

- Vacall Industries

- Vac-Con

The Global Vacuum Truck Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 4 billion by 2034, driven by the rise in urbanization and rapid industrial development, especially across emerging economies. These vehicles are essential for handling solid and liquid waste, sewer maintenance, and cleaning operations across a wide range of industries. As cities grow and infrastructure expands, public and private entities are increasingly turning to vacuum trucks for efficient waste removal and sanitation. Industrial sectors such as mining, construction, and energy also rely on vacuum trucks to manage spills, sludge, and hazardous materials, reinforcing the vehicle's importance in modern waste management ecosystems.

Stricter environmental regulations introduced globally have prompted municipalities and industries to adopt vacuum trucks to meet pollution control requirements. These vehicles offer a secure method of transporting hazardous and non-hazardous materials without contaminating the environment. Their role in ensuring safety compliance across sectors like chemicals, utilities, and petroleum continues to gain prominence. As environmental standards evolve, there's growing interest in technologically advanced vacuum trucks that provide better performance, reduced emissions, and enhanced safety.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $4 Billion |

| CAGR | 6.5% |

The liquid suction truck segment held a 60% share in 2024 and is projected to reach USD 2 billion by 2034. This growth is largely fueled by the adoption of advanced technologies, including real-time data monitoring, IoT integration, and telematics. These smart enhancements enable better route optimization, reduce unplanned downtimes, and support predictive maintenance strategies, making fleet operations more cost-effective and reliable. Additionally, innovations in hydraulic components and vacuum pump systems have resulted in trucks that operate with higher suction power and reduced noise levels, which improves operational efficiency while aligning with stricter environmental mandates.

When it comes to fuel types, internal combustion engine (ICE) vacuum trucks dominated the market in 2024 with an 88% share. Despite this dominance, the shift toward sustainability is evident with increased interest in cleaner fuel alternatives. Renewable natural gas (RNG), often captured from agricultural or landfill methane, and liquefied natural gas (LNG) are emerging as popular substitutes to conventional diesel, offering lower carbon emissions and regulatory benefits. Hydrogen-powered ICEs are also gaining traction as an interim solution, bridging the gap between traditional diesel engines and fully electric or zero-emission vehicles.

Europe Vacuum Truck Market held 29% share in 2024, driven by the region's strict environmental regulations have made efficient waste handling and pollution control technologies mandatory, positioning vacuum trucks as essential for public utilities, construction, and industrial cleaning. These vehicles are widely utilized for maintaining sewer systems, handling hazardous waste, and managing debris from infrastructure development projects. Continued urbanization and investments in green infrastructure across Europe further support the rising need for technologically advanced, low-emission vacuum trucks. With a growing emphasis on sustainability and municipal cleanliness, demand is expected to stay strong across both public and private sectors in the region.

To maintain and strengthen market positioning, key companies are investing in innovation and sustainability. Players like Amphitec BV, Federal Signal, GapVax, Dongzheng Special Purpose Vehicle, DISAB Vacuum Technology, Alamo Group, Fulongma Group, Cappellotto, Baker Hughes, and Super Products are integrating cleaner fuel systems, advancing vacuum technologies, and expanding their geographic presence. They also focus on building strategic partnerships with municipalities and industrial operators to ensure long-term contracts and dependable service pipelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEM Manufacturers

- 3.2.2 Component Suppliers

- 3.2.3 Chassis & Engine Providers

- 3.2.4 Rental & Fleet Service Providers

- 3.2.5 System Integrators & Custom Fabricators

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the Industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.2 Supply chain restructuring

- 3.3.2.3 Price transmission to end markets

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Cost breakdown analysis

- 3.8 Pricing analysis

- 3.8.1 Product

- 3.8.2 Region

- 3.9 Patent analysis

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing Urbanization and Municipal Waste Management Needs

- 3.11.1.2 Expansion in Oil & Gas and Mining Operations

- 3.11.1.3 Stricter Environmental and Safety Regulations

- 3.11.1.4 Technological Advancements and Automation

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High Capital and Maintenance Costs

- 3.11.2.2 Limited Infrastructure in Developing Regions

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Liquid suction trucks

- 5.3 Dry suction trucks

- 5.4 Combination trucks

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Industrial cleaning

- 7.3 Excavation

- 7.4 Municipal

- 7.5 General cleaning

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Small capacity (Up to 5 m³)

- 8.3 Medium capacity (5–10 m³)

- 8.4 Large capacity (Above 10 m³)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alamo Group

- 10.2 Amphitec BV

- 10.3 Cappellotto

- 10.4 DISAB Vacuum Technology

- 10.5 Dongzheng Special Purpose Vehicle

- 10.6 Federal Signal

- 10.7 Fulongma Group

- 10.8 GapVax

- 10.9 Gradall Industries

- 10.10 Guzzler Manufacturing

- 10.11 Hi-Vac Corporation

- 10.12 Kanematsu Engineering

- 10.13 Keith Huber

- 10.14 KOKS Group

- 10.15 Ledwell & Son

- 10.16 Rivard

- 10.17 Sewer Equipment

- 10.18 Super Products

- 10.19 Vacall Industries

- 10.20 Vac-Con

真空吸污車市場:全球市場預測,2026-2032年

真空吸污車市場:全球市場預測,2026-2032年 真空吸污車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、最終用戶、功能、設備

真空吸污車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、最終用戶、功能、設備 真空抽吸車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

真空抽吸車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 真空吸污車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、燃料類型、應用類型、地區和競爭格局分類,2021-2031年

真空吸污車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、燃料類型、應用類型、地區和競爭格局分類,2021-2031年 2026-2030年全球真空吸污車市場

2026-2030年全球真空吸污車市場 真空吸污車市場規模、佔有率及成長分析(按產品類型、材質、應用和地區分類)-產業預測(2026-2033 年)

真空吸污車市場規模、佔有率及成長分析(按產品類型、材質、應用和地區分類)-產業預測(2026-2033 年) 真空卡車的世界市場

真空卡車的世界市場