|

市場調查報告書

商品編碼

1741037

碳酸氫鈉市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Sodium Bicarbonate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

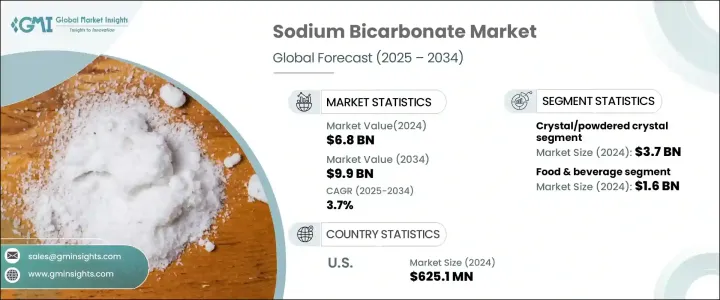

2024年,全球碳酸氫鈉市場規模達68億美元,預計到2034年將以3.7%的複合年成長率成長,達到99億美元,這得益於工業應用的不斷擴展以及各行業法規合規性不斷提高。從歷史上看,碳酸氫鈉一直是許多行業的主要產品,包括製藥、食品加工和環境解決方案。儘管全球供應鏈不穩定導致碳酸氫鈉供應中斷,但其需求仍表現出顯著的韌性,這主要得益於其在各種製造和加工業務中不可或缺的作用。

亞太、北美和歐洲等地區的需求成長主要源自於快速的工業化進程和日益增強的環保意識。這些地區正在積極採取措施,以符合不斷發展的環保標準,從而對碳酸氫鈉的需求持續成長。此外,碳酸氫鈉在醫療保健配方中的應用以及作為藥物pH值控制劑的應用也持續提升了其重要性。在農業和動物飼料領域,碳酸氫鈉也顯著成長,在這些領域中,碳酸氫鈉既可用作殺菌劑,也可用作營養添加劑。這些因素共同確保了該產品在全球供應鏈和消費週期中佔據重要地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 68億美元 |

| 預測值 | 99億美元 |

| 複合年成長率 | 3.7% |

晶體和粉狀碳酸氫鈉繼續佔據市場主導地位。預計2024年該細分市場的市值將達到37億美元,2025年至2034年間的複合年成長率將達到4.2%。粉狀碳酸氫鈉因其化學穩定性、易儲存性和更長的保存期限而脫穎而出。這種形態在食品生產、製藥和個人護理等注重穩定品質和可靠配方的行業中尤為有利。粉末狀碳酸氫鈉因其細膩、流動性好的質地而備受青睞,這使其適合直接混合、高效包裝和精確配製。此外,它還具有優異的溶解性和一致的粒徑,從而簡化了嚴格監管行業中的計量操作。其在煙氣脫硫的應用也增強了其在工業應用領域的需求。

在食品和飲料領域,碳酸氫鈉在2024年的估值為16億美元,預計2025年至2034年的複合年成長率為4.1%。該領域約佔總市場佔有率的22.9%。碳酸氫鈉在烘焙、加工食品和飲料中的應用日益廣泛,凸顯了其作為重要膨鬆劑和pH調節劑的作用。消費者越來越傾向於選擇方便、即食和健康的食品,這促使製造商使用既能提升產品品質又不損害健康的配料。碳酸氫鈉憑藉其清潔標籤的吸引力和多功能性,完美契合了這些偏好。

在美國,2024年碳酸氫鈉市值為6.251億美元,預計到2034年將以3.5%的複合年成長率成長。美國市場的成長主要受工業活動、不斷變化的法規和持續的經濟發展的影響。政府的支持性政策、完善的工業基礎設施以及嚴格的環境和食品安全法規促進了穩定的需求。疫情後消費者行為的轉變,以及新的工業投資,進一步推動了成長。醫療保健和便利消費品領域的需求均顯著上升,鞏固了美國在全球市場中的優勢地位。

競爭格局由主要參與者主導,他們旨在透過創新和策略擴張來獲取更大的市場佔有率。企業正在實現產品線多元化,投資永續解決方案,並加強全球影響力以滿足不斷成長的需求。持續的研發投入,尤其是在增強產品功能性和永續性方面的投入,正在重塑這些企業的定位。尤其值得一提的是,它們更重視產品創新、注重環保的生產實踐,並透過生產最佳化和併購進軍高需求地區。隨著市場動態日益受到消費趨勢和監管變化的影響,企業正在調整策略,以保持競爭力並回應全球需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 供給側影響(原料)

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 2021-2024年主要出口國

- 2021-2024年主要進口國

- 製造流程和供應鏈分析

- 原料分析

- 關鍵原料

- 原物料採購

- 原物料價格趨勢

- 原物料供應商

- 製造流程分析

- 索爾維法

- 天然鹼法

- 碳酸鈉法

- 氫氧化鈉法

- 蘇打石提取

- 新興生產技術

- 成本結構分析

- 供應鏈分析

- 供應鏈結構和映射

- 分銷通路分析

- 主要物流供應商

- 供應鏈挑戰

- 供應鏈最佳化策略

- 生產能力分析

- 全球生產能力

- 產能利用率

- 計畫中的產能擴張

- 庫存管理和倉儲

- 品質控制和認證標準

- 原料分析

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 全球監管格局

- 食品級法規

- 藥品級法規

- 工業級法規

- 區域監管分析

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

- 進出口法規

- 產品標籤和包裝法規

- 安全和處理指南

- 環境法規

- 排放控制法規

- 廢棄物管理法規

- 監理影響評估

- 對生產成本的影響

- 對市場進入障礙的影響

- 對產品開發的影響

- 全球監管格局

- 衝擊力

- 成長動力

- 製藥業的需求不斷增加。

- 擴大在食品和飲料領域的應用。

- 人們對環境議題的關注度不斷提高,對環保產品的需求也不斷增加。

- 個人護理和化妝品行業的成長。

- 產業陷阱與挑戰

- 原物料價格波動。

- 對生產過程有嚴格的環境法規。

- 成長動力

- 未來市場展望與策略機遇

- 2025-2034年市場預測

- 短期預測(1-3年)

- 中期預測(4-7年)

- 長期預測(8-10年)

- 新興市場機遇

- 高成長應用領域

- 尚未開發的區域市場

- 利基市場機會

- 策略成長機會

- 產品開發機會

- 市場拓展機會

- 加值服務機會

- 技術採用與創新路線圖

- 永續發展驅動的機遇

- 策略建議

- 對於製造商

- 對於分銷商和供應商

- 最終用途

- 對於投資者

- 未來情境規劃

- 樂觀情境

- 現實場景

- 悲觀情景

- 2025-2034年市場預測

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

- 風險分析和緩解策略

- 市場風險評估

- 需求波動風險

- 價格波動風險

- 競爭風險

- 替代風險

- 營運風險

- 供應鏈中斷

- 生產風險

- 品質控制風險

- 監理與合規風險

- 環境和永續性風險

- 地緣政治風險

- 風險緩解策略

- 多元化策略

- 對沖策略

- 保險和風險轉移機制

- 應急計劃

- 產業利害關係人的風險管理框架

- 市場風險評估

第5章:市場估計與預測:依形式,2021-2034

- 主要趨勢

- 水晶/粉晶

- 液體

- 泥

第6章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 食品和飲料

- 工業的

- 製藥

- 個人護理

- 農業化學品

- 動物飼料

- 其他

第7章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Akshar Chemical India Private Limited

- Ciner Group

- Church & Dwight

- Crystal Mark

- FMC

- GHCL

- Haohua Honghe Chemical

- Natural Soda

- Opta Minerals

- Sisecam

- Solvay

- Tata Chemicals

- Tosoh

The Global Sodium Bicarbonate Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 3.7% to reach USD 9.9 billion by 2034, driven by a combination of expanding industrial applications and rising regulatory compliance across various sectors. Historically, sodium bicarbonate has remained a staple across numerous industries, including pharmaceuticals, food processing, and environmental solutions. Despite facing disruptions due to global supply chain instability, the demand for sodium bicarbonate displayed significant resilience, largely due to its indispensable role in diverse manufacturing and processing operations.

The increasing demand in regions such as Asia Pacific, North America, and Europe has primarily been driven by rapid industrialization and growing environmental awareness. These regions are taking proactive steps to align with evolving environmental standards, resulting in sustained demand for sodium bicarbonate. Additionally, the compound's use in healthcare formulations and as a pH control agent in medications continues to fuel its relevance. There has also been notable growth in the agriculture and animal feed sectors, where sodium bicarbonate is used both as a fungicide and nutritional additive. These dynamics collectively ensure that the product retains a strong foothold in global supply chains and consumption cycles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 3.7% |

The crystal and powdered crystal forms of sodium bicarbonate continue to dominate the market landscape. Valued at USD 3.7 billion in 2024, this segment is projected to grow at a CAGR of 4.2% between 2025 and 2034. The powdered crystal form stands out for its chemical stability, ease of storage, and longer shelf life. This format is particularly advantageous in sectors like food production, pharmaceuticals, and personal care, where consistent quality and reliable formulation are key. Powdered sodium bicarbonate is preferred for its fine, free-flowing texture, which makes it suitable for direct blending, efficient packaging, and precise formulation. Furthermore, it offers excellent solubility and consistent particle size, which simplifies dosing in tightly regulated industries. Its utility in flue gas desulfurization also strengthens its demand across industrial applications.

Within the food and beverage sector, sodium bicarbonate held a valuation of USD 1.6 billion in 2024, with expectations to grow at a 4.1% CAGR from 2025 to 2034. This segment accounts for approximately 22.9% of the total market share. The increasing incorporation of sodium bicarbonate in baking, processed foods, and beverages underscores its role as a vital leavening and pH-regulating agent. Rising consumer inclination toward convenient, ready-to-eat, and health-oriented food options is pushing manufacturers to use ingredients that enhance product quality without compromising health. Sodium bicarbonate aligns well with these preferences due to its clean-label appeal and functional versatility.

In the United States, the sodium bicarbonate market was valued at USD 625.1 million in 2024 and is projected to expand at a CAGR of 3.5% through 2034. Growth in the U.S. market is largely shaped by industrial activity, evolving regulations, and ongoing economic developments. Supportive government policies, an established industrial infrastructure, and stringent environmental and food safety regulations are contributing to steady demand. Post-pandemic shifts in consumer behavior, alongside new industrial investments, have further bolstered growth. There is an observable uptick in demand across both healthcare and convenience-focused consumer goods sectors, reinforcing the country's stronghold in the global landscape.

The competitive landscape is dominated by key players aiming to secure larger market shares through innovation and strategic expansion. Companies are diversifying product lines, investing in sustainable solutions, and strengthening their global presence to meet rising demand. Continuous efforts in research and development, particularly toward enhancing product functionality and sustainability, are reshaping how these companies position themselves. In particular, there is a noticeable emphasis on product innovation, eco-conscious manufacturing practices, and tapping into high-demand regions through production optimization and mergers. With market dynamics increasingly shaped by consumer trends and regulatory shifts, businesses are adjusting strategies to stay competitive and responsive to global needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Manufacturing process and supply chain analysis

- 3.4.1 Raw materials analysis

- 3.4.1.1 Key raw materials

- 3.4.1.2 Raw material sourcing

- 3.4.1.3 Raw material price trends

- 3.4.1.4 Raw material suppliers

- 3.4.2 Manufacturing process analysis

- 3.4.2.1 Solvay process

- 3.4.2.2 Trona process

- 3.4.2.3 Sodium carbonate method

- 3.4.2.4 Sodium hydroxide method

- 3.4.2.5 Nahcolite extraction

- 3.4.2.6 Emerging production technologies

- 3.4.2.7 Cost structure analysis

- 3.4.3 Supply chain analysis

- 3.4.3.1 Supply chain structure and mapping

- 3.4.3.2 Distribution channels analysis

- 3.4.3.3 Key logistics providers

- 3.4.3.4 Supply chain challenges

- 3.4.3.5 Supply chain optimization strategies

- 3.4.4 Production capacity analysis

- 3.4.4.1 Global production capacity

- 3.4.4.2 Capacity utilization rates

- 3.4.4.3 Planned capacity expansions

- 3.4.5 Inventory management and warehousing

- 3.4.6 Quality control and certification standards

- 3.4.1 Raw materials analysis

- 3.5 Supplier landscape

- 3.6 Profit margin analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.8.1 Global regulatory landscape

- 3.8.1.1 Food grade regulations

- 3.8.1.2 Pharmaceutical grade regulations

- 3.8.1.3 Industrial grade regulations

- 3.8.2 Regional regulatory analysis

- 3.8.2.1 North America

- 3.8.2.2 Europe

- 3.8.2.3 Asia pacific

- 3.8.2.4 Rest of the world

- 3.8.3 Import-export regulations

- 3.8.4 Product labeling and packaging regulations

- 3.8.5 Safety and handling guidelines

- 3.8.6 Environmental regulations

- 3.8.6.1 Emission control regulations

- 3.8.6.2 Waste management regulations

- 3.8.7 Regulatory impact assessment

- 3.8.7.1 Impact on production costs

- 3.8.7.2 Impact on market entry barriers

- 3.8.7.3 Impact on product development

- 3.8.1 Global regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand in the pharmaceutical industry.

- 3.9.1.2 Expanding applications in food and beverage sectors.

- 3.9.1.3 Rising environmental concerns and demand for eco-friendly products.

- 3.9.1.4 Growth in the personal care and cosmetics industry.

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Price volatility of raw materials.

- 3.9.2.2 Stringent environmental regulations on production processes.

- 3.9.1 Growth drivers

- 3.10 Future market outlook and strategic opportunities

- 3.10.1 Market forecast 2025–2034

- 3.10.1.1 Short-term forecast (1–3 years)

- 3.10.1.2 Medium-term forecast (4–7 years)

- 3.10.1.3 Long-term forecast (8–10 years)

- 3.10.2 Emerging market opportunities

- 3.10.2.1 High-growth application areas

- 3.10.2.2 Untapped regional markets

- 3.10.2.3 Niche segment opportunities

- 3.10.3 Strategic growth opportunities

- 3.10.3.1 Product development opportunities

- 3.10.3.2 Market expansion opportunities

- 3.10.3.3 Value-added services opportunities

- 3.10.4 Technology adoption and innovation roadmap

- 3.10.5 Sustainability-driven opportunities

- 3.10.6 Strategic recommendations

- 3.10.7 For manufacturers

- 3.10.8 For distributors and suppliers

- 3.10.9 For end use

- 3.10.10 For investors

- 3.10.11 Future scenario planning

- 3.10.11.1 Optimistic scenario

- 3.10.11.2 Realistic scenario

- 3.10.11.3 Pessimistic scenario

- 3.10.1 Market forecast 2025–2034

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Risk analysis and mitigation strategies

- 4.5.1 Market risks assessment

- 4.5.1.1 Demand fluctuation risks

- 4.5.1.2 Price volatility risks

- 4.5.1.3 Competitive risks

- 4.5.1.4 Substitution risks

- 4.5.2 Operational risks

- 4.5.2.1 Supply chain disruptions

- 4.5.2.2 Production risks

- 4.5.2.3 Quality control risks

- 4.5.3 Regulatory and compliance risks

- 4.5.4 Environmental and sustainability risks

- 4.5.5 Geopolitical risks

- 4.5.6 Risk mitigation strategies

- 4.5.6.1 Diversification strategies

- 4.5.6.2 Hedging strategies

- 4.5.6.3 Insurance and risk transfer mechanisms

- 4.5.6.4 Contingency planning

- 4.5.7 Risk management framework for industry stakeholders

- 4.5.1 Market risks assessment

Chapter 5 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Crystal/powdered crystal

- 5.3 Liquid

- 5.4 Slurry

Chapter 6 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Industrial

- 6.4 Pharmaceutical

- 6.5 Personal care

- 6.6 Agrochemical

- 6.7 Animal feed

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Akshar Chemical India Private Limited

- 8.2 Ciner Group

- 8.3 Church & Dwight

- 8.4 Crystal Mark

- 8.5 FMC

- 8.6 GHCL

- 8.7 Haohua Honghe Chemical

- 8.8 Natural Soda

- 8.9 Opta Minerals

- 8.10 Sisecam

- 8.11 Solvay

- 8.12 Tata Chemicals

- 8.13 Tosoh