|

市場調查報告書

商品編碼

1741034

醫療電子市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Medical Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

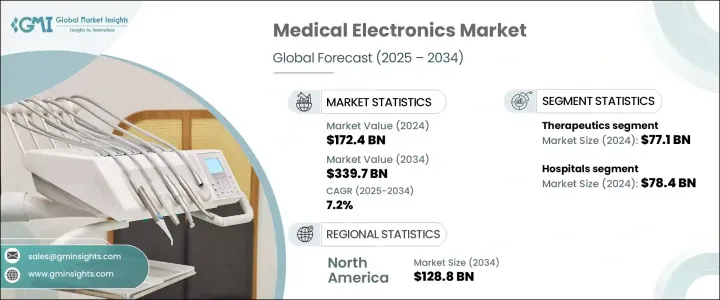

2024年,全球醫療電子市場規模達1,724億美元,預計到2034年將以7.2%的複合年成長率成長,達到3,397億美元。這一成長主要源於醫療保健領域電子系統和設備的廣泛應用,這些系統和設備用於支援診斷、治療、預防和病患監護。隨著醫療保健領域日益數位化,醫療電子技術正在改變臨床醫生的診療方式。從診斷影像工具和穿戴式監視器到機器人手術系統和互聯治療系統,這些設備正在重塑患者體驗和臨床療效。人工智慧、物聯網和雲端運算等智慧技術的整合正在重新定義營運效率,加快診斷速度,提高資料準確性,並減少人為錯誤。醫院、診所,甚至家庭護理環境如今都依賴互聯的醫療電子設備來簡化工作流程、管理慢性疾病並增強病患參與度。隨著全球人口老化和非傳染性疾病發病率的上升,人們明顯轉向技術驅動的醫療保健解決方案。消費者要求個人化、便利和即時的醫療保健服務,推動公司加速創新並推出更直覺、更可靠的醫療電子設備。

慢性病和傳染病(包括心血管疾病、癌症和呼吸系統疾病)的發生率持續上升,這在很大程度上推動了對先進醫療電子產品的需求激增。大眾對早期疾病檢測和預防保健的認知日益增強,促進了診斷技術的廣泛應用。同時,微創手術技術的進步也加速了對高精準度電子工具的需求。這些創新正在幫助提高即時手術的準確性,縮短復健時間,並改善全球患者的臨床療效。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1724億美元 |

| 預測值 | 3397億美元 |

| 複合年成長率 | 7.2% |

醫療機器人、遠端監控和穿戴式診斷等領域的持續技術創新也為市場帶來了強勁發展勢頭。隨著消費者越來越傾向於更智慧、更互聯的醫療工具,電子產品在醫療應用中的整合也日益受到青睞。全球醫療保健支出的不斷成長進一步推動了先進電子設備的普及,尤其是那些用於管理複雜手術和長期照護的設備。這一趨勢在專業醫療領域尤其明顯,因為這些領域對即時資料、增強成像和精準控制的需求仍然至關重要。

2024年,治療領域收入達771億美元,這得益於植入式和體外設備在慢性病管理的應用日益增加。這些治療技術融合了先進的電子功能,以提高安全性、精準度和個人化護理,尤其是在心血管、神經系統和呼吸系統治療領域。心律調節器、神經刺激器和輸液幫浦等設備正被廣泛應用,以提高生活品質並減少就診次數。

2024年,醫院引領了終端用戶的採用,創造了784億美元的市場規模,佔據了45.5%的市場。這些機構高度依賴診斷和治療電子設備來有效管理門診和住院護理。醫院致力於最佳化臨床工作流程,盡量減少治療延誤,持續投資於下一代監測設備、手術技術和影像系統,以期獲得更佳的治療效果。

2023年,美國醫療電子市場規模達574億美元,這得益於心血管疾病、糖尿病、癌症和神經系統疾病等慢性疾病日益加重的負擔。隨著越來越多的患者需要持續監測和治療,對先進電子醫療設備的需求持續高漲。美國也受益於強大的研發基礎設施和早期的技術應用,這有助於其在醫療創新領域中保持領先地位。

全球醫療電子市場的領導者——包括奧林巴斯、深圳邁瑞生物醫療電子、西門子醫療、樂普醫療、波士頓科學、東芝醫療系統、富士膠片控股、通用電氣醫療、雅培實驗室、微創醫療科學、三星電子、美敦力、銳珂醫療、荷蘭皇家飛利浦和百勝——正在實施關鍵戰略以增強其市場影響力。這些策略包括增加研發投入以加速創新、與醫療服務供應商合作獲取即時回饋、拓展新興市場以及利用人工智慧和物聯網推出智慧診斷和遠端護理平台。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病和傳染病負擔加重

- 技術先進的醫療電子產品日益普及

- 越來越傾向微創手術

- 資本密集型機器租賃的興起和外國直接投資(FDI)重大政策的發展

- 產業陷阱與挑戰

- 嚴格的監管情景

- 缺乏熟練的醫療保健專業人員

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 各國應對措施

- 對產業的影響

- 供應方影響(製造成本)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(消費者成本)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(製造成本)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 療法

- 心律調節器

- 植入式心臟復律去顫器

- 神經刺激裝置

- 手術機器人

- 呼吸照護設備

- 診斷

- 病人監護設備

- PET-CT設備

- MRI掃描儀

- 超音波設備

- X光設備

- CT掃描儀

- 其他產品類型

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 診所

- 其他最終用途

第7章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第8章:公司簡介

- Abbott Laboratories

- Boston Scientific

- Carestream Health

- Esaote

- FUJIFILM Holdings

- GE HealthCare

- Koninklijke Philips

- Lepu Medical Technology

- Medtronic

- MicroPort Scientific

- Olympus

- Samsung Electronics

- Shenzhen Mindray Bio-Medical Electronics

- Siemens Healthineers

- Toshiba Medical Systems

The Global Medical Electronics Market was valued at USD 172.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 339.7 billion through 2034. This growth is driven by the expanding use of electronic systems and devices across healthcare sectors to support diagnosis, treatment, prevention, and patient monitoring. As the healthcare landscape becomes increasingly digitized, medical electronics are transforming how clinicians deliver care. From diagnostic imaging tools and wearable monitors to robotic surgery systems and connected therapeutics, these devices are reshaping patient experiences and clinical outcomes. The integration of smart technologies like AI, IoT, and cloud computing is redefining operational efficiency, enabling faster diagnostics, improving data accuracy, and reducing human error. Hospitals, clinics, and even home care environments now rely on interconnected medical electronics to streamline workflows, manage chronic diseases, and enhance patient engagement. With an aging global population and the rising incidence of non-communicable diseases, there's a clear shift toward tech-driven healthcare solutions. Consumers are demanding personalized, accessible, and real-time healthcare services, pushing companies to innovate faster and introduce more intuitive, reliable medical electronic devices.

The continuous rise in chronic and infectious diseases-including cardiovascular conditions, cancer, and respiratory disorders-is contributing heavily to the surging demand for advanced medical electronics. There's growing public awareness around early disease detection and preventive care, which is encouraging the widespread use of diagnostic technologies. At the same time, advancements in minimally invasive surgical techniques are accelerating the need for high-precision electronic tools. These innovations are helping improve real-time procedural accuracy, reduce recovery times, and enhance clinical outcomes for patients globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $172.4 Billion |

| Forecast Value | $339.7 Billion |

| CAGR | 7.2% |

The market is also seeing robust momentum from ongoing technological innovation in areas like medical robotics, remote monitoring, and wearable diagnostics. As consumers lean toward smarter, more connected healthcare tools, the integration of electronics in medical applications continues to gain traction. Rising global healthcare expenditures further support the adoption of sophisticated electronic devices, especially those designed to manage complex procedures and long-term care. This trend is particularly evident in specialized medical fields where demand for real-time data, enhanced imaging, and precision control remains critical.

In 2024, the therapeutics segment generated USD 77.1 billion, driven by the increasing use of implantable and external devices to manage chronic conditions. These therapeutic technologies combine advanced electronic features to improve safety, delivery accuracy, and personalized care-especially in cardiovascular, neurological, and respiratory treatment. Devices such as pacemakers, neurostimulators, and infusion pumps are being widely adopted to boost quality of life and reduce hospital visits.

Hospitals led end-user adoption in 2024, generating USD 78.4 billion and accounting for 45.5% of the market share. These institutions depend heavily on both diagnostic and therapeutic electronics to manage outpatient and inpatient care efficiently. With a focus on optimizing clinical workflows and minimizing treatment delays, hospitals continue to invest in next-generation monitoring equipment, surgical technologies, and imaging systems to drive better outcomes.

The U.S. Medical Electronics Market generated USD 57.4 billion in 2023, fueled by the growing burden of chronic diseases such as cardiovascular disorders, diabetes, cancer, and neurological conditions. With more patients requiring continuous monitoring and treatment, the demand for advanced electronic medical devices remains high. The U.S. also benefits from strong R&D infrastructure and early tech adoption, helping sustain its leadership in medical innovation.

Leading players in the Global Medical Electronics Market-including Olympus, Shenzhen Mindray Bio-Medical Electronics, Siemens Healthineers, Lepu Medical Technology, Boston Scientific, Toshiba Medical Systems, FUJIFILM Holdings, GE HealthCare, Abbott Laboratories, MicroPort Scientific, Samsung Electronics, Medtronic, Carestream Health, Koninklijke Philips, and Esaote-are implementing key strategies to strengthen their market presence. These include boosting R&D investments to fast-track innovation, collaborating with healthcare providers for real-time feedback, expanding into emerging markets, and leveraging AI and IoT to launch intelligent diagnostic and remote care platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of chronic and infectious diseases

- 3.2.1.2 Growing adoption of technologically advanced medical electronics

- 3.2.1.3 Increasing preference towards minimally invasive surgeries

- 3.2.1.4 Upsurge in leasing of capital-intensive machines and development of significant policies for foreign direct investment (FDI)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Pacemakers

- 5.2.2 Implantable cardioverter-defibrillators

- 5.2.3 Neurostimulation devices

- 5.2.4 Surgical robots

- 5.2.5 Respiratory care devices

- 5.3 Diagnostics

- 5.3.1 Patient monitoring devices

- 5.3.2 PET-CT devices

- 5.3.3 MRI scanners

- 5.3.4 Ultrasound devices

- 5.3.5 X-rays devices

- 5.3.6 CT scanners

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Clinics

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Boston Scientific

- 8.3 Carestream Health

- 8.4 Esaote

- 8.5 FUJIFILM Holdings

- 8.6 GE HealthCare

- 8.7 Koninklijke Philips

- 8.8 Lepu Medical Technology

- 8.9 Medtronic

- 8.10 MicroPort Scientific

- 8.11 Olympus

- 8.12 Samsung Electronics

- 8.13 Shenzhen Mindray Bio-Medical Electronics

- 8.14 Siemens Healthineers

- 8.15 Toshiba Medical Systems

醫療用電子設備市場:按設備類型、技術和應用分類-2026-2032年全球市場預測

醫療用電子設備市場:按設備類型、技術和應用分類-2026-2032年全球市場預測 醫療和保健電子市場預測至2034年—按設備類型、產品類型、技術、應用、最終用戶和地區分類的全球分析

醫療和保健電子市場預測至2034年—按設備類型、產品類型、技術、應用、最終用戶和地區分類的全球分析 仿生半導體架構市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶分類生物晶片半導體平台市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型及最終用戶分類醫療用電子設備市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能

仿生半導體架構市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶分類生物晶片半導體平台市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型及最終用戶分類醫療用電子設備市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能 2026年全球醫療用電子設備市場報告醫用壓電陶瓷元件市場按產品類型、材料類型、應用和最終用戶分類-2026-2032年全球預測電子測角儀市場按產品類型、感測器技術、技術、精度、分銷管道、應用和最終用戶分類,全球預測,2026-2032年

2026年全球醫療用電子設備市場報告醫用壓電陶瓷元件市場按產品類型、材料類型、應用和最終用戶分類-2026-2032年全球預測電子測角儀市場按產品類型、感測器技術、技術、精度、分銷管道、應用和最終用戶分類,全球預測,2026-2032年 醫療用電子設備市場規模、佔有率和成長分析(按組件、醫療器材/設備類型、醫療程序、醫療設備分類、醫療機構和地區分類)—產業預測(2026-2033 年)

醫療用電子設備市場規模、佔有率和成長分析(按組件、醫療器材/設備類型、醫療程序、醫療設備分類、醫療機構和地區分類)—產業預測(2026-2033 年) 醫療電子市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、最終用戶、地區和競爭格局分類,2020-2030年預測

醫療電子市場-全球產業規模、佔有率、趨勢、機會和預測,依產品類型、最終用戶、地區和競爭格局分類,2020-2030年預測