|

市場調查報告書

商品編碼

1741012

液化氫儲存市場機會、成長動力、產業趨勢分析及2025-2034年預測Liquefied Hydrogen Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

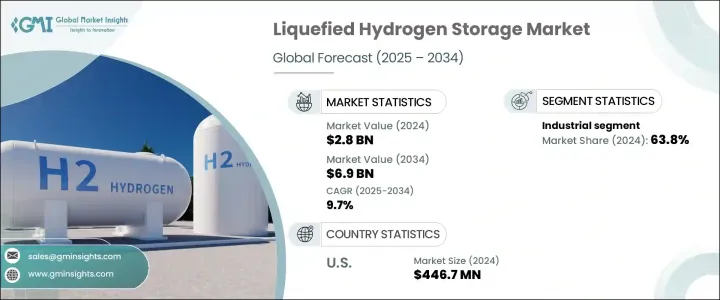

2024年,全球液化氫儲存市場規模達28億美元,預計到2034年將以9.7%的複合年成長率成長,達到69億美元,這得益於全球日益轉向清潔能源的趨勢。隨著脫碳努力的加強,液化氫正成為重塑未來能源格局的關鍵因素。各國政府、企業和消費者正齊心協力,尋求更乾淨、更有效率的解決方案,這為氫能技術的發展創造了肥沃的土壤。液化氫儲存是這項轉變的核心,它為再生能源整合提供了可擴展、高效且經濟的解決方案。低溫技術、更智慧的監控系統和緊湊型設計的突破,正在推動該行業朝著更高的可靠性和可承受性邁進。將過剩的再生能源以氫氣形式儲存並在需求高峰時利用的能力,正在解決與間歇性和電網穩定性相關的關鍵挑戰。隨著各國大力投資基礎建設升級和能源韌性,液化氫儲存將成為各行各業不可或缺的一部分。私部門的創新、公共資金和有利的監管框架正在融合,釋放前所未有的成長機會,標誌著全球能源經濟的重大轉變。

向液化氫的轉型已超越工業營運,並在交通運輸、儲能和分散式發電領域取得了強勁進展。全球各國政府正在加速這項進程,提供補貼和政策誘因,鼓勵採用更環保的技術。日益嚴格的排放法規使氫能解決方案在運輸、發電和重工業領域越來越有吸引力。液化氫儲存在這些快速發展的應用中正獲得強勁發展,為符合全球氣候目標的長期永續能源解決方案奠定了基礎。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 28億美元 |

| 預測值 | 69億美元 |

| 複合年成長率 | 9.7% |

隨著化學、煉油和高熱製造等行業整合氫能以逐步淘汰化石燃料,工業領域在2024年將佔據63.8%的主導佔有率。液氫因其更高的能量密度仍然是首選,使其成為大規模儲存和高效運作的理想選擇。對大容量、遠端儲能日益成長的需求,也使液態氫成為專注於零排放性能的運輸系統的顛覆性技術。在工業領域應對空間和效率限制方面,液氫在緊湊的儲存框架內提供更大能量輸出的能力至關重要。隨著間歇性再生能源的加速擴張,氫在平衡供需方面的作用對於確保電網穩定正變得越來越重要。

2024年,美國液化氫儲存市場規模達到4.467億美元,這得益於氫能基礎設施(尤其是加氫站和大型儲存項目)的強勁投資。先進的製造能力以及日益壯大的電動車和氫能汽車產業正在推動需求成長。包括能源部主導的聯邦措施正在積極支持研發工作,以增強未來儲存的可擴展性和可靠性。

為了保持競爭力,FuelCell Energy、Cockerill Jingli、ITM Power、SSE、Air Products and Chemicals、ENGIE、Linde、McPhy Energy、Air Liquide、Gravitricity、GKN 和 Nel 等公司正在加倍投入創新和策略合作。關鍵策略包括擴大產能、推動低溫絕緣技術、投資長期研究以及成立合作企業以加速部署和實現產品多樣化。積極參與政府支持的計畫也有助於這些企業獲得資金,並在新興市場建立先發優勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 貿易管理關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 工業的

- 運輸

- 固定式

- 其他

第6章:市場規模及預測:依地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

第7章:公司簡介

- Air Liquide

- Air Products and Chemicals

- Cockerill Jingli

- ENGIE

- FuelCell Energy

- GKN

- Gravitricity

- ITM Power

- Linde

- McPhy Energy

- Nel

- SSE

The Global Liquefied Hydrogen Storage Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 6.9 billion by 2034, driven by the growing worldwide shift toward cleaner energy alternatives. As decarbonization efforts intensify, liquefied hydrogen is becoming a key player in reshaping the future energy landscape. Governments, corporations, and consumers are aligning to demand cleaner, more efficient solutions, creating fertile ground for hydrogen technologies. Liquefied hydrogen storage is at the heart of this transformation, providing a scalable, efficient, and cost-effective solution for renewable energy integration. Breakthroughs in cryogenic technologies, smarter monitoring systems, and compact designs are pushing the industry toward higher reliability and affordability. The ability to store excess renewable energy as hydrogen and utilize it when demand peaks is solving critical challenges related to intermittency and grid stability. As nations invest heavily in infrastructure upgrades and energy resilience, liquefied hydrogen storage is poised to become indispensable across industries. Private-sector innovation, public funding, and favorable regulatory frameworks are converging to unlock unprecedented growth opportunities, signaling a pivotal shift in the global energy economy.

The transition to liquefied hydrogen is extending beyond industrial operations and making strong inroads into mobility, energy storage, and distributed power generation. Worldwide government initiatives are accelerating the momentum, offering subsidies and policy incentives to adopt greener technologies. Tightening emission regulations are making hydrogen solutions increasingly attractive across transportation, power generation, and heavy industry. Liquefied hydrogen storage is gaining strong traction in these fast-evolving applications, setting the stage for long-term, sustainable energy solutions that align with global climate targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 9.7% |

The industrial sector accounted for a dominant 63.8% share in 2024 as sectors like chemicals, refineries, and high-heat manufacturing integrate hydrogen to phase out fossil-based fuels. Liquefied hydrogen remains the preferred choice due to its higher energy density, making it ideal for large-scale storage and high-efficiency operations. The growing need for high-capacity, long-range energy storage is also making liquefied hydrogen a game-changer for transportation systems focused on zero-emission performance. Its ability to deliver extended energy outputs within compact storage frameworks is critical as industries tackle space and efficiency constraints. As the expansion of intermittent renewable energy sources accelerates, hydrogen's role in balancing supply and demand is becoming even more vital to ensuring grid stability.

The United States Liquefied Hydrogen Storage Market reached USD 446.7 million in 2024, fueled by robust investment in hydrogen infrastructure, especially in fueling stations and large storage projects. Advanced manufacturing capabilities and the growing electric and hydrogen vehicle industries are propelling demand. Federal initiatives, including those led by the Department of Energy, are aggressively supporting R&D efforts to enhance storage scalability and reliability for the future.

To stay competitive, companies like FuelCell Energy, Cockerill Jingli, ITM Power, SSE, Air Products and Chemicals, ENGIE, Linde, McPhy Energy, Air Liquide, Gravitricity, GKN, and Nel are doubling down on innovation and strategic partnerships. Key strategies include expanding production capacities, advancing cryogenic insulation technologies, investing in long-term research, and forming collaborative ventures to fast-track deployment and product diversification. Active participation in government-backed programs is also helping these players secure funding and build early-mover advantages across emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trade administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034, (USD Million)

- 5.1 Key trends

- 5.2 Industrial

- 5.3 Transportation

- 5.4 Stationary

- 5.5 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034, (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products and Chemicals

- 7.3 Cockerill Jingli

- 7.4 ENGIE

- 7.5 FuelCell Energy

- 7.6 GKN

- 7.7 Gravitricity

- 7.8 ITM Power

- 7.9 Linde

- 7.10 McPhy Energy

- 7.11 Nel

- 7.12 SSE

全球小型空氣壓縮系統市場:按產品類型、壓力、最終用戶和地區分類-預測(至2030年)

全球小型空氣壓縮系統市場:按產品類型、壓力、最終用戶和地區分類-預測(至2030年) 氫氣儲存腔市場預測至2034年—按儲存類型、儲存容量、功能、應用、最終用戶和地區分類的全球分析

氫氣儲存腔市場預測至2034年—按儲存類型、儲存容量、功能、應用、最終用戶和地區分類的全球分析 2026年全球固體儲氫材料市場報告

2026年全球固體儲氫材料市場報告 固體氫儲存槽市場:依儲槽等級、安裝類型、儲存壓力、儲槽尺寸及應用分類-2026-2032年全球預測固體氫儲存系統市場:依儲存材料、系統、動作溫度和最終用戶分類,全球預測,2026-2032年全球固體儲氫解決方案市場(按材料類型、容量範圍、外形尺寸、應用和最終用戶分類)預測(2026-2032年)

固體氫儲存槽市場:依儲槽等級、安裝類型、儲存壓力、儲槽尺寸及應用分類-2026-2032年全球預測固體氫儲存系統市場:依儲存材料、系統、動作溫度和最終用戶分類,全球預測,2026-2032年全球固體儲氫解決方案市場(按材料類型、容量範圍、外形尺寸、應用和最終用戶分類)預測(2026-2032年) 全球地下儲氫市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球氫氣儲存市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球氫氣壓縮和儲存系統市場:預測(至2034年)-按儲存類型、技術、應用、最終用戶和地區分類的分析按容量、純度、類型、吸附劑類型、應用和最終用戶產業變壓式吸附氫氣純化系統市場—2026-2032年全球預測

全球地下儲氫市場規模、佔有率、趨勢及成長分析報告(2026-2034年)全球氫氣儲存市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球氫氣壓縮和儲存系統市場:預測(至2034年)-按儲存類型、技術、應用、最終用戶和地區分類的分析按容量、純度、類型、吸附劑類型、應用和最終用戶產業變壓式吸附氫氣純化系統市場—2026-2032年全球預測