|

市場調查報告書

商品編碼

1740988

能源和公用事業碳管理系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Energy and Utility Carbon Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

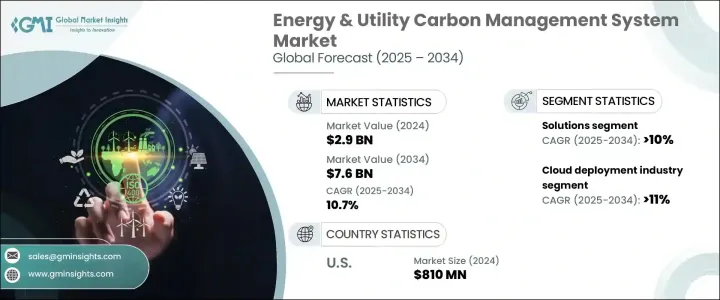

2024年,全球能源和公用事業碳管理系統市場規模達到29億美元,預計到2034年將以10.7%的複合年成長率成長,達到76億美元,這得益於能源行業排放法規的收緊和碳合規要求的不斷提高。隨著全球各行各業積極推進淨零排放目標,能源和公用事業公司面臨越來越大的壓力,需要採用數位碳管理平台來確保準確、即時地追蹤排放。市場正在經歷一場重大轉型,永續性正成為一項核心業務要務,而非一項可有可無的舉措。

企業正在將碳情報直接整合到其營運框架中,以保持競爭力、滿足氣候資訊揭露要求,並與監管機構和利害關係人建立更牢固的關係。日益向分散式、再生能源發電的轉變進一步加速了對先進碳追蹤技術的需求。此外,對ESG標準和綠色融資的日益重視,使得碳管理能力對於確保投資和提升市場信譽至關重要。隨著環境政策的演變和公眾監督的加強,未能將其碳策略與全球預期相符的企業可能會失去市場佔有率和投資者信心。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 29億美元 |

| 預測值 | 76億美元 |

| 複合年成長率 | 10.7% |

隨著分散式和再生能源模式的步伐加快,企業高度依賴精準的碳追蹤系統來實現合規性和內部永續發展目標。精準的報告工具已成為幫助企業滿足氣候相關資訊揭露要求並邁向淨零排放目標不可或缺的工具。科技的快速發展降低了實施碳管理平台的成本和複雜性,即使是規模較小的公用事業公司也能將排放監測納入日常營運。

人工智慧和區塊鏈技術驅動的數位解決方案價格日益親民,進一步推動了市場成長。這些創新技術能夠即時追蹤排放,增強資料報告,提高可擴展性,同時降低營運成本。然而,貿易政策和關稅結構的轉變正在影響供應鏈,導致碳管理解決方案的部署可能出現延遲。一些公司正在探索國內採購或其他生產策略,但此類舉措可能需要額外的時間和資金,這可能會影響全球貿易動態。

預計到2034年,能源和公用事業碳管理系統市場中的解決方案部分將以10%的複合年成長率成長。對於旨在滿足動態監管需求的公用事業公司而言,能夠即時洞察碳排放、能源消耗和環境績效的數位平台正變得至關重要。整合的人工智慧分析和預測模型可協助企業在保持合規性的同時,推動主動的減碳策略。

預計基於雲端的碳管理平台將超過本地部署,到 2034 年的複合年成長率將達到 11%。雲端解決方案提供經濟高效、靈活的工具存取、即時排放審計和無縫可擴展性,幫助公用事業公司以更快的速度和更高的可靠性滿足不斷變化的合規性要求。

2024年,美國能源和公用事業碳管理系統市場規模達8.1億美元,這得益於聯邦和州政府日益成長的監管壓力、ESG合規要求以及利益相關者對碳報告透明度的要求。企業正在將碳情報融入營運之中,以引領永續發展工作並實現雄心勃勃的脫碳目標。

全球能源和公用事業碳管理系統市場的主要參與者包括 Salesforce、Enablon、施耐德電氣、Locus Technologies、Trinity Consultants、Carbon Footprint Ltd.、SAP、New Era Cleantech、Accuvio、IBM、Envirosoft、ESP、Enviance、NativeEnergy、Energy、Daksome Software、Capel、Daksome、Intex、Iativesometrix、Capie、Daksome Software、Capel、Daksome、Capel、Iaksome Software、Capie、Daksome Software、Capel。為了增強市場影響力,各公司正優先考慮數位轉型,大力投資人工智慧驅動的工具、即時排放分析和可自訂的雲端平台,以服務大型企業和中型公用事業公司。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 川普政府關稅對貿易和整體產業的影響

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 創新與永續發展格局

第5章:市場規模及預測:依組件分類,2021 - 2034 年

- 主要趨勢

- 解決方案

- 服務

第6章:市場規模及預測:依部署,2021 - 2034 年

- 主要趨勢

- 雲

- 本地

第7章:市場規模及預測:依地區 2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- Accuvio

- Carbon Footprint Ltd.

- Dakota Software

- Enablon

- EnergyCap.

- Engie

- Enviance

- Envirosoft

- ESP

- IBM

- Intelex

- Isometrix

- Locus Technlogies

- NativeEnergy

- New Era Cleantech

- Salesforce

- SAP

- Schneider Electric

- Trinity Consultants

The Global Energy and Utility Carbon Management System Market reached USD 2.9 billion in 2024 and is projected to grow at a CAGR of 10.7% to reach USD 7.6 billion by 2034, fueled by the tightening of emissions regulations and rising carbon compliance mandates across the energy sector. As industries worldwide push toward aggressive net-zero goals, energy and utility companies are facing mounting pressure to adopt digital carbon management platforms that ensure accurate, real-time tracking of emissions. The market is witnessing a significant transformation, with sustainability becoming a core business imperative rather than an optional initiative.

Companies are integrating carbon intelligence directly into their operational frameworks to maintain competitiveness, meet climate disclosure requirements, and build stronger relationships with regulators and stakeholders. A growing shift toward decentralized, renewable-based power generation further accelerates demand for advanced carbon tracking technologies. Moreover, the increasing emphasis on ESG standards and green financing has made carbon management capabilities essential for securing investments and boosting market credibility. As environmental policies evolve and public scrutiny intensifies, businesses that fail to align their carbon strategies with global expectations risk losing both market share and investor confidence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 billion |

| Forecast Value | $7.6 billion |

| CAGR | 10.7% |

As the transition to decentralized and renewable power models gathers pace, companies rely heavily on precision carbon tracking systems to achieve regulatory compliance and internal sustainability goals. Precision reporting tools have become indispensable for helping firms meet climate-related disclosure mandates and move toward net-zero emissions targets. Rapid technological evolution has lowered the cost and complexity of implementing carbon management platforms, enabling even smaller utilities to integrate emissions monitoring into daily operations.

Market growth is further propelled by the rising affordability of digital solutions powered by artificial intelligence and blockchain technologies. These innovations allow real-time emissions tracking, enhanced data reporting, and improved scalability while also reducing operational overhead. However, shifting trade policies and changing tariff structures are impacting supply chains, causing potential delays in the deployment of carbon management solutions. Some companies are exploring domestic sourcing or alternative production strategies, although such moves may require additional time and capital, potentially affecting global trade dynamics.

The solutions segment within the energy and utility carbon management system market is projected to grow at a CAGR of 10% through 2034. Digital platforms delivering real-time insights into carbon output, energy consumption, and environmental performance are becoming essential for utilities aiming to meet dynamic regulatory demands. Integrated AI analytics and predictive modeling help organizations drive proactive carbon mitigation strategies while maintaining compliance.

Cloud-based carbon management platforms are anticipated to outpace on-premises deployments, growing at a CAGR of 11% through 2034. Cloud solutions offer cost-effective, flexible access to tools, real-time emissions auditing, and seamless scalability, helping utilities meet evolving compliance requirements with greater speed and reliability.

The United States Energy and Utility Carbon Management System Market generated USD 810 million in 2024, driven by mounting federal and state regulatory pressure, ESG compliance mandates, and stakeholder demands for transparency in carbon reporting. Companies are embedding carbon intelligence into operations to lead sustainability efforts and achieve ambitious decarbonization targets.

Major players in the Global Energy and Utility Carbon Management System Market include Salesforce, Enablon, Schneider Electric, Locus Technologies, Trinity Consultants, Carbon Footprint Ltd., SAP, New Era Cleantech, Accuvio, IBM, Envirosoft, ESP, Enviance, NativeEnergy, EnergyCap, Dakota Software, Intelex, Isometrix, and Engie. To strengthen market presence, companies are prioritizing digital transformation, investing heavily in AI-driven tools, real-time emissions analytics, and customizable, cloud-based platforms to serve both large enterprises and mid-sized utilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Impact of trump administration tariffs on trade & overall industry

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Solutions

- 5.3 Services

Chapter 6 Market Size and Forecast, By Deployment, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Size and Forecast, By Region 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Accuvio

- 8.2 Carbon Footprint Ltd.

- 8.3 Dakota Software

- 8.4 Enablon

- 8.5 EnergyCap.

- 8.6 Engie

- 8.7 Enviance

- 8.8 Envirosoft

- 8.9 ESP

- 8.10 IBM

- 8.11 Intelex

- 8.12 Isometrix

- 8.13 Locus Technlogies

- 8.14 NativeEnergy

- 8.15 New Era Cleantech

- 8.16 Salesforce

- 8.17 SAP

- 8.18 Schneider Electric

- 8.19 Trinity Consultants