|

市場調查報告書

商品編碼

1740953

銅和黃銅扁平材市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Copper And Brass Flat Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

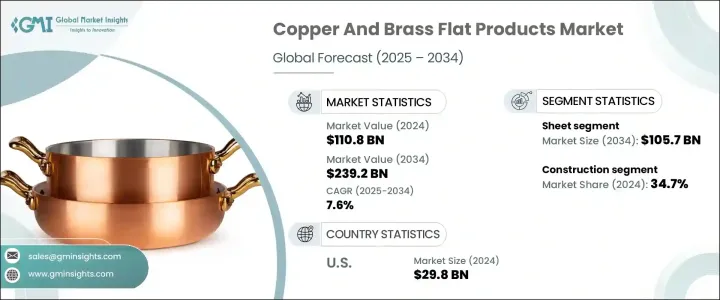

2024年,全球銅和黃銅扁平材市場規模達1,108億美元,預計2034年將以7.6%的複合年成長率成長,達到2,392億美元。全球基礎設施投資和工業發展不斷成長,推動了對這些金屬產品的需求。銅和黃銅因其優異的導電性、耐腐蝕性和在眾多應用中的適應性而廣受歡迎。電動車、再生能源系統的日益普及以及電子產業的持續技術進步,推動了市場穩步擴張。電氣和電子元件對銅的依賴性也日益增強,這得益於銅的卓越性能。

此外,眾多產業對能源效率和先進工程技術的追求,進一步推動了對銅和黃銅扁平材的需求。隨著各行各業持續將節能放在首位,這些金屬在需要最佳性能和長期耐用性的應用中的應用日益廣泛。銅和黃銅以其優異的導熱性和導電性而聞名,這使得它們成為需要高效管理熱量和能源的系統和組件的理想選擇。例如,在工業機械中,銅和黃銅扁平材通常用於熱交換器、散熱器和冷卻系統,其高效的導熱能力有助於最佳化能源利用並防止過熱。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1108億美元 |

| 預測值 | 2392億美元 |

| 複合年成長率 | 7.6% |

在銅和黃銅扁平材市場的所有產品類型中,板材已成為領先細分市場,2024 年市場價值達 497 億美元。預計該細分市場將大幅成長,到 2034 年將達到 1,057 億美元。銅和黃銅板材因其柔韌性、易加工性和多功能性而備受青睞,在許多行業中備受追捧。這些材料以其卓越的強度、延展性和美觀性而聞名,所有這些都使其得到了廣泛的應用。它們易於切割、成型和加工成各種尺寸和形狀,使其能夠適應各種應用。

建築業對銅和黃銅板材的需求尤其高,該行業是最大的市場驅動力,佔34.7%。這些材料是現代建築結構和裝飾元素不可或缺的一部分。銅和黃銅板材以及帶材和板材廣泛用於屋頂系統、牆面覆層、簷槽、落水管以及門窗框架的建造。它們的耐腐蝕性使其成為對耐用性和使用壽命至關重要的外部應用的理想選擇。此外,它們兼具美觀性,包括溫暖、光澤的外觀,使其成為建築細節設計的熱門選擇,例如裝飾性特徵和裝飾性立面。隨著全球城鎮化進程的持續加速,預計對銅和黃銅板材的需求將快速成長。

2024年,美國銅和黃銅扁平材市場規模達298億美元,預計2025年至2034年複合年成長率為7.4%。美國對銅和黃銅扁平材的高需求與電動車、再生能源和現代通訊系統等先進技術的擴張息息相關。銅在散熱和高效輸電方面發揮著重要作用,使其成為新興科技基礎設施不可或缺的材料。因此,預計美國在未來幾年仍將是銅和黃銅扁平材的主要消費國。

全球銅和黃銅扁平材市場的領導者包括 Global Copper Conductors、Gujarat Copper Alloys Ltd、Aurubis、Chhajed Steel Limited 和 KME Copper。為了擴大市場佔有率並保持競爭力,主要參與者正在實施多項有效策略。企業投資先進的製造技術,以提高精度、品質和產量。策略夥伴關係和收購有助於擴大其地域覆蓋範圍和產品組合。永續性是企業關注的重點,企業採用環保的生產方法和可回收材料。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(銷售價格)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 2021-2024年主要出口國

- 2021-2024年主要進口國

註:以上貿易統計僅提供重點國家

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 餐飲和酒店業的需求不斷成長

- 生質能發電的成長

- 電子商務和直接面對消費者的銷售擴張

- 產業陷阱與挑戰

- 森林砍伐與監管限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場規模及預測:依木材類型,2021 - 2034

- 主要趨勢

- 原木

- 木屑

- 顆粒

- 林業殘留物

- 其他

第6章:市場規模及預測:依最終用途,2021 - 2034

- 主要趨勢

- 食品服務

- 配電

- 其他

第7章:市場規模及預測:按配銷通路,2021 - 2034

- 主要趨勢

- 大型超市和超市

- 專賣店

- 電子商務

- 企業對企業 (B2B)

- 其他

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Cornish Firewood

- Firewood Fuel

- Lost Coast Forest Products

- JB Firewood

- Pinnacle Firewood Company

- Surefire Wood

- Wilson Enterprises

- Cutting Edge Firewood

- Wood Step

- The Log Store Group

- Woodmill

- Premier Firewood Company

- UAB Vli Timber

- Woodbioma

The Global Copper and Brass Flat Products Market was valued at USD 110.8 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 239.2 billion by 2034, driven by the rising investments in infrastructure and industrial development worldwide drives the growing demand for these metal products. Copper and brass are widely chosen for their excellent conductivity, corrosion resistance, and adaptability in numerous applications. The rising popularity of electric vehicles, renewable energy systems, and ongoing technological progress across the electronics sector contribute to steady market expansion. Electrical and electronic components increasingly rely on copper due to their superior performance.

Moreover, the drive toward energy efficiency and advanced engineering across numerous industries is further boosting the demand for copper and brass flat products. As industries continue to prioritize energy savings, these metals are being increasingly utilized in applications that require optimal performance and long-term durability. Copper and brass are known for their excellent thermal and electrical conductivity, which makes them ideal for systems and components that need to efficiently manage heat and energy. For example, in industrial machinery, copper and brass flat products are commonly used in heat exchangers, radiators, and cooling systems, where their ability to conduct heat effectively helps optimize energy use and prevent overheating.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.8 Billion |

| Forecast Value | $239.2 Billion |

| CAGR | 7.6% |

Among the product types in the copper and brass flat products market, the sheets segment has emerged as the leading segment, with a market value of USD 49.7 billion in 2024. This segment is expected to grow significantly, reaching USD 105.7 billion by 2034. Copper and brass sheets are favored for their flexibility, ease of processing, and versatility, making them highly sought after across numerous industries. These materials are known for their superior strength, malleability, and aesthetic appeal, all contribute to their widespread use. Their ability to be easily cut, shaped, and fabricated into various sizes and forms enables them to be adapted to varied applications.

The demand for copper and brass sheets is particularly high in the construction sector, which is the largest market driver, accounting for 34.7% share. These materials are integral to both structural and decorative elements in modern buildings. Copper and brass sheets, along with strips and plates, are used extensively in the construction of roofing systems, wall cladding, gutters, downspouts, and window and door frames. Their corrosion resistance makes them ideal for exterior applications where durability and longevity are critical. Additionally, their aesthetic qualities, including their warm, lustrous appearance, make them a popular choice for architectural detailing, such as ornamental features and decorative facades. As urbanization continues to accelerate globally, the demand for copper and brass sheets is expected to grow rapidly.

United States Copper and Brass Flat Products Market accounted for USD 29.8 billion in 2024 and is projected to grow at a CAGR of 7.4% from 2025 to 2034. The nation's high demand for copper and brass flat products is tied to the expansion of advanced technologies, including electric mobility, renewable power, and modern communication systems. Copper's role in heat dissipation and efficient power transmission makes it indispensable for emerging tech infrastructure. As a result, the U.S. is expected to remain a leading consumer in the coming years.

Leading companies in the Global Copper and Brass Flat Products Market include Global Copper Conductors, Gujarat Copper Alloys Ltd, Aurubis, Chhajed Steel Limited, and KME Copper. To expand market presence and stay competitive, key players are implementing several effective strategies. Companies invest in advanced manufacturing technologies to improve precision, quality, and output. Strategic partnerships and acquisitions are helping expand their geographical reach and product portfolios. Sustainability is a strong focus, with firms adopting eco-friendly production methods and recyclable materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-Side impact (Selling Price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-Side impact (Raw Materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (USD Mn)

- 3.3.2 Major importing countries, 2021-2024 (USD Mn)

Note: The above trade statistics will be provided for key countries only

- 3.4 Impact on trade

- 3.4.1 Trade volume disruptions

- 3.4.2 Retaliatory measures

- 3.5 Impact on the industry

- 3.5.1 Supply-side impact (raw materials)

- 3.5.1.1 Price volatility in key materials

- 3.5.1.2 Supply chain restructuring

- 3.5.1.3 Production cost implications

- 3.5.2 Demand-side impact (selling price)

- 3.5.2.1 Price transmission to end markets

- 3.5.2.2 Market share dynamics

- 3.5.2.3 Consumer response patterns

- 3.5.1 Supply-side impact (raw materials)

- 3.6 Key companies impacted

- 3.7 Strategic industry responses

- 3.7.1 Supply chain reconfiguration

- 3.7.2 Pricing and product strategies

- 3.7.3 Policy engagement

- 3.8 Outlook and future considerations

- 3.9 Supplier landscape

- 3.10 Profit margin analysis

- 3.11 Key news & initiatives

- 3.12 Regulatory landscape

- 3.13 Impact forces

- 3.13.1 Growth drivers

- 3.13.1.1 Rising demand from food services & hospitality

- 3.13.1.2 Growth in biomass power generation

- 3.13.1.3 E-commerce & direct-to-consumer sales expansion

- 3.13.2 Industry pitfalls & challenges

- 3.13.2.1 Deforestation & regulatory restrictions

- 3.13.1 Growth drivers

- 3.14 Growth potential analysis

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Wood Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Log wood

- 5.3 Wood chips

- 5.4 Pellets

- 5.5 Forestry residues

- 5.6 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Food services

- 6.3 Power distribution

- 6.4 Others

Chapter 7 Market Size and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Hypermarkets and supermarkets

- 7.3 Specialty stores

- 7.4 E-commerce

- 7.5 Business to business

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cornish Firewood

- 9.2 Firewood Fuel

- 9.3 Lost Coast Forest Products

- 9.4 JB Firewood

- 9.5 Pinnacle Firewood Company

- 9.6 Surefire Wood

- 9.7 Wilson Enterprises

- 9.8 Cutting Edge Firewood

- 9.9 Wood Step

- 9.10 The Log Store Group

- 9.11 Woodmill

- 9.12 Premier Firewood Company

- 9.13 UAB Vli Timber

- 9.14 Woodbioma

按應用、形態、作物類型、終端用戶產業和銷售管道的氯氧化銅市場—2025-2032年全球預測銅合金市場按合金類型、形態、終端用戶產業、製造流程和應用分類-2025-2032年全球預測

按應用、形態、作物類型、終端用戶產業和銷售管道的氯氧化銅市場—2025-2032年全球預測銅合金市場按合金類型、形態、終端用戶產業、製造流程和應用分類-2025-2032年全球預測 全球銅合金市場美國連接器用銅合金市場規模、佔有率及趨勢分析報告:依合金類型、最終用途及細分市場預測,2025-2033年連接器用銅合金市場規模、佔有率和趨勢分析報告:按合金類型、最終用途、地區和細分市場預測,2025-2033 年銅扁軋延產品市場規模、佔有率、趨勢分析報告:依產品、最終用途、地區、細分市場預測,2025-2033年美國扁平軋延銅產品市場規模、佔有率、趨勢分析報告:按產品、最終用途和細分市場預測,2025-2033 年

全球銅合金市場美國連接器用銅合金市場規模、佔有率及趨勢分析報告:依合金類型、最終用途及細分市場預測,2025-2033年連接器用銅合金市場規模、佔有率和趨勢分析報告:按合金類型、最終用途、地區和細分市場預測,2025-2033 年銅扁軋延產品市場規模、佔有率、趨勢分析報告:依產品、最終用途、地區、細分市場預測,2025-2033年美國扁平軋延銅產品市場規模、佔有率、趨勢分析報告:按產品、最終用途和細分市場預測,2025-2033 年 全球銅碲合金市場:市場佔有率及排名、總銷售量及需求預測(2025-2031)

全球銅碲合金市場:市場佔有率及排名、總銷售量及需求預測(2025-2031) 壓延銅產品市場規模、佔有率、趨勢、行業分析報告:依產品、應用、厚度和地區,市場預測2025-2034

壓延銅產品市場規模、佔有率、趨勢、行業分析報告:依產品、應用、厚度和地區,市場預測2025-2034 全球黃銅棒市場規模(依產品類型、等級、最終用途、區域範圍和預測)

全球黃銅棒市場規模(依產品類型、等級、最終用途、區域範圍和預測)