|

市場調查報告書

商品編碼

1740916

汽車盤式聯軸器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Disc Couplings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

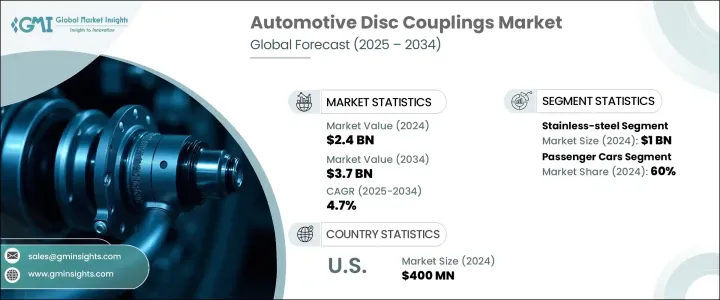

2024年,全球汽車盤式聯軸器市場規模達24億美元,預計2034年將以4.7%的複合年成長率成長,達到37億美元。這得歸功於市場對精密互動式汽車內裝日益成長的需求,以及智慧技術在汽車領域的日益普及。隨著汽車製造商持續向電氣化和自動化轉型,盤式聯軸器已成為支援兼顧功能性和美觀性的高性能系統的關鍵部件。這些零件在連接機械和電子子系統方面發揮著至關重要的作用,尤其是在電動車(EV)和自動駕駛平台中,無縫整合和以用戶為中心的體驗已成為常態。

汽車產業正在快速發展,重點關注下一代出行方式和更智慧的座艙技術。隨著駕駛者偏好轉向更直覺、更沉浸式的駕駛體驗,膜片聯軸器正在協助開發超越傳統開關和控制裝置的創新系統。消費者正在尋找具有觸控響應、多功能表面、整合觸覺和智慧介面的車輛,而膜片聯軸器有助於彌合硬體和軟體之間的差距,從而提高安全性、響應速度和舒適性。汽車製造商擴大採用先進的動力傳動系統和控制技術,這些技術需要可靠、輕量化、高強度的零件,能夠承受惡劣條件、振動和高負載。隨著這種需求的不斷成長,膜片聯軸器正被整合到電動傳動系統、資訊娛樂模組和內部控制系統中,以確保更平穩的運作和更高的能源效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 24億美元 |

| 預測值 | 37億美元 |

| 複合年成長率 | 4.7% |

技術不斷重新定義汽車膜片聯軸器的功能。最新研發成果包括嵌入式感測器和3D觸控表面,順應了智慧汽車系統日益成長的趨勢。這些創新在電動車和自動駕駛汽車領域尤其重要,因為這些汽車的座艙技術正在不斷發展,以提供免持、語音控制和響應迅速的使用者介面。隨著汽車製造商致力於降低傳統控制的複雜性並增強駕駛員互動,膜片聯軸器推動了向簡潔、互動式儀錶板和集中控制中心的轉變。觸覺回饋、動態氛圍照明和自適應資訊娛樂系統等功能依賴精確的機電連接,這使得膜片聯軸器不可或缺。

就材料細分而言,市場包括不銹鋼、鋁和塑膠膜片聯軸器。其中,不鏽鋼以2024年約10億美元的估值佔據市場領先地位。這種優勢源自於其卓越的強度、耐熱性和高耐用性——這些特性是高性能和電動車的關鍵特性。不銹鋼聯軸器能夠有效承受劇烈振動和極端條件,使其成為長期可靠性和性能一致性要求嚴格的應用的理想選擇。隨著汽車製造商強調永續和高輸出動力傳動系統,不銹鋼仍然是工程師在設計高性能和長壽命產品時的首選材料。

根據最終用途,汽車膜片聯軸器市場可分為乘用車和商用車。 2024年,乘用車佔了全球市場的60%。這一強勁成長得益於電動和自動駕駛技術在消費性汽車中的日益普及。原始設備製造商更專注於透過智慧介面、輕量化傳動系統組件和無縫內裝控制系統來最佳化駕駛體驗——所有這些都需要整合堅固耐用的膜片聯軸器系統。從小型電動車到高階自動駕駛汽車,膜片聯軸器確保從資訊娛樂到動力傳輸的每個部件都能平穩安全地運作。

從地區來看,北美汽車盤式聯軸器市場在2024年的產值達到4億美元。美國汽車產業持續引領尖端動力傳動系統技術的實施。美國國內汽車製造商正在大力投資電氣化,並採用先進的盤式聯軸器來提升性能和駕駛舒適度。隨著電動車在美國的普及,對能夠承受電動傳動系統熱負荷和振動的高品質聯軸器的需求正在大幅成長。該地區的研究活動也不斷增加,旨在開發輕量化、高效的零件,以支援汽車電氣化目標。

全球汽車碟式聯軸器市場的主要參與者包括弗蘭德 (Flender)、約翰克蘭 (John Crane)、愛斯科 (ESCO)、鐵姆肯 (Timken)、REICH 和 Rathi Transpower。這些公司正透過策略聯盟、持續的產品創新以及高度重視研發來提升競爭優勢。他們正在投資輕量化、耐腐蝕材料和模組化聯軸器設計,以提高與下一代汽車平台的兼容性。許多參與者還透過整合智慧功能來提升產品性能,以滿足不斷變化的消費者期望以及原始設備OEM)對節能和性能驅動解決方案的要求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 組件提供者

- 製造商

- 技術提供者

- 配銷通路分析

- 最終用途

- 利潤率分析

- 供應商格局

- 川普政府關稅的影響

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 對貿易的影響

- 技術與創新格局

- 專利分析

- 監管格局

- 成本細分分析

- 重要新聞和舉措

- 衝擊力

- 成長動力

- 向電動車和自動駕駛汽車轉變

- 材料和感測技術的進步

- 向電動車和自動駕駛汽車轉變

- OEM客製化與品牌差異化舉措

- 產業陷阱與挑戰

- 開發和整合成本高

- 與舊系統的兼容性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 撓性聯軸器

- 剛性聯軸器

- 膜片聯軸器

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 傳動系統

- 傳動系統

- 動力傳動系統

第8章:市場估計與預測:按材料 2021 - 2034

- 主要趨勢

- 不銹鋼

- 鋁

- 塑膠

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Altra

- ASA Electronics

- Challenge

- Coupling

- CURRAX

- Dodge

- ESCO

- Flender

- John Crane

- Korea Coupling

- Lovejoy

- R+W Coupling

- Rathi Transpower

- Regal Rexnord

- REICH

- RENK-MAAG

- Renold

- Timken

- Tsubakimoto

- Voith

The Global Automotive Disc Couplings Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 3.7 billion by 2034, fueled by the increasing demand for sophisticated, interactive vehicle interiors and the rising integration of smart technologies into the automotive sector. As vehicle manufacturers continue transitioning toward electrification and automation, disc couplings have become vital in supporting high-performance systems that prioritize both functionality and aesthetics. These components play a crucial role in linking mechanical and electronic subsystems, especially in electric vehicles (EVs) and autonomous platforms, where seamless integration and user-centric experiences are now the norm.

The automotive industry is evolving rapidly, with a sharp focus on next-gen mobility and smarter in-cabin technologies. As driver preferences shift toward more intuitive and immersive driving experiences, disc couplings are enabling the development of innovative systems that go beyond traditional switches and controls. Consumers are looking for vehicles that offer touch-responsive, multifunctional surfaces, integrated haptics, and smart interfaces-and disc couplings help bridge the gap between hardware and software, enhancing safety, responsiveness, and comfort. Automakers are increasingly embracing advanced drivetrain and control technologies that demand reliable, lightweight, and high-strength components capable of withstanding harsh conditions, vibrations, and high loads. With this demand on the rise, disc couplings are being integrated into electric drivetrains, infotainment modules, and interior control systems to ensure smoother operation and improved energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 4.7% |

Technology continues to redefine the functionality of automotive disc couplings. The latest developments feature embedded sensors and 3D touch surfaces that align with the growing trend of intelligent vehicle systems. These innovations are particularly relevant in EVs and autonomous vehicles, where in-cabin technology is evolving to deliver hands-free, voice-controlled, and responsive user interfaces. As automakers work to reduce the complexity of traditional controls and enhance driver interaction, disc couplings enable the shift toward clean, interactive dashboards and centralized control hubs. Features like haptic feedback, dynamic ambient lighting, and adaptive infotainment systems rely on precise mechanical-electronic connectivity-making disc couplings indispensable.

In terms of material segmentation, the market includes stainless steel, aluminum, and plastic disc couplings. Among these, stainless steel led the market with a valuation of around USD 1 billion in 2024. This dominance stems from its superior strength, resistance to heat, and high durability-key attributes for use in high-performance and electric vehicles. Stainless steel couplings can efficiently handle intense vibrations and extreme conditions, making them ideal for applications where long-term reliability and performance consistency are non-negotiable. As automakers emphasize sustainable and high-output drivetrains, stainless steel remains the go-to material for engineers designing for performance and longevity.

Based on end use, the automotive disc couplings market is categorized into passenger cars and commercial vehicles. Passenger cars accounted for 60% of the global market in 2024. This stronghold is attributed to the increasing adoption of electric and autonomous technologies in consumer vehicles. OEMs are placing greater focus on optimizing the driving experience with smart interfaces, lightweight drivetrain components, and seamless interior controls-all of which demand the integration of robust disc coupling systems. From compact EVs to high-end autonomous cars, disc couplings ensure that every element, from infotainment to power transmission, operates smoothly and safely.

Regionally, the North America Automotive Disc Couplings Market generated USD 400 million in 2024. The U.S. automotive industry continues to lead with the implementation of cutting-edge drivetrain technologies. Domestic automakers are investing heavily in electrification and are incorporating advanced disc couplings to boost performance and driver comfort. With EV adoption gaining momentum across the U.S., the need for high-quality couplings that can handle thermal loads and vibration in electric drivetrains is growing substantially. This region is also witnessing increased research activity aimed at developing lightweight, efficient components to support vehicle electrification targets.

Key players in the global automotive disc couplings market include Flender, Dodge, Regal Rexnord, RENK-MAAG, Voith, John Crane, ESCO, Timken, REICH, and Rathi Transpower. These companies are sharpening their competitive edge through strategic alliances, continuous product innovation, and a strong emphasis on research and development. They are investing in lightweight, corrosion-resistant materials and modular coupling designs to improve compatibility with next-gen automotive platforms. Many of these players are also advancing product capabilities by integrating smart features that align with evolving consumer expectations and OEM requirements for energy efficiency and performance-driven solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Shift toward electric and autonomous vehicles

- 3.8.1.2 Advancements in material and sensing technology

- 3.8.1.3 Shift toward electric and autonomous vehicles

- 3.8.1.4 OEM initiatives for customization and brand differentiation

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development and integration costs

- 3.8.2.2 Compatibility issues with legacy systems

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Flexible couplings

- 5.3 Rigid couplings

- 5.4 Disc couplings

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Drivetrain system

- 7.3 Transmission system

- 7.4 Powertrain system

Chapter 8 Market Estimates & Forecast, By Material 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Stainless steel

- 8.3 Aluminum

- 8.4 Plastic

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Altra

- 10.2 ASA Electronics

- 10.3 Challenge

- 10.4 Coupling

- 10.5 CURRAX

- 10.6 Dodge

- 10.7 ESCO

- 10.8 Flender

- 10.9 John Crane

- 10.10 Korea Coupling

- 10.11 Lovejoy

- 10.12 R+W Coupling

- 10.13 Rathi Transpower

- 10.14 Regal Rexnord

- 10.15 REICH

- 10.16 RENK-MAAG

- 10.17 Renold

- 10.18 Timken

- 10.19 Tsubakimoto

- 10.20 Voith