|

市場調查報告書

商品編碼

1740915

乳製品混合市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dairy Blends Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

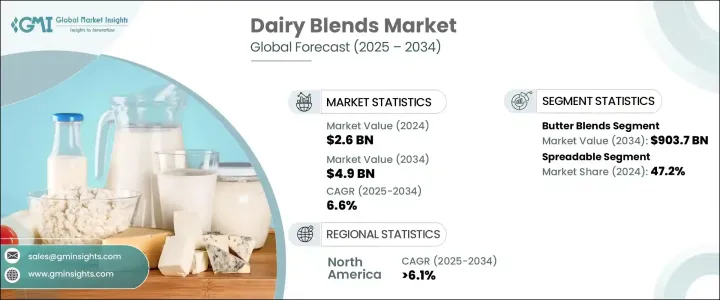

2024年,全球乳製品混合市場規模達26億美元,預計到2034年將以6.6%的複合年成長率成長,達到49億美元,這得益於對滿足現代消費模式的多功能食品配料日益成長的需求。如今,消費者越來越追求兼顧口味、營養和便利性的食品選擇,而乳製品混合市場恰好滿足了這一需求。這種轉變源自於人們日益增強的健康意識、對即食產品的青睞、以及對永續且令人愉悅的飲食體驗的追求。乳製品混合市場完美地融合了這一平衡點——它們將傳統乳製品的豐富感官吸引力與額外的功能性和健康益處相結合。這些產品口感較佳,保存期限較長,熱穩定性較高,塗抹性較強。這些特性使乳製品混合市場成為各種食品應用的理想選擇,從冷凍食品、烘焙食品到醬料和零食。隨著全球食品偏好的演變,消費者越來越傾向於選擇易於融入日常膳食且營養成分個人化的乳製品混合市場。

由於科技的重大進步,乳製品配方正在快速發展。均質化、微膠囊化和精準混合技術的突破,使製造商能夠生產出滿足特定健康目標或飲食需求的配方。無論是降低脂肪含量、添加維生素,或是為兒童、運動員或老年人定製配方,乳製品行業如今都擁有提供精準營養的工具。人們對健康的關注比以往任何時候都更加強烈,這些量身定做的解決方案正在幫助消費者在不犧牲風味和口感的情況下實現個人健康目標。全球供應鏈多元化是另一個促進因素。企業如今在採購和生產方面更加靈活,這有助於它們快速適應原料價格波動、貿易動態以及氣候相關挑戰。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 26億美元 |

| 預測值 | 49億美元 |

| 複合年成長率 | 6.6% |

市場按類型細分為精緻奶油、奶油、起司、優格和其他特殊混合產品。其中,奶油混合產品市場影響力強勁,預計到2034年將達到9.037億美元,複合年成長率為6.5%。這些混合產品因其穩定的質地、風味以及穩定產品配方(尤其是在烘焙和包裝食品中)的能力,在食品加工領域備受推崇。

就形態而言,乳製品混合物可分為粉狀、液態和塗抹型產品。塗抹型混合物佔據主導地位,市佔率達47.2%,預計到2034年將達到12億美元,複合年成長率為6.9%。塗抹型混合物使用方便,與快節奏的生活方式相得益彰,用途廣泛,從直接塗抹到醬料和餐食套裝,都深受消費者喜愛。

預計2025年至2034年間,北美混合乳製品市場的複合年成長率將達到6.1%,這得益於該地區向健康、植物性飲食的轉變。添加大豆、燕麥或杏仁成分的混合乳製品正受到那些尋求清潔標籤、功能性傳統乳製品替代品的消費者的青睞。人們對風味增強、營養豐富且耐儲存的食品的需求不斷成長,進一步推動了市場成長。

嘉吉、Agropur、菲仕蘭坎皮納、凱裡集團、恆天然、Dohler 和 AFP 等領先企業正在加大研發投入,力求提供更乾淨的標籤和更高的營養價值。透過策略合作和以永續發展為重點的舉措,這些企業正在擴大其全球影響力,同時滿足消費者對負責任採購和減少環境影響的期望。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 主要出口國

- 主要進口國

註:以上貿易統計僅提供重點國家

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 消費者喜歡脂肪和膽固醇含量較低的乳製品混合物。

- 功能性食品需求不斷成長

- 混合乳製品是合適的替代品

- 產業陷阱與挑戰

- 嚴格的標籤和成分法律可能會限制市場擴張。

- 一些買家認為混合乳製品的品質比純乳製品低。

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 奶油混合物

- 奶油混合物

- 混合優格

- 起司混合物

- 其他混合

第6章:市場估計與預測:依形式,2021 - 2034 年

- 主要趨勢

- 可塗抹

- 液體

- 粉末

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 烘焙和糖果

- 乳製品和冷凍甜點

- 飲料

- 營養和功能性食品

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Kerry Group plc

- FrieslandCampina

- Cargill, Incorporated

- Fonterra Co-operative Group Limited

- Dohler GmbH

- Agropur

- AFP advanced food products llc

- Cape Food Ingredients

- Intermix Australia Pty Ltd.

- Spectrum Organics Products, LLC

The Global Dairy Blends Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 4.9 billion by 2034, fueled by the rising demand for multi-functional food ingredients that meet modern consumption patterns. Consumers today are increasingly looking for food options that offer a balance between taste, nutrition, and convenience, and dairy blends deliver on all fronts. This shift is being driven by a growing awareness of health, a busy lifestyle that favors ready-to-use products, and a desire for sustainable yet indulgent eating experiences. Dairy blends strike that perfect middle ground-they combine the rich sensory appeal of traditional dairy with added functionality and health benefits. These products provide improved mouthfeel, longer shelf life, thermal stability, and enhanced spreadability. These attributes make dairy blends ideal for a wide range of food applications, from frozen and baked goods to sauces and snacks. As global food preferences evolve, consumers are turning to blends that are easy to incorporate into their daily meals while offering tailored nutritional profiles.

Dairy blends are evolving quickly, thanks to major advancements in technology. Breakthroughs in homogenization, microencapsulation, and precision blending are allowing manufacturers to create blends that target specific health goals or dietary requirements. Whether it's lowering fat content, enriching with vitamins, or customizing blends for children, athletes, or the elderly, the industry now has the tools to deliver precision nutrition. The focus on wellness is stronger than ever, and these tailored solutions are helping consumers meet personal health targets without giving up flavor or texture. Global supply chain diversification is another driving factor. Companies are now more agile in their sourcing and production, helping them adapt quickly to fluctuations in raw material prices, trade dynamics, and climate-related challenges.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 6.6% |

The market is segmented by type into refined creams, butter, cheese, yogurt, and other specialty blends. Among these, butter blends are making a strong impact and are expected to reach USD 903.7 million by 2034, growing at a CAGR of 6.5%. These blends are highly valued in the food processing sector for their consistent texture, flavor, and ability to stabilize product formulations, particularly in baked and packaged foods.

In terms of form, dairy blends are categorized as powders, liquids, and spreadable products. Spreadable blends dominate with a 47.2% market share and are projected to hit USD 1.2 billion by 2034, growing at a CAGR of 6.9%. Their ease of use, compatibility with fast-paced lifestyles, and versatility in everything from direct spreads to sauces and meal kits make them a consumer favorite.

North America's dairy blends market is forecasted to grow at a CAGR of 6.1% between 2025 and 2034, supported by the region's shift toward health-conscious, plant-forward diets. Blends incorporating soy, oat, or almond elements are gaining traction among those seeking clean-label, functional alternatives to traditional dairy. The rising demand for flavor-enhancing, nutrient-rich, and shelf-stable foods further boosts market growth.

Leading companies such as Cargill, Agropur, Friesland Campina, Kerry Group, Fonterra, Dohler, and AFP are pushing the envelope with R&D investments aimed at delivering cleaner labels and higher nutritional value. Through strategic collaborations and sustainability-focused initiatives, these players are expanding their global footprint while meeting consumer expectations for responsible sourcing and reduced environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: The above trade statistics will be provided for key countries only

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Consumers prefer dairy blends for lower fat and cholesterol content.

- 3.8.1.2 Growing demand for functional foods

- 3.8.1.3 Dairy blends offer a suitable alternative

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Strict labeling and composition laws can limit market expansion.

- 3.8.2.2 Some buyers see blends as lower quality than pure dairy.

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy cream blends

- 5.3 Butter blends

- 5.4 Yogurt blends

- 5.5 Cheese blends

- 5.6 Other blends

Chapter 6 Market Estimates & Forecast, By Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Spreadable

- 6.3 Liquid

- 6.4 Powder

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery & confectionery

- 7.3 Dairy & frozen desserts

- 7.4 Beverages

- 7.5 Nutritional & functional foods

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Kerry Group plc

- 9.2 FrieslandCampina

- 9.3 Cargill, Incorporated

- 9.4 Fonterra Co-operative Group Limited

- 9.5 Dohler GmbH

- 9.6 Agropur

- 9.7 AFP advanced food products llc

- 9.8 Cape Food Ingredients

- 9.9 Intermix Australia Pty Ltd.

- 9.10 Spectrum Organics Products, LLC