|

市場調查報告書

商品編碼

1740908

熱塑性膠黏膜市場機會、成長動力、產業趨勢分析及2025-2034年預測Thermoplastic Adhesive Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

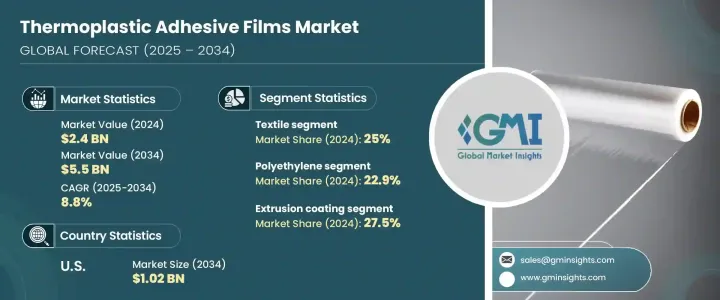

2024年,全球熱塑性膠黏膜市場規模達24億美元,預計到2034年將以8.8%的複合年成長率成長,達到55億美元。這一成長趨勢主要源自於多個終端產業對輕量化材料的日益青睞,尤其是在汽車和電子製造業。熱塑性膠黏膜正擴大用於黏合零件,同時顯著降低產品整體重量。它們能夠支持燃油效率目標並有助於減少排放,這與全球日益嚴格的環境法規和永續發展基準相契合。

在緊湊型電子產品和穿戴式裝置中,這些薄膜具有出色的耐熱性,這對於在微型高密度產品設計中保持性能至關重要。它們能夠在智慧型手機、軟性電子設備和下一代消費設備等空間受限的應用中實現清潔加工和可靠黏合。此外,醫療技術領域正在成為一個潛力巨大的新興領域,生物相容性、耐化學性和易於滅菌至關重要。這些薄膜可用於各種醫療穿戴式裝置和一次性醫療保健產品,提供持久且非侵入性的黏合。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 24億美元 |

| 預測值 | 55億美元 |

| 複合年成長率 | 8.8% |

永續性正成為塑造需求的核心主題。熱塑性膠黏膜因其無溶劑和可回收特性,被視為環保解決方案,非常適合那些尋求最大限度減少揮發性有機化合物 (VOC) 排放的行業。製造商擴大採用環保型膠合劑替代品,以符合監管框架以及環境、社會和治理 (ESG) 目標。薄膜流延和熱熔應用等加工技術的進步,提高了膠黏膜的熱性能、密封性和黏性,使其在工業層壓板和光學系統等高精度要求領域的應用範圍不斷擴大。

就材料細分而言,2024 年的市場包括聚乙烯、聚醯胺、熱塑性聚氨酯、聚酯、聚丙烯、聚烯烴和其他材料類型。 2024 年市值為 24 億美元,預計到 2034 年將大幅成長至 55 億美元。其中,聚乙烯佔 2024 年總佔有率的 22.9%,主要原因是其價格實惠、柔韌性好,且能與各種基材良好黏合。聚乙烯用於包裝和汽車等領域,但隨著各行各業轉向更先進的高性能薄膜,其成長率仍然溫和。熱塑性聚氨酯憑藉其彈性、透明度和優異的耐磨性,正經歷著顯著的發展動能。對小型化和軟性組件日益成長的需求,支持了其在新興應用領域的應用。

從技術面來看,2024 年的市場細分為擠出塗覆、熱熔膠、樹脂共混、薄膜流延和其他加工技術。擠出塗覆法憑藉其高速生產能力和在各種基材上始終如一的塗層質量,以 27.5% 的市場佔有率佔據該細分市場的首位。熱熔膠因其無溶劑、環保特性和可靠的黏合強度而迅速發展,尤其是在電子和衛生相關產品領域。樹脂共混雖然有利於客製化薄膜特性(例如黏性和耐熱性),但由於配方要求複雜且生產成本較高而受到限制。薄膜流延在高精度環境中越來越受歡迎,因為在這些環境中,光滑、無缺陷的薄膜至關重要,尤其是在光學和醫療級應用中。

以2024年的最終用途分析,市場可分為紡織、汽車、電子電氣、醫療、防彈、建築和其他領域。隨著服裝、家居和智慧紡織品對無縫層壓的需求不斷成長,紡織業佔據了25%的市場佔有率,佔據主導地位。黏合膜在無溶劑紡織品黏合解決方案中發揮關鍵作用。在汽車領域,對輕量化的追求以及降低噪音、振動和聲振粗糙度(NVH)的需求增強了這些薄膜的重要性。醫療應用也在快速發展,尤其是用於健康監測設備和診斷工具的皮膚敏感型和可滅菌薄膜。防彈和國防應用利用高強度薄膜作為防護複合材料的分層材料。

從地區來看,美國在2024年佔據全球市場的17.8%,價值約4.3億美元,預計2034年將成長至10.2億美元。這一主導地位得益於熱塑性膠黏膜在汽車、航太、醫療和電子等先進製造業領域的日益普及。美國對無溶劑膠黏劑的重視及其扶持性政策環境,包括貿易法規和國內採購策略的調整,正在推動本土生產和創新。

推動產業競爭的主要參與者包括陶氏公司、3M 公司、巴斯夫公司、漢高公司和科思創公司等公司,它們各自採用不同的方法來加強其市場地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 汽車輕量化需求不斷成長

- 消費性電子產品和穿戴式裝置的成長

- 醫療器材產業的擴張

- 越來越青睞永續黏合劑

- 薄膜流延與熱熔技術進步

- 紡織業創新不斷湧現(例如智慧紡織品)

- 產業陷阱與挑戰

- 原料成本高(例如TPU、聚醯胺)

- 與熱固性塑膠相比,耐熱性和耐化學性有限

- 多層結構的複雜可回收性

- 成長動力

- 川普政府關稅的影響—結構化概述

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 聚乙烯

- 聚醯胺

- 熱塑性聚氨酯

- 聚酯纖維

- 聚丙烯

- 聚光學透鏡

- 其他材料

第6章:市場估計與預測:依技術分類,2021 年至 2034 年

- 主要趨勢

- 擠壓塗層

- 熱熔膠

- 樹脂混合

- 電影選角

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 紡織品

- 汽車

- 電氣和電子

- 醫療的

- 防彈保護

- 建造

- 其他最終用途

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- 3M Company

- Arkema SA

- Ashland Global

- Avery Dennison

- BASF SE

- Covestro AG

- Dow Inc.

- DuPont

- EMS-Chemie Holding AG

- HB Fuller

- Henkel AG

- Huntsman Corporation

- Mitsui Chemicals Inc.

- Sika AG

The Global Thermoplastic Adhesive Films Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 5.5 billion by 2034. This upward trend is largely fueled by the growing preference for lightweight materials across several end-use industries, especially in automotive and electronics manufacturing. Thermoplastic adhesive films are being increasingly used to bond components while significantly reducing overall product weight. Their ability to support fuel efficiency goals and contribute to reduced emissions aligns well with tightening environmental regulations and sustainability benchmarks globally.

In compact electronics and wearable devices, these films offer excellent thermal resistance, which is essential for maintaining performance in miniature, high-density product designs. They allow for clean processing and reliable bonding in space-constrained applications such as smartphones, flexible gadgets, and next-gen consumer devices. Additionally, the medical technology sector is emerging as a high-potential area, where biocompatibility, chemical resistance, and easy sterilization are vital. These films are used in a variety of medical wearables and disposable healthcare products, delivering durable yet non-invasive adhesion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 8.8% |

Sustainability is becoming a central theme in shaping demand. Thermoplastic adhesive films are seen as an eco-conscious solution due to their solvent-free nature and recyclability, making them suitable for industries seeking to minimize VOC emissions. Manufacturers are increasingly adopting environmentally friendly adhesive alternatives to align with regulatory frameworks and environmental, social, and governance (ESG) goals. Advances in processing technologies like film casting and hot melt applications have improved the thermal behavior, sealing ability, and tack properties of adhesive films, expanding their use in areas that demand high precision, such as industrial laminates and optical systems.

In terms of material segmentation, the market in 2024 includes polyethylene, polyamide, thermoplastic polyurethane, polyester, polypropylene, polyolefins, and other material types. With the market valued at USD 2.4 billion in 2024, it is forecast to grow substantially and reach USD 5.5 billion by 2034. Among these, polyethylene accounted for 22.9% of the total share in 2024, primarily due to its affordability, flexibility, and ability to bond well with various substrates. It is used in sectors like packaging and automotive, although its growth rate remains modest as industries shift toward more advanced performance films. Thermoplastic polyurethane is experiencing significant momentum thanks to its elasticity, transparency, and superior abrasion resistance. The growing need for miniaturized and flexible components is supporting its adoption across emerging applications.

From a technology standpoint, the 2024 market is segmented into extrusion coating, hot melt adhesives, resin blending, film casting, and other processing techniques. The extrusion coating method led the segment with a 27.5% market share due to its high-speed production capability and consistent coating quality across various substrates. Hot melt adhesives are expanding quickly, especially in electronics and hygiene-related products, driven by their solvent-free, environmentally sound properties and dependable bond strength. Resin blending, while advantageous for customizing film characteristics like tack and heat resistance, faces constraints due to complex formulation requirements and elevated production costs. Film casting is finding preference in high-precision environments where smooth, defect-free films are essential, particularly for optical and medical-grade applications.

When analyzed by end use in 2024, the market is divided into textiles, automotive, electrical and electronics, medical, ballistic protection, construction, and other sectors. The textile industry led with a 25% share, as demand rises for seamless lamination in garments, home furnishings, and smart textiles. Adhesive films are playing a key role in solvent-free textile bonding solutions. In the automotive domain, the push for lighter vehicles and the need to mitigate noise, vibration, and harshness (NVH) have reinforced the relevance of these films. Medical uses are also advancing rapidly, particularly in skin-sensitive and sterilizable films for health-monitoring devices and diagnostic tools. Ballistic and defense applications leverage high-strength films for layering purposes in protective composites.

Regionally, the United States held a 17.8% share in the global market in 2024, valued at approximately USD 430 million, and is projected to grow to USD 1.02 billion by 2034. This dominance is attributed to the increasing penetration of thermoplastic adhesive films in advanced manufacturing sectors like automotive, aerospace, medical, and electronics. The country's focus on solvent-free adhesives and its supportive policy environment, including adjustments in trade regulations and domestic sourcing strategies, are boosting local production and innovation.

Major players driving competition in the industry include companies like Dow Inc., 3M Company, BASF SE, Henkel AG, and Covestro AG, each adopting different approaches to strengthen their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand in automotive lightweighting

- 3.6.1.2 Growth in consumer electronics and wearables

- 3.6.1.3 Expansion of the medical device industry

- 3.6.1.4 Increasing preference for sustainable adhesives

- 3.6.1.5 Technological advancements in film casting and hot melt

- 3.6.1.6 Rising textile industry innovations (e.g., smart textiles)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High raw material costs (e.g., TPU, polyamide)

- 3.6.2.2 Limited heat and chemical resistance compared to thermosets

- 3.6.2.3 Complex recyclability of multi-layer structures

- 3.6.1 Growth drivers

- 3.7 Impact of trump administration tariffs – structured overview

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.4.4 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.3 Polyamide

- 5.4 Thermoplastics polyurethane

- 5.5 Polyester

- 5.6 Polypropylene

- 5.7 Polyolens

- 5.8 Other materials

Chapter 6 Market Estimates and Forecast, By Technologies, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Extrusion coating

- 6.3 Hot melt adhesive

- 6.4 Resin blending

- 6.5 Film casting

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textile

- 7.3 Automotive

- 7.4 Electrical and electronics

- 7.5 Medical

- 7.6 Ballistic protection

- 7.7 Construction

- 7.8 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Arkema SA

- 9.3 Ashland Global

- 9.4 Avery Dennison

- 9.5 BASF SE

- 9.6 Covestro AG

- 9.7 Dow Inc.

- 9.8 DuPont

- 9.9 EMS-Chemie Holding AG

- 9.10 H.B. Fuller

- 9.11 Henkel AG

- 9.12 Huntsman Corporation

- 9.13 Mitsui Chemicals Inc.

- 9.14 Sika AG