|

市場調查報告書

商品編碼

1740903

數位故障記錄器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Digital Fault Recorder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

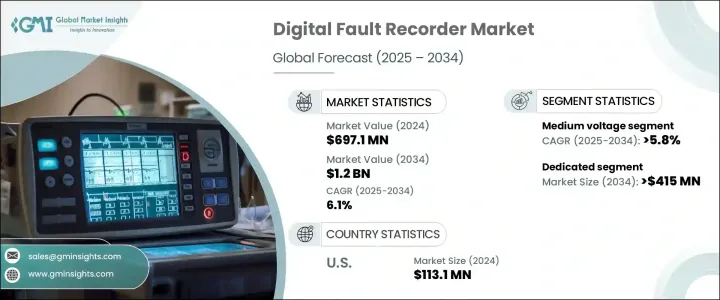

2024年,全球數位故障記錄器市場規模達6.971億美元,預計隨著電力基礎設施的大規模現代化,該市場規模將以6.1%的複合年成長率成長,到2034年達到12億美元。隨著能源系統從傳統模式向智慧自動化網路演進,精確監控和快速故障診斷的需求變得比以往任何時候都更加重要。數位故障記錄器(DFR)正成為這個轉型過程中不可或缺的工具,它為公用事業公司提供電網行為的即時洞察,使其能夠快速做出營運決策,最大限度地減少停電,並保持穩定的電力傳輸。

現代電力系統正在整合更多再生能源、分散式能源資產和智慧技術,從而建立高度複雜的網路。這種複雜性需要超越傳統功能的先進診斷工具。數位故障記錄器透過提供高速資料採集、遠端系統存取和進階分析功能來滿足這些要求。它們使公用事業公司能夠執行詳細的事件重建並精確定位故障根源,不僅可以減少停機時間,還可以提高電網的長期效率。數位變電站和智慧電網解決方案的廣泛應用正在加速這一趨勢,進一步推動對智慧、響應迅速的故障檢測系統的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6.971億美元 |

| 預測值 | 12億美元 |

| 複合年成長率 | 6.1% |

隨著產業重點轉向彈性和營運透明度,數位故障記錄器 (DFR) 在電力管理策略中發揮越來越重要的作用。其數位架構可無縫整合到更廣泛的控制系統中,使其在現代電網環境中具有高度適應性。數位故障記錄器能夠自動收集資料並提供可操作的洞察,使公用事業公司能夠實現更精簡、更具預測性的維護方案。這符合全球能源目標,即專注於電網可靠性、永續電力分配和經濟高效的基礎設施升級。

然而,數位故障記錄器產業也難以免受到宏觀經濟壓力的影響。對進口商品徵收的關稅,尤其是與電子產品、鋼鐵和鋁相關的商品,正在影響各行各業的零件成本。由於數位故障記錄器包含半導體、通訊模組和金屬外殼,這些投入的任何價格波動都可能影響生產成本和利潤率。市場參與者必須透過最佳化供應鏈、投資在地化製造以及追求減少對敏感材料依賴的設計創新來應對這些挑戰。

就產品類型而言,專用DFR細分市場預計到2034年將創造超過4.15億美元的市場價值。這些設備專為故障記錄而設計,比多功能系統具有更高的精度和穩定性。專用記錄器設計為獨立於其他電網控制元件運行,在對不間斷性能至關重要的高可靠性裝置中尤其重要。其精確度和專注的功能使其成為需要可靠故障檢測且不受輔助製程干擾的行業的首選。

中壓類別通常涵蓋1kV至36kV的系統,預計到2034年,其複合年成長率將超過5.8%。這一成長是由配電網、工業營運以及可再生能源整合設施對故障監控日益成長的需求所推動的。公用事業公司正在積極升級傳統電網基礎設施,透過嵌入數位監控工具來提高故障定位精度並減少服務中斷。因此,分散式故障復原器 (DFR) 正成為中壓電網現代化專案的關鍵組件,其支援本地診斷和遙測的能力可增強系統可靠性。

在美國,數位故障記錄器市場持續穩定發展。 2022年,該市場規模達1.035億美元,2023年攀升至1.081億美元,2024年再次回升至1.131億美元。老化基礎設施升級的投資不斷增加,加上電網對極端天氣事件和波動性能源需求的脆弱性增加,促使公用事業公司採用更複雜的故障分析解決方案。其重點是確保營運連續性,並保護電網免受可預測和意外中斷的影響。

行業領導者憑藉廣泛的全球營運和成熟的研發能力保持競爭優勢。市佔率超過 20% 的公司在北美、歐洲和亞洲等關鍵地區擁有生產基地。他們的全球佈局使其能夠實現經濟高效的生產和快速的產品交付。憑藉其在創新和可靠性方面的長期聲譽,這些公司預計將在數位故障記錄器行業深入數位化時代之際,影響其發展軌跡。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 戰略儀表板

- 創新與永續發展格局

第5章:市場規模及預測:依類型,2021 - 2034

- 主要趨勢

- 投入的

- 多功能的

第6章:市場規模及預測:按電壓,2021 - 2034

- 主要趨勢

- 中壓

- 高壓

- 超高壓

第7章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 高速擾動

- 低速擾動

- 穩定狀態

第 8 章:市場規模與預測:按安裝量,2021 年至 2034 年

- 主要趨勢

- 世代

- 傳染

- 分配

第9章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第10章:公司簡介

- ABB

- Ametek

- Ducati Energia

- Eaton

- Elspec

- E-Max Instruments

- Erlphase

- General Electric

- Hitachi

- Kinkei

- Kocos

- Logiclab

- Mehta Tech

- Qualitrol

- Schneider Electric

- Siemens

The Global Digital Fault Recorder Market was valued at USD 697.1 million in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.2 billion by 2034 as power infrastructure undergoes widespread modernization. As energy systems evolve from traditional models to intelligent, automated networks, the need for precise monitoring and rapid fault diagnosis is becoming more critical than ever. DFRs are emerging as indispensable tools in this transformation, offering utilities real-time insight into grid behavior, allowing them to make swift operational decisions, minimize outages, and maintain consistent power delivery.

Modern electrical systems are integrating more renewable energy sources, distributed energy assets, and smart technologies, creating highly complex networks. This complexity demands advanced diagnostic tools that go beyond conventional capabilities. Digital fault recorders meet these requirements by offering high-speed data capture, remote system access, and advanced analytics. They enable utilities to perform detailed event reconstruction and pinpoint the origin of faults, which not only reduces downtime but also enhances long-term grid efficiency. The widespread adoption of digital substations and smart grid solutions is accelerating this trend, further boosting demand for intelligent, responsive fault detection systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $697.1 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.1% |

As industry priorities shift toward resilience and operational transparency, DFRs are playing an increasingly vital role in power management strategies. Their digital architecture allows seamless integration into broader control systems, making them highly adaptable in modern grid environments. With their ability to automate data collection and provide actionable insights, digital fault recorders are empowering utilities to achieve more streamlined and predictive maintenance regimes. This aligns with global energy goals focused on grid reliability, sustainable power distribution, and cost-effective infrastructure upgrades.

However, the DFR industry is not immune to macroeconomic pressures. Tariffs introduced on imported goods, particularly those related to electronics, steel, and aluminum, are impacting component costs across various industrial sectors. Since digital fault recorders include semiconductors, communication modules, and metal casings, any price volatility in these inputs can influence production costs and profit margins. Market participants must navigate these challenges by optimizing supply chains, investing in localized manufacturing, and pursuing design innovations that reduce dependency on sensitive materials.

In terms of product types, the dedicated DFR segment is expected to generate more than USD 415 million by 2034. These devices are purpose-built for fault recording and offer higher accuracy and stability than multifunctional systems. Designed to operate independently of other grid control elements, dedicated recorders are especially valued in high-reliability installations where uninterrupted performance is critical. Their precision and focused functionality make them a preferred choice for sectors that demand robust fault detection without the interference of ancillary processes.

The medium voltage category, typically covering systems between 1kV and 36kV, is forecast to expand at a CAGR exceeding 5.8% through 2034. This growth is driven by heightened demand for fault monitoring within distribution networks, industrial operations, and facilities integrating renewable energy. Utilities are actively upgrading legacy grid infrastructure by embedding digital monitoring tools that improve fault location accuracy and reduce service interruptions. As a result, DFRs are becoming key components in medium-voltage network modernization projects, where their ability to support local diagnostics and telemetry enhances system reliability.

Within the United States, the digital fault recorder market continues to show steady progress. It reached USD 103.5 million in 2022, climbed to USD 108.1 million in 2023, and rose again to USD 113.1 million in 2024. The growing investment in aging infrastructure upgrades, along with increased grid vulnerability to extreme weather events and fluctuating energy demands, is encouraging utilities to adopt more sophisticated fault analysis solutions. The focus is on ensuring operational continuity and protecting the grid from both predictable and unexpected disruptions.

Industry leaders maintain a competitive edge through extensive global operations and well-established research and development capabilities. Companies holding more than 20% of the market share collectively operate manufacturing facilities in key regions including North America, Europe, and Asia. Their global presence allows for cost-effective production and quick product delivery. With long-standing reputations for innovation and reliability, these firms are positioned to influence the trajectory of the digital fault recorder industry as it moves deeper into the digital age.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Dedicated

- 5.3 Multifunctional

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Medium voltage

- 6.3 High voltage

- 6.4 Extra high voltage

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 High speed disturbance

- 7.3 Low speed disturbance

- 7.4 Steady state

Chapter 8 Market Size and Forecast, By Installation, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Generation

- 8.3 Transmission

- 8.4 Distribution

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Russia

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Turkey

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Ametek

- 10.3 Ducati Energia

- 10.4 Eaton

- 10.5 Elspec

- 10.6 E-Max Instruments

- 10.7 Erlphase

- 10.8 General Electric

- 10.9 Hitachi

- 10.10 Kinkei

- 10.11 Kocos

- 10.12 Logiclab

- 10.13 Mehta Tech

- 10.14 Qualitrol

- 10.15 Schneider Electric

- 10.16 Siemens

2026年全球分散式數位故障記錄系統市場報告2026年全球數位故障記錄系統市場報告

2026年全球分散式數位故障記錄系統市場報告2026年全球數位故障記錄系統市場報告 數位故障記錄器市場:2026-2032年全球市場預測(按產品類型、安裝配置、通訊協定、監控類型、應用和最終用戶分類)

數位故障記錄器市場:2026-2032年全球市場預測(按產品類型、安裝配置、通訊協定、監控類型、應用和最終用戶分類) 全球數位故障記錄器(DFR)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球數位故障記錄器(DFR)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 專用數位故障記錄器市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、電壓、最終用途產業、地區和競爭細分,2020-2030 年)數位故障記錄器市場-全球產業規模、佔有率、趨勢、機會和預測(按應用程式、類型、最終用戶、技術、地區和競爭細分,2020-2030 年)輸電線路故障監測設備市場按故障類型、組件、部署、應用和最終用戶分類 - 2025-2030 年全球預測

專用數位故障記錄器市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、電壓、最終用途產業、地區和競爭細分,2020-2030 年)數位故障記錄器市場-全球產業規模、佔有率、趨勢、機會和預測(按應用程式、類型、最終用戶、技術、地區和競爭細分,2020-2030 年)輸電線路故障監測設備市場按故障類型、組件、部署、應用和最終用戶分類 - 2025-2030 年全球預測 輸配電故障檢測市場,按組件、按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

輸配電故障檢測市場,按組件、按應用、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 數位故障記錄器市場規模、佔有率、趨勢分析報告:按組件、按技術、按安裝位置、按地區、細分市場預測,2024-2030 年

數位故障記錄器市場規模、佔有率、趨勢分析報告:按組件、按技術、按安裝位置、按地區、細分市場預測,2024-2030 年