|

市場調查報告書

商品編碼

1740896

客艙管理系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cabin Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

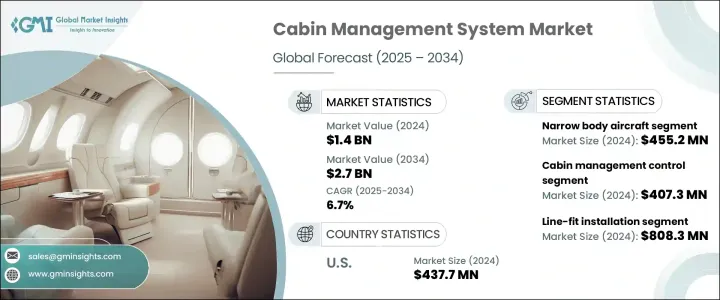

2024 年全球客艙管理系統市場規模為 14 億美元,預計到 2034 年將以 6.7% 的複合年成長率成長至 27 億美元。市場成長主要源自於對提升乘客舒適度的日益重視,以及高階飛機隊的擴張。隨著全球航空旅行持續復甦和擴張,航空公司更加重視提供優質的飛行體驗,這推動了對先進 CMS 技術的需求。這些系統能夠無縫控制各種客艙功能,包括照明、溫度、娛樂和通訊介面,從而顯著提高乘客滿意度和品牌忠誠度。增強型 CMS 解決方案也不斷發展,以支援無線技術、即時自適應和智慧自動化,從而實現更智慧、更個人化的客艙設定。

近年來,全球貿易政策的變化對CMS市場產生了影響。某些國家對進口產品實施的關稅規定提高了依賴外國零件的製造商的生產成本。這些成本上漲反過來又導致CMS產品價格上漲,對供應商和航空公司買家都產生了影響。這種情況促使許多製造商重新評估其供應鏈策略,其中一些製造商選擇在國內生產或從其他地區採購替代品。雖然這種變化支持了本地製造業生態系統,但也導致了CMS定價和全球產品供應的廣泛轉變。航空公司,尤其是那些注重成本管理的航空公司,由於CMS安裝和升級成本的增加,面臨營運成本的上升。然而,這些發展正在逐步為該行業建立更具彈性和本地化的供應結構。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 27億美元 |

| 複合年成長率 | 6.7% |

隨著全球航空旅客數量的成長以及航空業競爭壓力的加劇,對創新 CMS 解決方案的需求持續激增。航空公司正擴大採用智慧且直覺的技術,以滿足日益成長的消費者期望。 CMS 平台現已整合物聯網 (IoT) 感測器、基於應用程式的控制系統、語音辨識工具以及基於人工智慧的客製化功能,旨在提供無縫的機上體驗。這些增強功能支援航空公司提供一致的優質服務,同時滿足能源效率、噪音控制和系統可靠性方面的現代監管標準。

就飛機類型而言,窄體飛機市場領先,2024 年估值達 4.552 億美元。這類飛機在注重成本的短程航線運作中日益普及,推動了對輕型、高效且經濟實惠的 CMS 系統的需求。新興市場國內航空旅行的日益成長也加劇了對先進且經濟高效的 CMS 系統的需求,這些系統能夠在不增加飛機重量或營運成本的情況下,提供更佳的乘客控制。

按組件分類,客艙管理控制器在2024年佔據最大佔有率,市場規模達4.073億美元。隨著智慧感測器和自動化客艙技術的興起,對能夠管理多種客艙功能的集中控制單元的需求激增。航空公司和製造商優先考慮模組化、緊湊型、低功耗且易於升級或更換的控制器,以減少停機時間和維護工作。

按安裝類型分類,線裝系統市場在2024年以8.083億美元的價值成為市場領導者。隨著新飛機交付數量的增加,人們對原廠安裝的CMS系統的偏好也日益成長。高階飛機的買家尤其青睞支援先進多媒體功能、動態照明和智慧控制功能的全整合系統,從而在生產初期就打造出高階的客艙環境。

從地區來看,美國在CMS市場佔據主導地位,2024年的估值為4.377億美元。美國對豪華CMS升級和先進連接選項的強勁需求,尤其是在私人和商務航空領域,持續推動市場成長。此外,主要原始設備製造商和維修供應商的參與也為改裝和新安裝活動提供了支持,鞏固了美國作為關鍵市場的地位。

客艙管理系統市場仍高度分散,既有成熟的全球企業,也有創新新創公司。前三名的公司合計佔據超過29.7%的市場佔有率,主要專注於下一代解決方案。這些進步反映了從孤立的硬體系統向全面整合的數位客艙生態系統的廣泛轉變。該行業正快速轉向智慧模組化架構,以提供更佳的個人化和營運效率,這反映了航空平台向更電動化和互聯化發展的大趨勢。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 關鍵零件價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 乘客對飛行舒適度的需求不斷成長

- 擴大公務機和貴賓飛機隊

- 長途航班的成長

- 飛機產量增加

- 與智慧型設備整合

- 產業陷阱與挑戰

- 安裝和維護成本高

- 系統相容性問題

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按飛機類型,2021 - 2034 年

- 主要趨勢

- 窄體飛機

- 寬體飛機

- 支線噴射機

- 公務機

第6章:市場估計與預測:按組成部分,2021 - 2034 年

- 主要趨勢

- 客艙管理控制器

- 控制顯示和使用者介面

- 音訊/視訊介面模組

- 客艙管理軟體

- 連接模組

- 其他

第7章:市場估計與預測:按安裝類型,2021 - 2034 年

- 主要趨勢

- 線路安裝

- 改造安裝

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Alto Aviation

- Astronics

- BAE Systems

- Bombardier

- Collins

- Diehl Aviation

- Gogo Business Aviation

- Heads Up Technologies

- Honeywell

- KID Systeme

- Lufthansa Technik

- Rosen Aviation

- Safran Cabin

- Satcom Direct

- STG Aerospace

- Thales

The Global Cabin Management System Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 2.7 billion by 2034. This market's growth is primarily driven by a rising emphasis on enhancing passenger comfort, combined with the expansion of high-end aircraft fleets. As air travel continues to recover and expand globally, airline operators are placing a greater focus on offering a premium in-flight experience, which is fueling the need for advanced CMS technologies. These systems enable seamless control over various cabin features, including lighting, temperature, entertainment, and communication interfaces, all of which significantly improve passenger satisfaction and brand loyalty. Enhanced CMS solutions are also evolving to support wireless technology, real-time adaptability, and intelligent automation, allowing smarter and more personalized cabin settings.

In recent years, shifting global trade policies have impacted the CMS market. Tariff regulations imposed on imports from certain countries raised production costs for manufacturers relying on foreign components. These cost hikes, in turn, led to increased prices of CMS products, affecting both suppliers and airline buyers. This situation encouraged many manufacturers to reevaluate their supply chain strategies, with several opting for domestic production or sourcing alternatives from other regions. Although this change supported local manufacturing ecosystems, it also contributed to a broader shift in CMS pricing and global product availability. Airlines, particularly those focused on cost management, have faced increased operational costs due to the higher expense of CMS installations and upgrades. Nevertheless, these developments are gradually fostering a more resilient and localized supply structure for the industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 6.7% |

With rising global air passenger numbers and competitive pressures in the aviation sector, the demand for innovative CMS solutions continues to surge. Airlines are increasingly adopting smart and intuitive technologies that align with growing consumer expectations. CMS platforms now feature integrations with Internet of Things (IoT) sensors, app-based control systems, voice recognition tools, and AI-based customization, all designed to deliver a seamless onboard experience. These enhancements support airlines in delivering consistent, premium service while meeting modern regulatory standards in terms of energy efficiency, noise control, and system reliability.

In terms of aircraft types, the narrow-body aircraft segment led the market with a valuation of USD 455.2 million in 2024. The popularity of these aircraft in cost-conscious and short-haul operations is propelling the need for lightweight, efficient, and affordable CMS installations. Growing domestic air travel in emerging markets has also intensified demand for advanced yet cost-effective CMS setups that offer enhanced passenger control without increasing aircraft weight or operational expense.

By component, cabin management controllers accounted for the largest share in 2024, generating USD 407.3 million. The demand for centralized control units capable of managing multiple cabin functionalities has surged, particularly with the rise in smart sensors and automated cabin technologies. Airlines and manufacturers are prioritizing modular, compact, and low-power controllers that can be easily upgraded or replaced, helping reduce downtime and maintenance efforts.

Based on installation type, the line-fit segment emerged as the market leader with a value of USD 808.3 million in 2024. The increasing number of new aircraft deliveries has led to a growing preference for factory-installed CMS setups. Buyers of premium aircraft are especially keen on fully integrated systems that support advanced multimedia functions, dynamic lighting, and smart control capabilities, delivering a high-end cabin environment straight from production.

Regionally, the United States dominated the CMS market with a valuation of USD 437.7 million in 2024. The country's strong demand for luxurious CMS upgrades and advanced connectivity options, particularly in private and business aviation, continues to drive market growth. In addition, the presence of major OEMs and maintenance providers supports both retrofit and new installation activities, reinforcing the U.S.'s position as a key market.

The cabin management system landscape remains highly fragmented, with a mix of established global players and innovative startups. The top three companies collectively control over 29.7% of the market, focusing heavily on next-generation solutions. These advancements reflect a wider transition from isolated hardware systems to fully integrated digital cabin ecosystems. The industry is rapidly moving toward intelligent, modular architectures that offer enhanced personalization and operational efficiency, reflecting the broader trend toward more electric and connected aviation platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for in-flight passenger comfort

- 3.3.1.2 Expansion of business jet and vip aircraft fleets

- 3.3.1.3 Growth in long-haul flights

- 3.3.1.4 Increase in aircraft production

- 3.3.1.5 Integration with smart devices

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High installation and maintenance costs

- 3.3.2.2 System compatibility issues

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Narrow-body aircraft

- 5.3 Wide-body aircraft

- 5.4 Regional jets

- 5.5 Business jets

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Cabin management controllers

- 6.3 Control displays and user interfaces

- 6.4 Audio/video interface modules

- 6.5 Cabin management software

- 6.6 Connectivity modules

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Installation Type, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Line-fit installation

- 7.3 Retrofit installation

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alto Aviation

- 9.2 Astronics

- 9.3 BAE Systems

- 9.4 Bombardier

- 9.5 Collins

- 9.6 Diehl Aviation

- 9.7 Gogo Business Aviation

- 9.8 Heads Up Technologies

- 9.9 Honeywell

- 9.10 KID Systeme

- 9.11 Lufthansa Technik

- 9.12 Rosen Aviation

- 9.13 Safran Cabin

- 9.14 Satcom Direct

- 9.15 STG Aerospace

- 9.16 Thales

民航機空氣管理系統市場:依產品類型、飛機類型、最終用戶和通路分類-2026-2032年全球市場預測

民航機空氣管理系統市場:依產品類型、飛機類型、最終用戶和通路分類-2026-2032年全球市場預測 2026年低空經濟型空氣管理系統全球市場報告2026年全球空氣管理系統市場報告空氣管理系統市場:依產品類型、安裝類型和通路分類-2026年至2032年全球預測

2026年低空經濟型空氣管理系統全球市場報告2026年全球空氣管理系統市場報告空氣管理系統市場:依產品類型、安裝類型和通路分類-2026年至2032年全球預測 空氣管理系統市場-全球產業規模、佔有率、趨勢、機會、預測:按系統、平台、地區和競爭對手分類,2021-2031年飛機空氣管理系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按系統類型、飛機類型、地區和競爭格局分類,2021-2031年)按平台類型、系統類型、分銷管道和最終用戶分類的客艙空氣系統市場 - 全球預測 2026-2032

空氣管理系統市場-全球產業規模、佔有率、趨勢、機會、預測:按系統、平台、地區和競爭對手分類,2021-2031年飛機空氣管理系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按系統類型、飛機類型、地區和競爭格局分類,2021-2031年)按平台類型、系統類型、分銷管道和最終用戶分類的客艙空氣系統市場 - 全球預測 2026-2032 飛機空氣管理系統市場規模、佔有率和成長分析(按系統、平台、飛機類型和地區分類)-2026-2033年產業預測全球客艙管理系統市場(按組件、連接性、部署類型、安裝和最終用戶分類)- 2025 年至 2030 年預測

飛機空氣管理系統市場規模、佔有率和成長分析(按系統、平台、飛機類型和地區分類)-2026-2033年產業預測全球客艙管理系統市場(按組件、連接性、部署類型、安裝和最終用戶分類)- 2025 年至 2030 年預測