|

市場調查報告書

商品編碼

1740889

低密度聚乙烯包裝(LDPE)市場機會、成長動力、產業趨勢分析及2025-2034年預測Low-density Polyethylene Packaging (LDPE) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

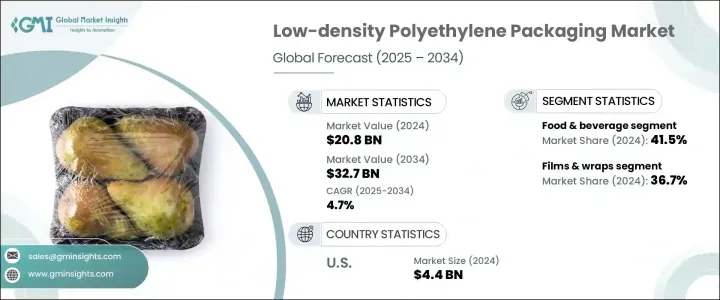

2024年,全球低密度聚乙烯包裝市場規模達208億美元,預計到2034年將以4.7%的複合年成長率成長,達到327億美元,這主要得益於食品、製藥和個人護理行業強勁的需求。這一成長反映了低密度聚乙烯包裝在消費品和工業領域的應用日益廣泛。隨著全球包裝產業的快速發展,低密度聚乙烯憑藉其柔韌性、耐用性、低生產成本和高防潮性,仍然是市場首選材料。由於企業和消費者都高度重視產品安全和保存期限,因此低密度聚乙烯包裝在確保各個供應鏈中產品完整性方面發揮關鍵作用。

電子商務和數位購物平台的興起也刺激了對軟包裝材料的需求,這些材料能夠承受運輸和搬運的壓力,同時保持產品的完好無損。此外,輕盈、節省空間的包裝有助於降低運輸成本,這使得低密度聚乙烯 (LDPE) 成為製造商的首選材料。食品安全和包裝衛生監管力道的不斷加大,進一步提升了市場潛力。在持續推動永續發展的背景下,製造商目前正在致力於生產可回收、環保的低密度聚乙烯 (LDPE) 包裝解決方案,這些解決方案正受到注重環保的消費者和監管機構的青睞。旨在提升營運效率和品牌吸引力的包裝形式和材料創新,正在塑造全球眾多包裝公司的策略方向。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 208億美元 |

| 預測值 | 327億美元 |

| 複合年成長率 | 4.7% |

低密度聚乙烯 (LDPE) 因其防潮性和柔韌性而被廣泛應用於食品和飲料行業,是包裝易腐產品的理想選擇。隨著生活方式的改變和城市化進程的推進,人們對簡便食品的需求不斷成長,這顯著推動了低密度聚乙烯包裝的使用。消費者越來越傾向於即食食品和單人份食品,尤其是在發展中經濟體,這些國家依賴低密度聚乙烯薄膜和容器來維持食品的新鮮度和安全性。低密度聚乙烯 (LDPE) 憑藉其衛生特性,可延長食品的保存期限,符合現代消費習慣和分銷模式。

在醫藥和個人護理領域,由於人們日益增強的醫療意識、全球人口老化以及個人健康支出的增加,低密度聚乙烯 (LDPE) 包裝持續受到青睞。尤其是在後疫情時代,人們對衛生和污染預防的重視程度不斷提高,這加速了一次性和防篡改包裝形式的轉變。低密度聚乙烯 (LDPE) 具有成本效益高且易於加工的特點,在幫助製造商滿足嚴格的安全和包裝標準方面發揮核心作用。從藥膏管和藥袋到個人護理小袋,LDPE 正在多個產品類別中證明其多功能性和有效性。

然而,市場面臨貿易相關干擾帶來的不利因素。川普政府對鋼鐵、鋁和中國零件徵收關稅,對整個包裝供應鏈產生了連鎖反應。這些政策導致低密度聚乙烯 (LDPE) 樹脂和成品包裝材料的成本上漲,對生產成本造成上行壓力,最終推高了消費者價格。與墨西哥和加拿大等主要合作夥伴的貿易緊張局勢也限制了原料的流動,對關鍵零件的供應構成挑戰,並增加了製造商的物流複雜性。

從產品細分來看,薄膜和包裝材料類別在2024年的市佔率為36.7%。這些產品因其適應性和防潮性能,廣泛應用於食品包裝、工業包裝和電商運輸。其價格實惠、使用方便,使其成為尋求最佳化包裝成本並確保產品安全的企業的首選。隨著各行各業對保護性包裝的需求不斷成長,這個細分市場也持續蓬勃發展。

2024年,食品飲料產業成為主導的終端應用領域,佔41.5%的市場。低密度聚乙烯(LDPE)包裝被廣泛用於保鮮和衛生,是冷凍食品、零食、乳製品和加工食品不可或缺的材料。隨著消費者擁抱快節奏、便利的生活方式,對低密度聚乙烯(LDPE)等軟性耐用包裝的依賴預計只會成長,尤其是在包裝食品消費量激增的新興市場。

2024年,美國低密度聚乙烯 (LDPE) 包裝市場規模達44億美元。該市場的成長主要得益於食品、製藥和電商產業的持續需求。加工技術的進步以及對安全、衛生和法規合規性的日益重視,正在推動創新。同時,人們對永續包裝的興趣日益濃厚,也促使製造商投資再生LDPE解決方案。這些努力使企業能夠滿足客戶期望,同時與全球永續發展目標保持一致。

全球低密度聚乙烯 (LDPE) 包裝市場的主要參與者包括康斯坦莎軟性包裝 (Constantia flexibles)、貝裡環球公司 (Berry Global Inc.)、希悅爾 (Sealed Air) 和安姆科公司 (Amcor plc)。這些公司正在利用技術升級和永續實踐來保持競爭力。關鍵策略包括擴大產品線、提高供應鏈彈性以及增強低密度聚乙烯產品的可回收性,以應對環境問題和不斷變化的監管框架。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 主要原物料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 衝擊力

- 成長動力

- 包裝食品和飲料行業的成長

- 藥品和個人護理需求不斷成長

- 電子商務和零售分銷的擴張

- 在工業和農業應用中的採用率不斷提高

- 輕量化和材料效率

- 產業陷阱與挑戰

- 環境問題和監管壓力

- 回收率低,循環性有限

- 成長動力

- 成長潛力分析

- 科技與創新格局

- 專利分析

- 重要新聞和舉措

- 未來市場趨勢

- 波特的分析

- PESTEL分析

- 監管格局

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按包裝類型,2021 - 2034 年

- 主要趨勢

- 包包和小袋

- 瓶子和容器

- 薄膜和包裝

- 管

- 其他

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 食品和飲料

- 個人護理和化妝品

- 電氣和電子產品

- 消費品

- 製藥

- 電子商務

- 其他

第7章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Amcor plc

- BENZ Packaging

- Berry Global Inc.

- Constantia Flexibles

- EPL Limited

- FKuR

- Inteplast Group

- Origin Pharma Packaging

- RKW Group

- SABIC

- Sealed Air

- Silgan Holdings

- Sirane Group

- Sonoco Products Company

- Strobel GmbH

- TC Transcontinental

- Thermo Fisher Scientific Inc.

- Westlake Corporation

The Global Low-Density Polyethylene Packaging Market was valued at USD 20.8 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 32.7 billion by 2034, driven by robust demand across food, pharmaceutical, and personal care industries. This growth reflects the expanding applications of LDPE packaging in both consumer and industrial sectors. With the global packaging industry rapidly evolving, LDPE remains a preferred material due to its flexibility, durability, low production cost, and high resistance to moisture. As businesses and consumers alike prioritize product safety and shelf-life, LDPE packaging plays a key role in ensuring product integrity across various supply chains.

The rising trend of e-commerce and digital shopping platforms also fuels the demand for flexible packaging materials that can withstand shipping and handling stress while keeping products intact. In addition, the shift toward lightweight, space-saving packaging that helps reduce transportation costs is making LDPE a go-to material for manufacturers. Growing regulatory focus on food safety and packaging hygiene is further enhancing the market potential. Amid ongoing efforts toward sustainability, manufacturers are now working on producing recyclable and eco-friendly LDPE packaging solutions, which are gaining traction among environmentally conscious consumers and regulators. Innovation in packaging formats and materials, aimed at boosting operational efficiency and brand appeal, is shaping the strategic direction of many packaging firms globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.8 billion |

| Forecast Value | $32.7 billion |

| CAGR | 4.7% |

LDPE is widely used in the food and beverage sector due to its moisture resistance and flexibility, making it ideal for packaging perishable products. The increasing demand for convenience food, driven by changing lifestyles and urbanization, is significantly boosting the use of LDPE-based packaging. Consumers are leaning heavily toward ready-to-eat meals and single-serve food products, especially in developing economies, which rely on LDPE films and containers to maintain freshness and safety. With its hygienic attributes, LDPE ensures an extended shelf life for food items, aligning with modern consumption habits and distribution models.

In the pharmaceutical and personal care segments, LDPE packaging continues to gain traction due to rising healthcare awareness, an aging global population, and higher spending on personal wellness. The heightened focus on hygiene and contamination prevention, particularly in the post-pandemic landscape, is accelerating the shift toward single-use and tamper-proof packaging formats. LDPE, being cost-effective and easy to process, is playing a central role in helping manufacturers meet stringent safety and packaging standards. From ointment tubes and medicine pouches to personal care sachets, LDPE is proving its versatility and effectiveness across multiple product categories.

However, the market has faced headwinds in the form of trade-related disruptions. Tariffs on steel, aluminum, and Chinese components introduced during the Trump administration caused a ripple effect throughout the packaging supply chain. These policies led to increased costs for LDPE resins and finished packaging materials, putting upward pressure on production expenses and ultimately raising consumer prices. Trade tensions with key partners like Mexico and Canada also restricted raw material flow, challenging the availability of essential components and adding to logistical complexity for manufacturers.

In terms of product segmentation, the films and wraps category accounted for a 36.7% market share in 2024. These products are widely used in food packaging, industrial wrapping, and e-commerce shipping due to their adaptability and moisture barrier properties. Their affordability and ease of use make them a preferred choice for businesses looking to optimize packaging costs while ensuring product safety. As the need for protective packaging grows across sectors, this segment continues to thrive.

The food and beverage industry emerged as the dominant end-use segment in 2024, holding a 41.5% market share. LDPE packaging is extensively used to safeguard freshness and hygiene, making it indispensable for frozen foods, snacks, dairy, and processed meals. As consumers embrace fast-paced, on-the-go lifestyles, the reliance on flexible and durable packaging like LDPE is only expected to grow, especially in emerging markets where packaged food consumption is surging.

The United States Low-Density Polyethylene (LDPE) Packaging Market was valued at USD 4.4 billion in 2024. Growth here is primarily driven by consistent demand from the food, pharmaceutical, and e-commerce sectors. Technological advancements in processing and the rising focus on safety, hygiene, and regulatory compliance are driving innovation. At the same time, increased interest in sustainable packaging is pushing manufacturers to invest in recycled LDPE solutions. These efforts are enabling businesses to meet customer expectations while aligning with global sustainability goals.

Major players in the global LDPE packaging market include Constantia Flexibles, Berry Global Inc., Sealed Air, and Amcor plc. These companies are leveraging technological upgrades and sustainable practices to stay competitive. Key strategies involve expanding product lines, improving supply chain resilience, and enhancing the recyclability of LDPE products to address environmental concerns and evolving regulatory frameworks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key raw material

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 key companies impacted

- 3.2.4 strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth in packaged food & beverage sector

- 3.3.1.2 Rising demand in pharmaceuticals & personal care

- 3.3.1.3 Expansion of e-commerce & retail distribution

- 3.3.1.4 Increased adoption in industrial and agricultural applications

- 3.3.1.5 Lightweighting and material efficiency

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Environmental concerns and regulatory pressure

- 3.3.2.2 Low recycling rate and limited circularity

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Technological & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Regulatory landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Packaging Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Bags & pouches

- 5.3 Bottles & containers

- 5.4 Films & wraps

- 5.5 Tubes

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Food and beverages

- 6.3 Personal care & cosmetics

- 6.4 Electricals & electronics

- 6.5 Consumer goods

- 6.6 Pharmaceuticals

- 6.7 E-commerce

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Amcor plc

- 8.2 BENZ Packaging

- 8.3 Berry Global Inc.

- 8.4 Constantia Flexibles

- 8.5 EPL Limited

- 8.6 FKuR

- 8.7 Inteplast Group

- 8.8 Origin Pharma Packaging

- 8.9 RKW Group

- 8.10 SABIC

- 8.11 Sealed Air

- 8.12 Silgan Holdings

- 8.13 Sirane Group

- 8.14 Sonoco Products Company

- 8.15 Strobel GmbH

- 8.16 TC Transcontinental

- 8.17 Thermo Fisher Scientific Inc.

- 8.18 Westlake Corporation

低密度聚乙烯市場分析及預測(至2035年):類型、產品、應用、技術、形式、最終用戶、材料類型、製程、功能與組件

低密度聚乙烯市場分析及預測(至2035年):類型、產品、應用、技術、形式、最終用戶、材料類型、製程、功能與組件 2026年全球低密度聚乙烯市場報告

2026年全球低密度聚乙烯市場報告 低密度聚乙烯(LDPE)市場,全球市場,2025-2029年

低密度聚乙烯(LDPE)市場,全球市場,2025-2029年 生質能聚乙烯低密度聚乙烯市場按等級、原料、產品形式、應用和分銷管道分類,全球預測,2026-2032年

生質能聚乙烯低密度聚乙烯市場按等級、原料、產品形式、應用和分銷管道分類,全球預測,2026-2032年 低密度聚乙烯:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

低密度聚乙烯:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 全球低密度聚乙烯市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)擠壓低密度聚乙烯(LDPE)市場:未來預測(2025-2030)

全球低密度聚乙烯市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)擠壓低密度聚乙烯(LDPE)市場:未來預測(2025-2030) 線型低密度聚乙烯(LLDPE)的全球市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2018年~2032年線型低密度聚乙烯(LLDPE)的印度市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2019年~2033年

線型低密度聚乙烯(LLDPE)的全球市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2018年~2032年線型低密度聚乙烯(LLDPE)的印度市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2019年~2033年 低密度聚乙烯市場(按技術、應用和地區分類)

低密度聚乙烯市場(按技術、應用和地區分類)