|

市場調查報告書

商品編碼

1740885

電氣線路互連系統 (EWIS) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Electrical Wiring Interconnection System (EWIS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

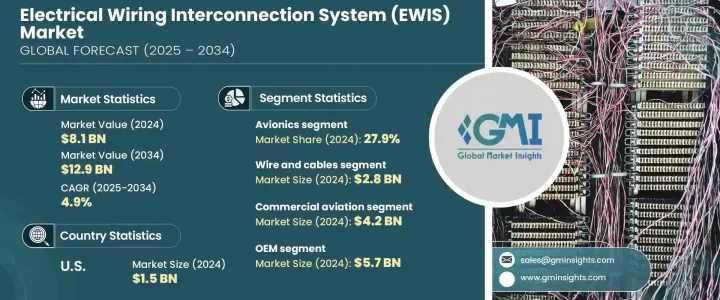

2024 年全球電氣線路互連系統市場價值為 81 億美元,預計到 2034 年將以 4.9% 的複合年成長率成長,達到 129 億美元,這主要得益於向全電動和多電動飛機的快速轉型,這一轉型在推動這一成長方面發揮了核心作用。航空業對整合電力系統的需求不斷成長,加上機上娛樂和即時連接系統的使用日益增多,正在重塑線路基礎設施。城市空中交通 (UAM) 平台和電動垂直起降 (eVTOL) 飛機的出現正在加速整個 EWIS 領域的創新。這些飛機需要能夠處理複雜電氣和資料傳輸任務的輕型高性能線路。人們對永續航空和增強電氣化的興趣日益濃厚,越來越依賴能夠與不斷發展的飛行技術無縫整合的先進線路系統。

然而,由於鋁、銅和鋼的關稅導致材料成本上升,該行業面臨壓力。這些金屬對於生產EWIS組件(包括連接器、電纜和外殼)至關重要。因此,製造商和最終用戶的生產成本正在上升。此外,對從中國進口的電子產品和半導體徵收的關稅正在阻礙供應鏈,並影響下一代EWIS組件的開發,尤其是用於數位系統和自動化飛機平台的組件。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 81億美元 |

| 預測值 | 129億美元 |

| 複合年成長率 | 4.9% |

電線電纜產業在2024年創造了28億美元的收入,這主要得益於對耐熱性、訊號保真度和輕量化設計的先進材料的需求。隨著現代飛機擴大採用數位和電氣技術,對高性能佈線系統(包括光纖和配電解決方案)的需求也日益成長。絕緣和屏蔽技術的創新使飛機的運作更加安全高效,同時有助於減輕飛機的整體重量。

在應用方面,航空電子設備領域在2024年佔了27.9%的佔有率。隨著駕駛艙控制、通訊系統和飛行資料處理的數位轉型,對可靠緊湊的EWIS的需求正在顯著成長。精確的航線規劃、電磁干擾屏蔽以及與數位儀錶板的整合如今已成為標配,尤其是在軍用和商用機隊中。這些系統確保了先進飛機子系統內持續的電力傳輸和資料連接。

由於美國航太和國防領域的蓬勃發展,美國電氣線路互連系統 (EWIS) 市場在 2024 年實現了 15 億美元的產值。美國對電動飛機的重視、城市空中交通項目的推進以及國防預算的不斷成長,為先進的 EWIS 部署提供了支持。自動化和模組化佈線系統的投資,以及強大的OEM)和供應商網路,持續推動美國市場對 EWIS 的需求。

泰科電子 (TE Connectivity)、柯林斯航太)、霍尼韋爾國際公司 (Honeywell International Inc.)、安費諾公司 (Amphenol Corporation) 和賽峰集團 (Safran) 等領先企業正在採取擴張研發設施、投資輕量化材料創新以及增強模組化設計能力等策略。許多公司正在與飛機製造商和國防機構建立戰略合作夥伴關係,共同開發下一代解決方案。這些公司專注於數位整合、智慧診斷和可擴展佈線系統,以支援快速飛機組裝和長期運行可靠性。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 商用和國防領域飛機交付量激增

- 輕型和省油飛機的需求成長

- 向多電動和全電動飛機轉變的趨勢日益明顯(MEA/AESA)

- 機上娛樂 (IFE) 和連接系統日益普及

- 城市空中交通 (UAM) 和 eVTOL 飛機的出現

- 產業陷阱與挑戰

- 開發和製造成本高

- 嚴格的監管合規和認證延遲

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 電線電纜(每英尺)

- 連接器

- 電氣接地和連接裝置

- 電氣接頭

- 夾具

- 壓力密封

- 其他

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 航空電子設備

- 駕駛艙控制裝置

- 飛行控制系統(FCS)

- 飛行管理系統(FMS)

- 其他

- 內飾

- 機上娛樂 (IFE)

- 廚房

- 座椅電源

- 客艙管理

- 推進系統

- 引擎

- 輔助動力裝置(APU)

- 其他

- 機體

- 翅膀

- 尾巴

- 其他

第7章:市場估計與預測:依航空類型,2021 - 2034 年

- 主要趨勢

- 商業航空

- 窄體飛機(NBA)

- 寬體飛機(WBA)

- 超大型飛機(VLA)

- 區域運輸飛機(RTA)

- 軍事航空

- 戰鬥機

- 運輸飛機

- 軍用直升機

- 商務及通用航空

- 公務機

- 直升機

- 活塞式飛機

- 渦輪螺旋槳飛機

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Amphenol Corporation

- Boeing

- Collins Aerospace (Raytheon Technologies)

- Co-Operative Industries Aerospace & Defense (kSARIA)

- Ducommun

- EIS Electronics GmbH

- Elektro Metall Export

- Honeywell International Inc.

- InterConnect Wiring

- JST Sales America

- kSARIA Corporation

- Leonardo

- Molex

- PEI-Genesis

- Pic Wire & Cable (Angelus Corporation)

- Safran

- TE Connectivity

- WL Gore & Associates

The Global Electrical Wiring Interconnection System Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 12.9 billion by 2034, driven by the rapid transition toward all-electric and more-electric aircraft playing a central role in driving this growth. Increased demand for integrated electric systems in aviation, combined with the rising use of in-flight entertainment and real-time connectivity systems, is reshaping wiring infrastructure. The emergence of Urban Air Mobility (UAM) platforms and electric vertical takeoff and landing (eVTOL) aircraft are accelerating innovation across the EWIS landscape. These aircraft require lightweight, high-performance wiring capable of handling complex electrical and data transmission tasks. Rising interest in sustainable aviation and enhanced electrification is increasing dependency on advanced wiring systems that integrate seamlessly with evolving flight technologies.

However, the industry faces pressure due to elevated material costs from tariffs on aluminum, copper, and steel. These metals are critical to producing EWIS components, including connectors, cables, and enclosures. As a result, manufacturers and end-users are experiencing increased production costs. In addition, tariffs on electronic and semiconductor imports from China are hampering supply chains and affecting the development of next-gen EWIS components, particularly those used in digital systems and automated aircraft platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 4.9% |

The wire and cables segment generated USD 2.8 billion in 2024, largely due to demand for advanced materials that offer thermal resistance, signal fidelity, and lightweight designs. As modern aircraft increasingly incorporate digital and electric technologies, there's a heightened requirement for high-performance wiring systems, including fiber optics and power distribution solutions. Innovations in insulation and shielding technologies enable safer and more efficient operations while helping reduce overall aircraft weight.

In terms of application, the avionics segment held a 27.9% share in 2024. With the digital transformation of cockpit controls, communication systems, and flight data processing, the demand for reliable and compact EWIS is growing significantly. Precision routing, electromagnetic interference shielding, and integration with digital dashboards are now standard, especially in military and commercial fleets. These systems ensure consistent power flow and data connectivity within advanced aircraft subsystems.

U.S. Electrical Wiring Interconnection System (EWIS) Market generated USD 1.5 billion in 2024 due to its expanding aerospace and defense sectors. The country's focus on more electric aircraft, increasing urban air mobility projects, and rising defense budgets support advanced EWIS deployment. Investments in automation and modular wiring systems, along with strong OEM and supplier networks, continue to fuel national demand.

Leading players such as TE Connectivity, Collins Aerospace, Honeywell International Inc., Amphenol Corporation, and Safran are adopting strategies like expanding RandD facilities, investing in lightweight material innovation, and enhancing modular design capabilities. Many are forming strategic partnerships with aircraft manufacturers and defense agencies to co-develop next-gen solutions. Companies focus on digital integration, smart diagnostics, and scalable wiring systems that support rapid aircraft assembly and long-term operational reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in aircraft deliveries across commercial and defense segments

- 3.7.1.2 Growth in demand for lightweight and fuel-efficient aircraft

- 3.7.1.3 Rise in shift toward more-electric and all-electric aircraft (MEA/AESA)

- 3.7.1.4 Increasing proliferation of in-flight entertainment (IFE) and connectivity systems

- 3.7.1.5 Emergence of Urban Air Mobility (UAM) and eVTOL Aircraft

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High development and manufacturing costs

- 3.7.2.2 Stringent regulatory compliance and certification delays

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million, Foot & Units)

- 5.1 Key trends

- 5.2 Wire and cables (per foot)

- 5.3 Connectors

- 5.4 Electrical grounding and bonding devices

- 5.5 Electrical splices

- 5.6 Clamps

- 5.7 Pressure seals

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Avionics

- 6.2.1 Cockpit controls

- 6.2.2 Flight control systems (FCS)

- 6.2.3 Flight management systems (FMS)

- 6.2.4 Others

- 6.3 Interiors

- 6.3.1 Inflight entertainment (IFE)

- 6.3.2 Galleys

- 6.3.3 In-seat power

- 6.3.4 Cabin management

- 6.4 Propulsion system

- 6.4.1 Engine

- 6.4.2 Auxiallry power unit (APU)

- 6.4.3 Other

- 6.5 Airframe

- 6.5.1 Wings

- 6.5.2 Tail

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Aviation Type, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Commercial aviation

- 7.2.1 Narrow body aircraft (NBA)

- 7.2.2 Wide body aircraft (WBA)

- 7.2.3 Very large aircraft (VLA)

- 7.2.4 Regional transport aircraft (RTA)

- 7.3 Military aviation

- 7.3.1 Fighter jets

- 7.3.2 Transport aircraft

- 7.3.3 Military helicopters

- 7.4 Business and general aviation

- 7.4.1 Business jets

- 7.4.2 Helicopters

- 7.4.3 Piston aircraft

- 7.4.4 Turboprop aircraft

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amphenol Corporation

- 10.2 Boeing

- 10.3 Collins Aerospace (Raytheon Technologies)

- 10.4 Co-Operative Industries Aerospace & Defense (kSARIA)

- 10.5 Ducommun

- 10.6 E.I.S. Electronics GmbH

- 10.7 Elektro Metall Export

- 10.8 Honeywell International Inc.

- 10.9 InterConnect Wiring

- 10.10 JST Sales America

- 10.11 kSARIA Corporation

- 10.12 Leonardo

- 10.13 Molex

- 10.14 PEI-Genesis

- 10.15 Pic Wire & Cable (Angelus Corporation)

- 10.16 Safran

- 10.17 TE Connectivity

- 10.18 W. L. Gore & Associates

電氣佈線互連系統市場:2026-2032年全球市場預測(按產品類型、電線類型、絕緣材料、導體材料、額定電壓、應用和最終用途行業分類)

電氣佈線互連系統市場:2026-2032年全球市場預測(按產品類型、電線類型、絕緣材料、導體材料、額定電壓、應用和最終用途行業分類) 電氣線路互連系統市場報告:趨勢、預測與競爭分析(至2035年)

電氣線路互連系統市場報告:趨勢、預測與競爭分析(至2035年) 全球電氣佈線互連系統市場-產業規模、佔有率、趨勢、機會和預測,按應用、航空類型、最終用戶、地區和競爭格局分類,2020-2030年預測

全球電氣佈線互連系統市場-產業規模、佔有率、趨勢、機會和預測,按應用、航空類型、最終用戶、地區和競爭格局分類,2020-2030年預測 軍用線束及電纜組件的全球市場 (~2035年):產品類型·屏蔽類型·平台·用途·各地區EWIS連接器市場報告:趨勢、預測與競爭分析(至2031年)全球軍用電氣佈線互連繫統 (EWIS) 市場:按組件、應用、最終用戶和地區進行預測(~2032 年)全球電氣布線互連系統(EWIS)市場:依類型、應用、最終用戶、地區(-2032)

軍用線束及電纜組件的全球市場 (~2035年):產品類型·屏蔽類型·平台·用途·各地區EWIS連接器市場報告:趨勢、預測與競爭分析(至2031年)全球軍用電氣佈線互連繫統 (EWIS) 市場:按組件、應用、最終用戶和地區進行預測(~2032 年)全球電氣布線互連系統(EWIS)市場:依類型、應用、最終用戶、地區(-2032)