|

市場調查報告書

商品編碼

1740820

CO2 雷射市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測CO2 Laser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

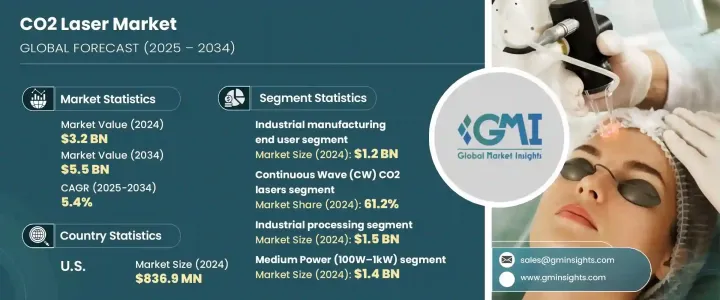

2024 年全球二氧化碳雷射器市場規模達 32 億美元,預計到 2034 年將以 5.4% 的複合年成長率成長,達到 55 億美元。這一成長得益於工業製造、醫療和美容等關鍵領域應用範圍的不斷擴大。二氧化碳雷射器憑藉其無與倫比的精度、多功能性以及加工塑膠、紡織品、玻璃和金屬等多種材料的能力,已成為首選技術。隨著各行各業日益轉向自動化和精密生產系統,二氧化碳雷射的採用率持續飆升。這些系統提供非接觸式加工,可最大限度地減少磨損、延長使用壽命,並確保切割更乾淨,同時最大程度地減少熱變形。

它們與工業 4.0 和智慧製造系統的整合,使其成為精簡營運、提升產品品質和減少浪費的關鍵資產。此外,對永續、節能生產技術日益成長的需求,進一步鞏固了它們作為各製造垂直領域重要工具的地位。技術進步,尤其是在光束控制、冷卻機制和模組化設計方面的進步,正在幫助製造商在不影響品質或效率的情況下擴大營運規模。因此,無論是老牌企業或新進者,都在利用這一趨勢,提升產品性能,擴大在高需求市場的影響力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 32億美元 |

| 預測值 | 55億美元 |

| 複合年成長率 | 5.4% |

CO2 雷射在需要複雜、非接觸式切割、焊接、鑽孔和雕刻解決方案的行業中日益受到青睞。與傳統加工工具相比,這些雷射可提供卓越的邊緣質量,並減少二次精加工的需求,從而顯著提高整體營運效率。其高速執行高精度任務的能力使其特別適合大規模生產環境。隨著製造商力求在保持品質標準的同時提高產量,CO2 雷射正擴大被部署用於替換老舊、效率低下的設備。

貿易政策持續影響市場動態,尤其是對來自關鍵雷射部件供應國的進口零件徵收關稅。這些政策變化增加了製造成本,促使企業重新思考其採購和營運模式。為了應對這些挑戰,許多企業正在探索替代供應商,並增加對國內製造能力的投資。這種轉變不僅有助於減少對全球貿易的依賴,也能縮短週轉時間,並提升供應鏈的韌性。儘管面臨這些不利因素,但由於對自動化和數位化整合生產生態系統的需求不斷成長,市場勢頭依然強勁。

在產品細分方面,中等功率類別(功率範圍從 100W 到 1kW)在 2024 年創造了 14 億美元的市場規模。該細分市場因其在高性能和經濟實惠之間實現了理想的平衡而持續受到歡迎。汽車、電子、紡織和包裝等行業青睞中功率 CO₂ 雷射器,因為它們能夠在各種材料上實現清晰的焊接、精細的標記和精細的雕刻。其緊湊的設計和高效的能源效率,使其對於希望在不超出預算的情況下實現自動化的中小型製造工廠尤其具有吸引力。這些系統還能與CNC工具機和機器人平台無縫整合,使其成為智慧工廠環境的理想選擇。

2024年,連續波 (CW) CO2 雷射器佔據了 61.2% 的市場佔有率,佔據主導地位,這反映出其在需要不間斷高強度雷射輸出的應用中得到了廣泛的應用。連續波雷射發射恆定的光束,可在結構金屬切割、深孔鑽孔和連續焊接等製程中實現深度穿透和始終如一的精度。航太、造船和重型機械等關鍵產業依賴這些雷射器,因為它們能夠在高產量生產線中高效運作。它們的可靠性和減少停機時間的能力與全球對精實製造和提高生產力的重視高度契合。

受先進製造業強勁需求的推動,美國二氧化碳雷射器市場在2024年達到8.369億美元。這些雷射在注重微觀精度和無縫自動化的行業中不可或缺。航太、醫療保健和消費性電子產品製造商正在採用二氧化碳雷射器,因為它們擁有卓越的精度和靈活的材料處理能力,可處理從金屬到聚合物的各種材料。在醫療領域,雷射輔助美容手術(例如皮膚重建和皮膚病治療)的日益普及也擴大了市場規模。

包括科醫人 (Lumenis)、相干公司 (Coherent, Inc.)、Epilog Laser、通快集團 (TRUMPF Group) 和科恩雷射系統 (Kern Laser Systems) 在內的領先公司正透過高性能雷射模組的策略研發鞏固其市場地位。這些公司正在擴展其產品組合,並客製化解決方案以滿足特定行業的獨特需求。與自動化公司和關鍵終端用戶的合作有助於強化供應鏈並改善服務交付。同時,對區域製造設施的投資正在擴大市場覆蓋範圍,並加快對不斷變化的貿易動態的反應。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 二氧化碳雷射在材料加工上的應用日益增多

- 醫療和美容應用需求激增

- 提高工業流程的自動化程度

- 二氧化碳雷射在國防和軍事領域的應用日益增多

- 雷射技術的不斷進步

- 產業陷阱與挑戰

- 初始資本投入高

- 替代雷射技術的出現

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按輸出功率,2021 - 2034 年

- 主要趨勢

- 低功率(100W以下)

- 中等功率(100W~1kW)

- 大功率(1kW以上)

第6章:市場估計與預測:依技術類型,2021-2034

- 主要趨勢

- 連續波(CW)CO2雷射器

- 脈衝二氧化碳雷射

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 醫療與美容

- 工業加工

- 科學與研究

- 感測與通訊

- 其他

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 航太和國防

- 工業製造

- 衛生保健

- 汽車

- 電信

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Alma Lasers

- Baison Laser

- Boss Laser

- Camfive Laser

- Epilog Laser

- Eurolaser

- Gravotech

- Haotian Laser

- INTERmedic

- JEISYS Medical

- JenaSurgical

- Kern Laser Systems

- Lasering USA

- Lumenis

- Lutronic

- Novanta Inc.

- OmniGuide

- RedSail

- Thunder Laser

- Trotec Laser

- Wattsan

The Global CO2 Laser Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 5.5 billion by 2034. This growth is fueled by an expanding range of applications across key sectors, including industrial manufacturing, medical treatments, and cosmetic procedures. CO2 lasers have emerged as a preferred technology due to their unmatched precision, versatility, and ability to process diverse materials such as plastics, textiles, glass, and metals. As industries increasingly shift toward automation and precision-based production systems, the adoption of CO2 lasers continues to surge. These systems offer non-contact processing, which minimizes wear and tear, boosts operational lifespan, and ensures cleaner cuts with minimal thermal distortion.

Their integration into Industry 4.0 and smart manufacturing setups makes them a critical asset in streamlining operations, improving product quality, and reducing waste. Moreover, the rising need for sustainable, energy-efficient production technologies further solidifies their position as an essential tool across various manufacturing verticals. Technological advancements, especially in beam control, cooling mechanisms, and modular design, are helping manufacturers scale operations without compromising on quality or efficiency. As a result, both established players and new entrants are capitalizing on this trend by enhancing product capabilities and expanding their presence in high-demand markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 billion |

| Forecast Value | $5.5 billion |

| CAGR | 5.4% |

CO2 lasers are gaining traction in industries that demand intricate, contact-free solutions for cutting, welding, drilling, and engraving. Compared to traditional processing tools, these lasers deliver superior edge quality and reduce the need for secondary finishing, which significantly improves overall operational efficiency. Their ability to execute high-precision tasks at high speed makes them particularly suitable for mass production environments. As manufacturers aim to improve throughput while maintaining quality standards, CO2 lasers are increasingly being deployed to replace older, less efficient equipment.

Trade policies continue to play a role in shaping market dynamics, especially tariffs on imported components from countries that supply essential laser parts. These policy changes have increased manufacturing costs, prompting companies to rethink their sourcing and operational models. To mitigate these challenges, many firms are exploring alternative suppliers and increasing investments in domestic manufacturing capabilities. This shift not only helps reduce dependency on global trade but also supports quicker turnaround times and improved supply chain resilience. Despite these headwinds, market momentum remains strong due to the growing demand for automation and digitally integrated production ecosystems.

In terms of product segmentation, the medium power category-ranging from 100W to 1kW-generated USD 1.4 billion in 2024. This segment continues to gain popularity as it offers an ideal balance between high performance and affordability. Industries such as automotive, electronics, textiles, and packaging prefer medium-power CO2 lasers for their ability to deliver clean welding, intricate marking, and detailed engraving across various materials. Their compact design and energy efficiency make them especially attractive for small to mid-sized manufacturing facilities looking to implement automation without overextending budgets. These systems also integrate seamlessly with CNC machines and robotics platforms, making them a natural fit for smart factory environments.

The Continuous Wave (CW) CO2 laser segment held a dominant 61.2% market share in 2024, reflecting its widespread use in applications that demand uninterrupted, high-intensity laser output. CW lasers emit a constant beam, enabling deep penetration and consistent precision in processes like structural metal cutting, deep-hole drilling, and continuous welding. Key industries such as aerospace, shipbuilding, and heavy machinery rely on these lasers for their ability to operate efficiently in high-throughput production lines. Their reliability and capacity to reduce downtime align well with the global emphasis on lean manufacturing and productivity enhancement.

The United States CO2 laser market generated USD 836.9 million in 2024, driven by strong demand across advanced manufacturing sectors. These lasers are indispensable in industries where microscopic precision and seamless automation are critical. Aerospace, healthcare, and consumer electronics manufacturers are adopting CO2 lasers for their exceptional accuracy and material-handling flexibility-from metals to polymers. In the medical space, the growing use of laser-assisted cosmetic procedures like skin resurfacing and dermatological treatments is also expanding the market scope.

Leading companies, including Lumenis, Coherent, Inc., Epilog Laser, TRUMPF Group, and Kern Laser Systems, are reinforcing their positions through strategic R&D in high-performance laser modules. These players are expanding their product portfolios and customizing solutions to meet the unique requirements of specific industries. Collaborations with automation firms and key end-users are helping strengthen supply chains and improve service delivery. At the same time, investments in regional manufacturing facilities are enhancing market reach and providing faster response times to shifting trade dynamics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increase in adoption of CO2 lasers in material processing

- 3.7.1.2 Surge in demand from medical and aesthetic applications

- 3.7.1.3 Increased automation in industrial processes

- 3.7.1.4 Rise in applications of CO2 lasers in the defense and military sector

- 3.7.1.5 Growing advancements in laser technology

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial capital investment

- 3.7.2.2 Emergence of alternative laser technologies

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Output Power, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low power (Below 100W)

- 5.3 Medium power (100W–1kW)

- 5.4 High power (Above 1kW)

Chapter 6 Market Estimates & Forecast, By Technology Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Continuous wave (CW) CO2 lasers

- 6.3 Pulsed CO2 lasers

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Medical & aesthetic

- 7.3 Industrial processing

- 7.4 Scientific & research

- 7.5 Sensing & communications

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Aerospace and defense

- 8.3 Industrial manufacturing

- 8.4 Healthcare

- 8.5 Automotive

- 8.6 Telecommunication

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alma Lasers

- 10.2 Baison Laser

- 10.3 Boss Laser

- 10.4 Camfive Laser

- 10.5 Epilog Laser

- 10.6 Eurolaser

- 10.7 Gravotech

- 10.8 Haotian Laser

- 10.9 INTERmedic

- 10.10 JEISYS Medical

- 10.11 JenaSurgical

- 10.12 Kern Laser Systems

- 10.13 Lasering USA

- 10.14 Lumenis

- 10.15 Lutronic

- 10.16 Novanta Inc.

- 10.17 OmniGuide

- 10.18 RedSail

- 10.19 Thunder Laser

- 10.20 Trotec Laser

- 10.21 Wattsan

二氧化碳雷射市場:按雷射類型、功率範圍、應用和最終用戶分類-全球預測,2026-2032年

二氧化碳雷射市場:按雷射類型、功率範圍、應用和最終用戶分類-全球預測,2026-2032年 全球二氧化碳雷射市場

全球二氧化碳雷射市場 2025年全球二氧化碳雷射市場報告2025年準分子雷射全球市場報告

2025年全球二氧化碳雷射市場報告2025年準分子雷射全球市場報告 雷射氣體供應服務市場報告:2030 年趨勢、預測與競爭分析

雷射氣體供應服務市場報告:2030 年趨勢、預測與競爭分析