|

市場調查報告書

商品編碼

1740819

飛機零件 MRO 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Aircraft Component MRO Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

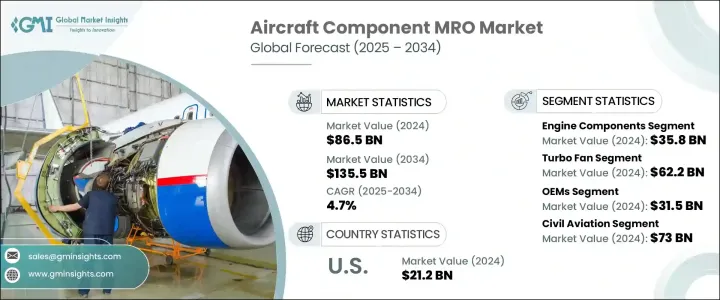

2024年,全球飛機零件MRO市場價值達865億美元,預計到2034年將以4.7%的複合年成長率成長,達到1355億美元,這得益於國際航空運輸量的激增和全球飛機機隊規模的擴大。隨著民航業的復甦和旅行需求的飆升,航空公司正在加大對維護、維修和大修服務的投資,以確保營運效率、法規合規性和乘客安全。隨著機隊日益多樣化和技術先進,MRO供應商正在利用尖端診斷工具、預測性維護技術和先進的材料修復技術來應對新的挑戰。人們對配備下一代引擎和整合系統的節油飛機的偏好日益成長,這正在重塑市場格局。隨著競爭加劇,營運商正在尋求更快的周轉時間、更高的技術專長和更具成本效益的解決方案,這促使MRO公司擴展能力、投資數位化並採用更智慧的服務模式以保持領先地位。

航空公司正在大力投資MRO服務,以滿足營運安全標準和不斷變化的監管要求。飛機系統(尤其是航空電子設備和推進部件)日益複雜,推動MRO流程採用數位化工具、智慧診斷和預測性維護技術。配備下一代引擎和整合電子系統的現代機隊對技術專長提出了更高的要求,這進一步刺激了全球對專業MRO服務的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 865億美元 |

| 預測值 | 1355億美元 |

| 複合年成長率 | 4.7% |

不斷變化的全球貿易政策為MRO業者帶來了更多障礙。對關鍵航空零件徵收進口關稅導致營運成本上升,尤其對美國供應商而言。這些關稅擾亂了現有的供應鏈,引發了人們對零件供應的嚴重擔憂,迫使航空公司重新考慮採購策略和維護計劃。同時,航空公司面臨越來越大的壓力,需要在確保完全合規的同時提高成本效益,這促使他們更加依賴長期服務協議,並擴大內部零件維修能力。

2024年,引擎零件市場產值達358億美元,佔據飛機零件MRO市場的主導地位。這一領先地位源於引擎零件至關重要且高昂的更換成本,這些零件需要細緻的維護和嚴格的大修計劃。燃燒室、渦輪葉片和燃油噴嘴等零件承受著極端的熱應力和機械應力,需要採用先進的修復工藝,包括熱障塗層、等離子噴塗和雷射熔覆。數位孿生和人工智慧驅動的診斷等智慧維護技術的整合正在徹底改變傳統的MRO工作流程,幫助供應商預測磨損模式,最大限度地減少停機時間,並顯著延長零件的使用壽命。

按飛機類型分類,渦輪扇引擎市場在2024年創造了622億美元的市場規模。渦輪風扇引擎複雜的設計和卓越的推力效率使其成為商用和軍用航空領域不可或缺的部件。這些引擎的維護程序通常涉及高精度雷射鑽孔和對高壓渦輪和風扇葉片等關鍵模組進行專門的防護塗層。隨著航空業追求更安靜、更省油的飛機,MRO服務供應商正在擴大其營運規模,以滿足採用複合材料和齒輪傳動結構的新一代引擎的需求。

在強勁的國內航空業的支撐下,美國飛機零件維護、大修 (MRO) 市場規模在 2024 年達到 212 億美元。美國擁有全球最大的商用飛機機隊之一,並在主要航空樞紐擁有密集的認證維修站和與原始設備製造商(OEM)合作的設施網路。戰略現代化建設和美國聯邦航空管理局 (FAA) 法規正在推動 MRO 能力的提升,尤其是在引擎和航空電子設備等關鍵系統方面。數位化記錄保存、永續性合規性和整合維護追蹤如今已成為美國 MRO 營運的核心。

飛機零件MRO產業的知名企業包括通用電氣公司、AAR、漢莎技術公司、新科工程公司和新航工程公司。這些領先公司正在拓展全球網路,投資數位化維護工具,並增強垂直整合的服務模式。與航空公司和原始設備製造商建立長期合作夥伴關係,專注於永續維修技術,以及提昇技術團隊的技能,仍然是增強服務可靠性並順應航空業發展趨勢的關鍵策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 川普政府關稅對飛機零件的影響分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響

- 價格傳導至終端市場

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 航空旅行需求不斷增加

- 航空當局的監管要求

- 將 MRO 活動外包給第三方供應商

- 低成本航空公司在全球的擴張

- 預測性維護技術的採用日益增多

- 產業陷阱與挑戰

- 零件維修成本高且複雜

- 全球熟練的MRO技術人員短缺

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依組件類型,2021 - 2034 年

- 主要趨勢

- 引擎部件

- 航空電子設備

- 起落架

- 機身部件

- 電氣系統

- 液壓系統

- 氣動系統

- 燃油系統

- 其他

第6章:市場估計與預測:依飛機類型,2021 - 2034 年

- 主要趨勢

- 渦輪螺旋槳飛機

- 渦輪軸

- 渦輪噴射引擎

- 渦輪風扇

- 窄體飛機

- 寬體飛機

- 支線噴射機

- 其他

第7章:市場估計與預測:依服務提供者類型,2021 - 2034 年

- 主要趨勢

- 原始設備製造商

- 航空公司(內部維修、維修和大修)

- 第三方 MRO 提供者(獨立)

- 軍事MRO單位

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 民航

- 軍事航空

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- MEA 其餘地區

第10章:公司簡介

- Lufthansa Technik

- General Electric Company

- ST Engineering

- SIA Engineering Company

- AAR

- AFI KLM E&M

- MTU Aero Engines AG

- Hong Kong Aircraft Engineering Company Limited.

- Delta Air Lines, Inc.

- Pratt & Whitney

- Rolls-Royce plc

- Ameco

- Turkish Technic Inc.

- Guangzhou Aircraft Maintenance Engineering Co.,Ltd.

- SR Technics Switzerland Ltd.

- AFI KLM E&M

- TAP.

- AJ Walter Aviation Limited

- Aero Norway AS

- StandardAero

The Global Aircraft Component MRO Market was valued at USD 86.5 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 135.5 billion by 2034, driven by the surge in international air traffic and the expanding global fleet of aircraft. As commercial aviation recovers and travel demand skyrockets, airlines are ramping up investments in maintenance, repair, and overhaul services to ensure operational efficiency, regulatory compliance, and passenger safety. With fleets becoming increasingly diverse and technologically advanced, MRO providers are adapting to new challenges by leveraging cutting-edge diagnostic tools, predictive maintenance technologies, and advanced material repair techniques. The rising preference for fuel-efficient aircraft, equipped with next-generation engines and integrated systems, is reshaping the market landscape. As competition intensifies, operators are seeking faster turnaround times, greater technical expertise, and cost-effective solutions, pushing MRO firms to expand capabilities, invest in digitalization, and adopt smarter service models to stay ahead.

Airlines are heavily investing in MRO services to meet operational safety standards and evolving regulatory mandates. Increasing complexity in aircraft systems, particularly in avionics and propulsion components, is pushing MRO procedures toward the adoption of digital tools, smart diagnostics, and predictive maintenance technologies. Modern fleets featuring next-generation engines and integrated electronic systems demand a higher degree of technical expertise, further fueling the global demand for specialized MRO services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $86.5 Billion |

| Forecast Value | $135.5 Billion |

| CAGR | 4.7% |

Shifting global trade policies are creating additional hurdles for MRO operators. The introduction of import tariffs on key aviation parts has elevated operational costs, especially for U.S.-based providers. These tariffs are disrupting established supply chains and raising serious concerns over component availability, compelling airlines to rethink procurement strategies and maintenance planning. At the same time, carriers are under mounting pressure to enhance cost-efficiency while ensuring full regulatory compliance, driving greater reliance on long-term service agreements and the expansion of in-house component repair capabilities.

The engine component segment generated USD 35.8 billion in 2024, dominating the aircraft component MRO market. This leadership comes from the critical importance and high replacement cost of engine parts, which require meticulous servicing and strict overhaul schedules. Components like combustors, turbine blades, and fuel nozzles endure extreme thermal and mechanical stress, necessitating advanced repair processes including thermal barrier coatings, plasma spraying, and laser cladding. The integration of smart maintenance technologies such as digital twins and AI-driven diagnostics is revolutionizing traditional MRO workflows, helping providers predict wear patterns, minimize downtime, and significantly extend component lifespans.

By aircraft type, the turbofan engines segment generated USD 62.2 billion in 2024. Turbofan engines' complex design and superior thrust efficiency make them essential across both commercial and military aviation sectors. Maintenance procedures for these engines often involve high-precision laser drilling and specialized protective coatings for critical modules like high-pressure turbines and fan blades. As the aviation industry pushes for quieter and more fuel-efficient aircraft, MRO service providers are scaling their operations to meet the needs of new-generation engines made with composite materials and geared architectures.

The U.S. Aircraft Component MRO Market reached USD 21.2 billion in 2024, supported by a robust domestic aviation industry. Hosting one of the world's largest commercial aircraft fleets, the U.S. boasts a dense network of certified repair stations and OEM-aligned facilities across key aviation hubs. Strategic modernization efforts and FAA regulations are driving advancements in MRO capabilities, especially for critical systems like engines and avionics. Digital recordkeeping, sustainability compliance, and integrated maintenance tracking are now central to U.S. MRO operations.

Prominent players in the aircraft component MRO industry include General Electric Company, AAR, Lufthansa Technik, ST Engineering, and SIA Engineering Company. Leading firms are expanding global networks, investing in digital maintenance tools, and enhancing vertically integrated service models. Long-term partnerships with airlines and OEMs, focus on sustainable repair technologies, and upskilling of technical teams remain key strategies to strengthen service reliability and align with evolving aviation industry trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs impact analysis on aircraft components

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-Side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-Side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Consumer response patterns

- 3.2.1.3.1 Supply-Side impact

- 3.2.1.4 Key Companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for air travel

- 3.3.1.2 Regulatory mandates from aviation authorities

- 3.3.1.3 Outsourcing MRO activities to third-party providers

- 3.3.1.4 Expansion of low-cost carrier operations globally

- 3.3.1.5 Increasing adoption of predictive maintenance technologies

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost and complexity of component repairs

- 3.3.2.2 Shortage of skilled MRO technicians globally

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Component Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Engine components

- 5.3 Avionics

- 5.4 Landing gear

- 5.5 Airframe components

- 5.6 Electrical systems

- 5.7 Hydraulic systems

- 5.8 Pneumatic systems

- 5.9 Fuel systems

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Turboprops

- 6.3 Turbo shafts

- 6.4 Turbo jet

- 6.5 Turbo fan

- 6.5.1 Narrow-body

- 6.5.2 Wide-body

- 6.5.3 Regional jets

- 6.5.4 Others

Chapter 7 Market Estimates & Forecast, By Service Provider Type, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Airlines (In-house MRO)

- 7.4 Third-Party MRO Providers (Independent)

- 7.5 Military MRO Units

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Civil aviation

- 8.3 Military aviation

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Lufthansa Technik

- 10.2 General Electric Company

- 10.3 ST Engineering

- 10.4 SIA Engineering Company

- 10.5 AAR

- 10.6 AFI KLM E&M

- 10.7 MTU Aero Engines AG

- 10.8 Hong Kong Aircraft Engineering Company Limited.

- 10.9 Delta Air Lines, Inc.

- 10.10 Pratt & Whitney

- 10.11 Rolls-Royce plc

- 10.12 Ameco

- 10.13 Turkish Technic Inc.

- 10.14 Guangzhou Aircraft Maintenance Engineering Co.,Ltd.

- 10.15 SR Technics Switzerland Ltd.

- 10.16 AFI KLM E&M

- 10.17 TAP.

- 10.18 A J Walter Aviation Limited

- 10.19 Aero Norway AS

- 10.20 StandardAero