|

市場調查報告書

商品編碼

1740813

有機乾酒糟飼料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Organic Dried Distiller's Grain Feed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

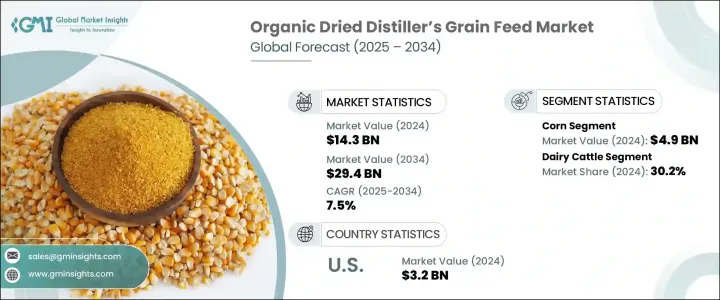

2024年,全球有機乾酒糟飼料市場價值143億美元,預計到2034年將以7.5%的複合年成長率成長,達到294億美元,這得益於有機畜產品需求的不斷成長,以及全行業對永續、環保的農業實踐的推動。隨著消費者偏好迅速轉向更清潔、更符合道德標準的食品,畜牧業面臨越來越大的壓力,需要與有機和再生飼料系統接軌。有機乾酒糟(DDG)正日益成為關鍵解決方案,彌合營養需求與有機合規性之間的差距。全球貿易中斷也凸顯了具有韌性、可追溯性的供應鏈的重要性,這進一步將有機乾酒糟定位為傳統飼料的可行替代品。隨著有機認證標準的收緊以及人們對動物福利和永續性的認知不斷加深,生產商正在迅速採用有機飼料投入,以滿足監管要求和消費者信任。在整個畜牧業,從家禽到乳牛和肉牛,有機玉米酒糟粕 (DDG) 如今已成為營養計畫中的關鍵成分,不僅性能可靠,而且符合有機認證標準。這一成長軌跡得益於持續的投資、不斷發展的監管框架以及成熟市場和新興市場的基礎設施建設。

過去幾年,隨著乙醇生產商轉向有機穀物投入並尋求生產設施認證,經認證的有機玉米酒糟粕(DDG)供應量大幅增加。這些發展正值市場對永續透明農業供應鏈的需求達到新高之際。生產商和飼料製造商比以往任何時候都更渴望採用既符合永續發展目標又符合市場需求的有機解決方案。北美憑藉其完善的有機農業生態系統,繼續在市場應用方面保持領先地位。然而,隨著各國投資有機生產模式並加強其認證和分銷基礎設施,亞太地區正迅速迎頭趕上。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 143億美元 |

| 預測值 | 294億美元 |

| 複合年成長率 | 7.5% |

玉米乾酒糟仍是主要原料,2024年將創造49億美元的收入,預計2034年將以7%的複合年成長率成長。玉米的廣泛供應、高澱粉含量以及乙醇發酵效率使其成為有機乾酒糟(DDG)生產的首選作物。玉米乾酒糟富含蛋白質和能量,營養密度高,也使其特別適合有機畜牧系統。對於依賴優質飼料投入以滿足嚴格的有機認證標準的生產商來說,這種一致性至關重要。隨著畜牧生產商繼續優先考慮營養和合規性,預計玉米乾酒糟將在有機飼料領域保持領先。

在動物應用方面,乳牛是最大的消費群。預計2024年乳牛市場價值將達到43億美元,複合年成長率將達到7.8%,反映了有機乾玉米酒糟(DDG)在滿足乳牛養殖業飲食需求方面發揮的關鍵作用。有機乳牛場限制使用合成添加劑和抗生素,越來越依賴有機乾玉米酒糟來天然提供蛋白質和纖維。這不僅有助於維持產奶量,還能促進牛群整體健康和活力。隨著全球對有機乳製品需求的成長,營養豐富、符合有機標準的飼料對該產業的重要性將日益凸顯。

2024年,美國有機乾酒糟飼料市場產值達32億美元,預計複合年成長率為7.3%。這一成長得益於人們對再生農業日益成長的興趣,以及消費者青睞永續、來源透明的動物產品。美國飼料製造商正在迅速適應,將有機乾酒糟(DDG)納入營養計劃,以支持性能和環境目標。鑑於其在循環農業中的作用——重新利用有機乙醇生產的副產品——有機乾酒糟正成為尋求提高生產力和永續性的美國生產商的誘人選擇。

弗林特山資源公司 (Flint Hills Resources)、阿徹丹尼爾斯米德蘭公司 (ADM)、綠色平原公司 (Green Plains Inc.)、POET LLC 和瓦萊羅能源公司 (Valero Energy Corporation) 等領先公司正在積極投資擴張和認證。這些關鍵參與者正在升級設施以滿足有機標準,與有機穀物供應商合作,並客製化其產品線以滿足特定的牲畜營養需求。策略合作夥伴關係以及對可追溯性和透明度的日益重視,繼續決定這些公司的市場策略,因為它們在不斷發展的有機飼料格局中為長期成長做好了準備。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 供給側影響(原料)

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 貿易統計(HS編碼)

- 2021-2024年主要出口國

- 2021-2024年主要進口國

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 消費者對有機動物產品的需求不斷增加

- 擴大有機畜禽養殖

- 政府支持和有機認證政策

- 強調永續和循環的農業實踐

- 產業陷阱與挑戰

- 經過認證的有機原料供應有限

- 與傳統飼料相比生產加工成本較高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依來源,2021-2034

- 主要趨勢

- 玉米

- 小麥

- 米

- 大麥

- 高粱

- 燕麥

- 黑麥

- 粟

- 其他

第6章:市場估計與預測:依動物類型,2021-2034

- 主要趨勢

- 乳牛

- 肉牛

- 豬

- 家禽

- 水藍色

- 其他動物類型

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 動物飼料

- 生物能源生產

- 肥料和土壤改良劑

- 其他

第8章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 線上

- 離線

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Bayer Animal Health

- ADM

- Agrifeeds

- Alcogroup SA

- Chimique India

- COFCO Biochemical (Anhui) Co. Ltd.

- Feedpedia

- Furst-McNess Company

- Greenfield Global Inc.

- Gulshan Polyols Ltd.

- Kemin Industries, Inc.

- Midas Overseas

- Nutrigo Feeds Pvt Ltd

- Poet LLC

- Valero Energy Corporation

The Global Organic Dried Distiller's Grain Feed Market was valued at USD 14.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 29.4 billion by 2034, driven by the rising demand for organic livestock products and an industry-wide push toward sustainable, eco-conscious farming practices. With consumer preferences rapidly shifting toward cleaner, ethically sourced food, the livestock sector is under mounting pressure to align with organic and regenerative feed systems. Organic DDGs are increasingly emerging as a key solution, bridging the gap between nutritional needs and organic compliance. Global trade disruptions have also heightened the importance of resilient, traceable supply chains-further positioning organic DDGs as a viable alternative to conventional feed. As organic certification standards tighten and awareness surrounding animal welfare and sustainability deepens, producers are rapidly adopting organic feed inputs to meet both regulatory expectations and consumer trust. Across the livestock industry, from poultry to dairy and beef cattle, organic DDGs are now a crucial ingredient in nutrition programs, offering both performance reliability and alignment with organic certifications. This growth trajectory is supported by continued investments, evolving regulatory frameworks, and infrastructure developments across established and emerging markets.

Over the past few years, the supply of certified organic DDGs has grown considerably, as ethanol producers shift toward organic grain inputs and seek certification for their production facilities. These developments come at a time when the demand for sustainable and transparent agricultural supply chains is reaching new heights. Producers and feed manufacturers are more eager than ever to embrace organic solutions that align with both sustainability goals and market demand. North America continues to lead in market adoption due to its well-established organic agriculture ecosystem. However, the Asia-Pacific region is quickly catching up, as countries invest in organic production models and enhance their certification and distribution infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $29.4 Billion |

| CAGR | 7.5% |

Corn-based dried distiller's grain remains the dominant feedstock, generating USD 4.9 billion in revenue in 2024 and projected to grow at a 7% CAGR through 2034. Corn's widespread availability, high starch content, and efficiency in ethanol fermentation make it a preferred crop for organic DDG production. The nutritional density of corn-derived DDGs, rich in protein and energy, also makes it especially well-suited for organic livestock systems. This consistency is vital for producers who rely on quality feed inputs to meet stringent organic certification standards. As livestock producers continue to prioritize nutrition and compliance, corn-based DDG is expected to retain its leadership in the organic feed segment.

In terms of animal application, dairy cattle represent the largest consumer segment. Valued at USD 4.3 billion in 2024 and forecasted to grow at a CAGR of 7.8%, this segment reflects the critical role that organic DDG plays in supporting the dietary needs of dairy operations. Organic dairy farms, which restrict the use of synthetic additives and antibiotics, increasingly rely on organic DDGs to deliver protein and fiber naturally. This not only helps maintain milk production levels but also supports overall herd health and vitality. As demand for organic dairy products grows globally, the importance of nutrient-rich, organically compliant feed will only become more central to the sector.

The United States Organic Dried Distiller's Grain Feed Market generated USD 3.2 billion in 2024 and is expected to grow at a 7.3% CAGR. This growth is fueled by increased interest in regenerative agriculture and consumer trends favoring sustainable, transparently sourced animal products. US feed manufacturers are adapting swiftly by integrating organic DDGs into nutrition plans that support both performance and environmental goals. Given their role in circular agriculture-repurposing by-products of organic ethanol production-organic DDGs are becoming an attractive choice for American producers looking to boost both productivity and sustainability.

Leading companies such as Flint Hills Resources, Archer Daniels Midland Company (ADM), Green Plains Inc., POET LLC, and Valero Energy Corporation are actively investing in expansion and certification. These key players are upgrading facilities to meet organic standards, collaborating with organic grain suppliers, and tailoring their product lines to cater to specific livestock nutrition requirements. Strategic partnerships and a growing emphasis on traceability and transparency continue to define the market strategies of these firms as they position themselves for long-term growth in the evolving organic feed landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.3 Demand-Side Impact (Selling Price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing consumer demand for organic animal products

- 3.8.1.2 Expansion of organic livestock and poultry farming

- 3.8.1.3 Government support and organic certification policies

- 3.8.1.4 Emphasis on sustainable and circular agricultural practices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited availability of certified organic raw materials

- 3.8.2.2 High production and processing costs compared to conventional feed

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn

- 5.3 Wheat

- 5.4 Rice

- 5.5 Barley

- 5.6 Sorghum

- 5.7 Oats

- 5.8 Rye

- 5.9 Millet

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Animal Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy cattle

- 6.3 Beef cattle

- 6.4 Swine

- 6.5 Poultry

- 6.6 Aqua

- 6.7 Other animal types

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Animal feed

- 7.3 Bioenergy production

- 7.4 Fertilizers & Soil amendments

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer Animal Health

- 10.2 ADM

- 10.3 Agrifeeds

- 10.4 Alcogroup SA

- 10.5 Chimique India

- 10.6 COFCO Biochemical (Anhui) Co. Ltd.

- 10.7 Feedpedia

- 10.8 Furst-McNess Company

- 10.9 Greenfield Global Inc.

- 10.10 Gulshan Polyols Ltd.

- 10.11 Kemin Industries, Inc.

- 10.12 Midas Overseas

- 10.13 Nutrigo Feeds Pvt Ltd

- 10.14 Poet LLC

- 10.15 Valero Energy Corporation