|

市場調查報告書

商品編碼

1740792

無線心臟監測系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Wireless Cardiac Monitoring Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

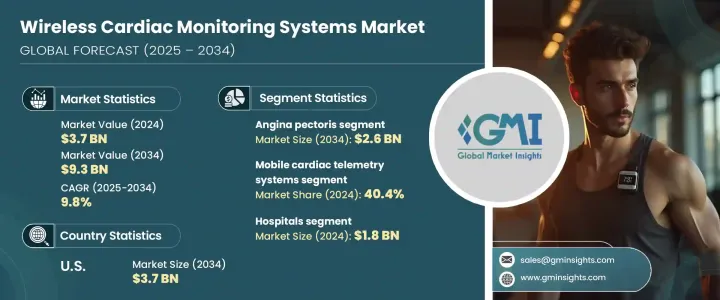

2024年,全球無線心臟監測系統市場規模達37億美元,預計2034年將以9.8%的複合年成長率成長,達到93億美元。這主要得益於全球範圍內對即時遠端心臟護理日益成長的需求以及心血管疾病日益普遍的發病率。無線心臟監測系統正在改變醫護人員監測心臟健康的方式,以實現持續追蹤和無線資料傳輸。這些系統透過提供近乎即時的洞察,幫助醫生更快、更精準地做出臨床反應,在早期識別心房顫動、心臟衰竭和心律不整等心臟相關疾病方面發揮關鍵作用。隨著老齡化人口和慢性病患者對持續監測的需求不斷成長,無線心臟監測的吸引力也日益凸顯。

技術創新仍然是推動這一市場發展的關鍵催化劑。新一代設備如今具備即時心電圖傳輸、人工智慧分析以及與雲端平台整合等先進功能,使臨床醫生能夠更有效地解讀心臟資料並迅速採取行動。這些工具顯著提高了診斷的準確性,並改善了患者護理效果,尤其是在門診或遠端環境中。日益向分散式護理和居家監護的轉變進一步推動了這個市場的擴張,使這些系統成為現代心臟護理的重要組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 37億美元 |

| 預測值 | 93億美元 |

| 複合年成長率 | 9.8% |

就產品細分而言,市場分為植入式心臟監視器 (ICM)、行動心臟遙測 (MCT) 系統和其他無線心臟監測產品。截至 2023 年,全球市場價值為 34 億美元,其中行動心臟遙測系統在 2024 年的營收佔有率為 40.4%。 MCT 設備能夠即時、連續地監測心律,並透過藍牙或蜂窩連接自主發送警報。此功能可確保立即檢測和報告異常心臟活動,從而提供一種主動的方法來診斷傳統的短期監測可能忽略的短暫性心律不整。門診環境中的廣泛應用以及對攜帶式、經濟高效的監測解決方案的日益偏好進一步支持了這一細分市場的持續成長。這些優勢對於需要長期照護的患者以及專注於降低再入院率和住院費用的醫療保健系統尤其重要。

無線心臟監測系統在心絞痛等疾病的管理中也發揮著至關重要的作用,這類疾病通常需要持續觀察,以識別可能引發嚴重心臟事件的缺血性事件或異常情況。即時監測有助於更好地評估症狀模式和誘因,從而實現更個人化、更及時的介入。當症狀出現異常或異常時,持續監測可以提供靜態測試方法可能遺漏的關鍵訊息,從而支持風險管理和預防保健策略。

從終端用途來看,市場細分為醫院、專科診所、診斷中心、家庭護理機構等。 2024年,光是醫院市場就達到了18億美元。配備先進心臟科室和專業人員的醫院是無線心臟技術的領先採用者,利用這些技術來提高診斷精度並最佳化患者護理路徑。在這些機構中,對支援雲端整合和人工智慧驅動資料管理的技術的投資也日益普遍,從而實現了即時分析和更快的醫療決策。此外,醫院正在積極採用尖端系統,包括穿戴式心電圖感測器和植入式設備,以提供高品質的護理並簡化營運。

預計到2034年,美國無線心臟監測系統市場規模將超過37億美元,這得益於其強大的醫療基礎設施和心血管疾病發生率的上升。美國受益於醫療創新的快速普及以及監管機構和投資者的持續支持。國內企業和研究機構也在開發下一代監測解決方案方面發揮關鍵作用,進一步推動了市場發展。心臟相關健康問題的日益成長以及對先進診斷工具的需求,正在推動臨床和家庭環境中無線心臟監測系統的採用率不斷提高。

該行業競爭依然激烈,美敦力、雅培實驗室、波士頓科學、iRhythm Technologies 和荷蘭皇家飛利浦等主要公司合計佔據全球約 40% 的市場佔有率。這些公司持續專注於遠端監控、人工智慧輔助診斷和無縫資料傳輸技術的突破,以在這個快速發展的市場中保持領先地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 心血管疾病(CVD)盛行率上升

- 無線心臟監測技術的技術進步

- 日益重視預防性醫療保健

- 產業陷阱與挑戰

- 農村和低度開發地區的可用性有限

- 嚴格的監管要求

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 各國應對措施

- 對產業的影響

- 供應方影響(製造成本)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(消費者成本)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(製造成本)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 植入式心臟監測儀(ICM)

- 移動心臟遙測系統

- 鉛基

- 基於補丁

- 其他產品

第6章:市場估計與預測:按適應症,2021 - 2034 年

- 主要趨勢

- 冠狀動脈疾病

- 心絞痛

- 動脈粥狀硬化

- 心臟衰竭

- 中風

- 其他適應症

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 診斷中心

- 居家照護環境

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- AliveCor

- Baxter International

- Biotronik

- Boston Scientific

- InfoBionic

- iRhythm Technologies

- Koninklijke Philips NV

- Medtronic

- Nihon Kohden

- SmartCardia

- Vital Connect

The Global Wireless Cardiac Monitoring Systems Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 9.3 billion by 2034, driven by the rising demand for real-time, remote cardiac care and the increasing prevalence of cardiovascular diseases worldwide. Wireless cardiac monitoring systems are transforming how healthcare professionals monitor heart health, allowing continuous tracking and wireless data transmission. These systems play a critical role in the early identification of heart-related conditions such as atrial fibrillation, heart failure, and arrhythmias by providing near real-time insights that enable faster and more precise clinical responses. As demand for continuous monitoring rises in aging populations and patients with chronic conditions, the appeal of wireless cardiac monitoring becomes more pronounced.

Technological innovation remains a key catalyst behind this market's momentum. New-generation devices now offer advanced features such as real-time ECG transmission, AI-enabled analytics, and integration with cloud platforms, empowering clinicians to interpret cardiac data more effectively and act promptly. These tools significantly enhance the accuracy of diagnosis and improve patient care outcomes, especially in outpatient or remote settings. The increasing shift toward decentralized care and home-based monitoring further fuels this market expansion, making these systems an essential component of modern cardiac care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 9.8% |

In terms of product segmentation, the market is categorized into implantable cardiac monitors (ICMs), mobile cardiac telemetry (MCT) systems, and other wireless cardiac monitoring products. As of 2023, the global market was valued at USD 3.4 billion, with mobile cardiac telemetry systems accounting for 40.4% of the revenue share in 2024. MCT devices enable real-time, continuous monitoring of cardiac rhythms and autonomously transmit alerts using Bluetooth or cellular connectivity. This functionality ensures immediate detection and reporting of abnormal heart activity, offering a proactive approach to diagnosing transient arrhythmias that traditional short-term monitoring may overlook. The consistent growth of this segment is further supported by broader adoption in outpatient settings and an increasing preference for portable, cost-efficient monitoring solutions. These benefits are particularly significant for patients requiring long-term care and for healthcare systems focused on reducing hospital readmissions and in-patient costs.

Wireless cardiac monitoring systems also play a vital role in managing conditions like angina pectoris, which often require ongoing observation to identify ischemic events or irregularities that can precede serious cardiac episodes. Real-time monitoring facilitates better evaluation of symptom patterns and triggers, allowing for more personalized and timely interventions. When symptoms occur unpredictably or present atypically, continuous monitoring provides critical insights that static testing methods might miss, thereby supporting risk management and preventive care strategies.

From an end-use perspective, the market is segmented into hospitals, specialty clinics, diagnostic centers, homecare settings, and others. In 2024, the hospital segment alone reached USD 1.8 billion. Hospitals equipped with advanced cardiology departments and specialized staff are leading adopters of wireless cardiac technologies, using them to improve diagnostic precision and optimize patient care pathways. Investments in technologies that support cloud integration and AI-driven data management have also become increasingly common in these facilities, enabling real-time analysis and faster medical decisions. Additionally, hospitals are actively adopting cutting-edge systems, including wearable ECG sensors and implantable devices, to deliver high-quality care and streamline operations.

The United States wireless cardiac monitoring systems market is projected to surpass USD 3.7 billion by 2034, driven by robust healthcare infrastructure and rising incidence of cardiovascular disease. The country benefits from the rapid adoption of medical innovations and consistent support from both regulatory bodies and investors. Domestic companies and research institutes are also playing a pivotal role in developing next-generation monitoring solutions, further advancing the market. The rise in heart-related health concerns and demand for advanced diagnostic tools are pushing adoption rates higher across clinical and home settings.

This industry remains highly competitive, with key players like Medtronic, Abbott Laboratories, Boston Scientific, iRhythm Technologies, and Koninklijke Philips N.V. collectively accounting for around 40% of the global market share. These companies continue to focus on breakthroughs in remote monitoring, AI-assisted diagnostics, and seamless data transmission technologies to stay ahead in this fast-evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased prevalence of cardiovascular diseases (CVDs)

- 3.2.1.2 Technological advancements in wireless cardiac monitoring technologies

- 3.2.1.3 Rising emphasis on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability in rural and underdeveloped areas

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implantable cardiac monitors (ICM)

- 5.3 Mobile cardiac telemetry systems

- 5.3.1 Lead-based

- 5.3.2 Patch-based

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Angina pectoris

- 6.4 Atherosclerosis

- 6.5 Heart failure

- 6.6 Stroke

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Diagnostic centers

- 7.5 Home care settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AliveCor

- 9.3 Baxter International

- 9.4 Biotronik

- 9.5 Boston Scientific

- 9.6 InfoBionic

- 9.7 iRhythm Technologies

- 9.8 Koninklijke Philips N.V.

- 9.9 Medtronic

- 9.10 Nihon Kohden

- 9.11 SmartCardia

- 9.12 Vital Connect

2026年全球無線心臟監測系統市場報告

2026年全球無線心臟監測系統市場報告 無線心臟監測系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途地區和競爭格局分類,2020-2030年預測

無線心臟監測系統市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、最終用途地區和競爭格局分類,2020-2030年預測 全球無線心臟監測系統市場

全球無線心臟監測系統市場 全球無線心臟監測系統市場 2024-2031

全球無線心臟監測系統市場 2024-2031