|

市場調查報告書

商品編碼

1740746

手術頭盔市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Surgical Helmet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

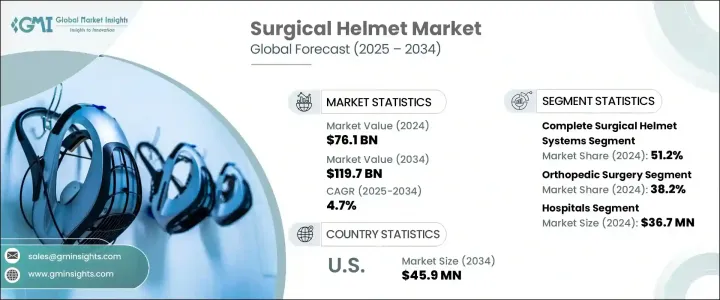

2024 年全球手術頭盔市場價值為 7,610 萬美元,預計到 2034 年將以 4.7% 的複合年成長率成長至 1.197 億美元。這一成長主要源於對更安全手術環境的需求不斷成長,以及全球複雜醫療程序的不斷增加。隨著外科手術實踐的不斷發展,人們越來越重視能夠最大限度地降低手術過程中污染和感染風險的防護設備。手術頭盔已成為手術室規程的重要組成部分,旨在保持無菌並提供先進的防護功能。這些頭盔不僅覆蓋外科醫生的頭部,還通常配備其他功能,如內置照明、通風系統和動力供氣裝置,從而提高外科醫生在長時間手術中的安全性和舒適度。

全球範圍內手術損傷發生率的上升顯著影響了市場擴張。緊急手術(尤其是涉及創傷的手術)數量的增加,加劇了對有效防護裝備的需求。隨著手術量的攀升,對能夠確保手術空間無菌和無污染的頭盔的需求也隨之成長。此外,手術頭盔設計和技術的改進使其在高風險手術環境中更易於日常使用,也更有效率。這些現代頭盔不僅可以保護手術人員免受空氣傳播的病原體和體液的侵害,還可以透過整合人體工學和視覺增強功能,減輕長時間手術過程中的疲勞。製造商正在開發具有更好氣流、更高可視性和輕質材料的先進型號,所有這些都旨在提升用戶體驗,同時保持嚴格的衛生標準。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7610萬美元 |

| 預測值 | 1.197億美元 |

| 複合年成長率 | 4.7% |

就產品類型而言,完整的手術頭盔系統在2024年佔據全球市場佔有率的51.2%,佔據主導地位。其主導地位源自於其一體化設計,能夠提供全面的保護。這些頭盔通常覆蓋整個頭部和上身,形成密封屏障,最大限度地降低交叉污染的可能性。此外,整合LED照明的款式也進一步提升了其受歡迎程度,在嚴苛的手術環境中,該照明能夠提供更佳的可視性。這項附加功能不僅提高了手術的精準度,也減輕了手術團隊的視覺壓力。

市場也呈現出基於應用的明顯細分。 2024年,骨科手術是最大的應用領域,佔了38.2%的市場。關節重建、脊椎矯正和其他肌肉骨骼疾病相關手術的日益增多,進一步推動了這項需求。這些手術通常耗時較長,且感染風險較高,因此防護頭盔成為手術室裝備的重要組成部分。已開發經濟體和新興經濟體中此類手術的增多,凸顯了手術頭盔在現代醫學中的重要角色。

從終端使用情況來看,醫院成為主導細分市場,2024 年市場規模達 3,670 萬美元。與其他醫療機構相比,醫院通常會進行更多手術,這自然會導致手術頭盔的消耗量更高。此外,醫院更有可能遵守嚴格的感染控制法規,其中許多法規要求使用個人防護裝備。隨著資金和基礎設施資源的增加,醫院可以投資更高品質的手術頭盔,從而鞏固其市場領導地位。

美國手術頭盔市場預計將經歷顯著成長,預計到2034年收入將達到4,590萬美元。美國廣泛的外科手術活動和嚴格的手術安全監管框架將進一步推動這一需求。美國醫療保健產業持續重視感染控制和安全措施,使手術頭盔成為手術室的標準配備。醫療基礎設施和安全技術投資的不斷增加也進一步推動了這一趨勢。

全球市場競爭激烈,成熟品牌和新進者都在努力創新和改進產品。 Zimmer Biomet、Stryker、MAXAIR Systems、Ecolab 和 THI Total Healthcare Innovation 等領先企業共佔據約 30% 的市佔率。這些公司正在投資先進的通風技術、防霧技術和整合式面罩等功能,以提高舒適度、可視性和整體手術性能。由於創新仍然是市場競爭力的核心,製造商不斷升級其產品,以滿足不斷變化的手術要求和監管標準。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 外科手術數量不斷增加

- 道路和運動事故數量不斷增加

- 手術頭盔的技術進步

- 日益重視感染控制

- 產業陷阱與挑戰

- 先進安全帽成本高昂

- 成長動力

- 成長潛力分析

- 監管格局

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供應方影響(原料)

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 完整的手術頭盔系統

- 帶LED

- 不含 LED

- 通風手術頭盔

- 其他產品類型

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 骨科手術

- 神經外科

- 心臟手術

- 耳鼻喉手術

- 一般外科

- 其他應用

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心(ASC)

- 專科診所

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- AresAir

- Beijing ZKSK Technology

- Ecolab

- Kaiser Technology

- Maharani Medicare

- MAXAIR Systems

- Prodancy

- Stryker

- THI Total Healthcare Innovation

- Zimmer Biomet

The Global Surgical Helmet Market was valued at USD 76.1 million in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 119.7 million by 2034. This growth is largely driven by the increasing demand for safer surgical environments and the rising number of complex medical procedures being performed worldwide. As surgical practices continue to evolve, there's a growing emphasis on protective equipment that minimizes the risk of contamination and infection during operations. Surgical helmets have become an essential part of operating room protocols, designed to maintain sterility and offer advanced protective features. These helmets not only cover the surgeon's head but often come equipped with additional functionalities such as built-in lighting, ventilation systems, and powered air supply mechanisms, enhancing both safety and surgeon comfort during long procedures.

Market expansion is significantly influenced by the increased global incidence of injuries requiring surgery. The rising number of emergency surgeries, particularly those involving trauma, has amplified the need for effective protective gear. As surgical volumes climb, so does the demand for headgear that can ensure a sterile and contamination-free operating space. Additionally, improvements in surgical helmet design and technology have made them more accessible and effective for daily use in high-risk surgical environments. These modern helmets not only shield the surgical staff from airborne pathogens and bodily fluids but also reduce fatigue during long procedures by integrating ergonomic and visual enhancements. Manufacturers are responding by developing advanced models with better airflow, improved visibility, and lightweight materials, all aimed at enhancing user experience while maintaining strict hygiene standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76.1 Million |

| Forecast Value | $119.7 Million |

| CAGR | 4.7% |

In terms of product type, complete surgical helmet systems took the lead in 2024, accounting for 51.2% of the global market. Their dominance is due to the all-in-one nature of these systems, which offer comprehensive protection. These helmets typically cover the entire head and upper body, creating a sealed barrier that minimizes the chances of cross-contamination. Their popularity is further boosted by the availability of variations featuring integrated LED lighting, which supports better visibility in challenging surgical environments. This added feature not only improves the precision of procedures but also reduces visual strain on the surgical team.

The market also shows strong segmentation based on application. Orthopedic surgeries represented the largest application area in 2024, capturing a 38.2% market share. The growing number of procedures related to joint reconstruction, spinal corrections, and other musculoskeletal conditions is fueling this demand. These surgeries often involve long hours and carry a high risk of exposure to infection, making protective headgear a crucial component of operating room gear. The increased frequency of such procedures across both developed and emerging economies highlights the essential role of surgical helmets in modern medicine.

Based on end-use settings, hospitals emerged as the dominant segment, accounting for USD 36.7 million in 2024. Hospitals typically perform a larger volume of surgeries compared to other healthcare facilities, which naturally translates to higher consumption of surgical helmets. Additionally, hospitals are more likely to follow stringent infection control regulations, many of which mandate the use of personal protective equipment. With more financial and infrastructural resources at their disposal, hospitals can invest in higher-quality surgical helmets, reinforcing their leadership position in the market.

The U.S. surgical helmet market is projected to experience considerable growth, with revenues expected to reach USD 45.9 million by 2034. The demand is bolstered by the country's extensive surgical activity and strict regulatory framework regarding surgical safety. The U.S. healthcare sector continues to prioritize infection control and safety measures, making surgical helmets a standard component in operating rooms. This trend is further supported by increasing investments in medical infrastructure and safety technologies.

The global market is competitive, with both established brands and new entrants striving to innovate and improve product offerings. Leading players such as Zimmer Biomet, Stryker, MAXAIR Systems, Ecolab, and THI Total Healthcare Innovation collectively hold around 30% of the market share. These companies are investing in features like advanced ventilation, anti-fog technologies, and integrated face shields to enhance comfort, visibility, and overall surgical performance. As innovation remains central to market competitiveness, manufacturers are constantly upgrading their products to meet evolving surgical requirements and regulatory standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures

- 3.2.1.2 Increasing number of road and sports accidents

- 3.2.1.3 Technological advancements in surgical helmets

- 3.2.1.4 Rising emphasis on infection control

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with advanced helmets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Complete surgical helmet systems

- 5.2.1 With LED

- 5.2.2 Without LED

- 5.3 Ventilated surgical helmets

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Orthopedic surgery

- 6.3 Neurosurgery

- 6.4 Cardiac surgery

- 6.5 ENT surgery

- 6.6 General surgery

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Specialty clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AresAir

- 9.2 Beijing ZKSK Technology

- 9.3 Ecolab

- 9.4 Kaiser Technology

- 9.5 Maharani Medicare

- 9.6 MAXAIR Systems

- 9.7 Prodancy

- 9.8 Stryker

- 9.9 THI Total Healthcare Innovation

- 9.10 Zimmer Biomet

外科剪鉗和剃刀市場:2026-2032年全球市場預測(按產品類型、操作模式、刀片類型、應用、最終用戶和分銷管道分類)

外科剪鉗和剃刀市場:2026-2032年全球市場預測(按產品類型、操作模式、刀片類型、應用、最終用戶和分銷管道分類) 外科器械市場報告:按產品、類別、應用、最終用戶和地區分類,2026-2034年外科器械市場:2026-2032年全球市場預測(按產品類型、類別、材料、應用和最終用戶分類)

外科器械市場報告:按產品、類別、應用、最終用戶和地區分類,2026-2034年外科器械市場:2026-2032年全球市場預測(按產品類型、類別、材料、應用和最終用戶分類) 2026年全球智慧手術頭盔系統市場報告

2026年全球智慧手術頭盔系統市場報告 全球外科器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球外科器械市場報告2026年全球鉸接式紙鑷市場報告全球手術頭盔系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)充電式手術剪市場按產品類型、電池類型、刀片材質、銷售管道、應用和最終用戶分類,全球預測(2026-2032年)手術頭盔系統市場:按類型、組件、應用、最終用戶和分銷管道分類 - 全球預測 2026-2032 年

全球外科器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球外科器械市場報告2026年全球鉸接式紙鑷市場報告全球手術頭盔系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)充電式手術剪市場按產品類型、電池類型、刀片材質、銷售管道、應用和最終用戶分類,全球預測(2026-2032年)手術頭盔系統市場:按類型、組件、應用、最終用戶和分銷管道分類 - 全球預測 2026-2032 年