|

市場調查報告書

商品編碼

1721562

倉庫機器人市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Warehouse Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

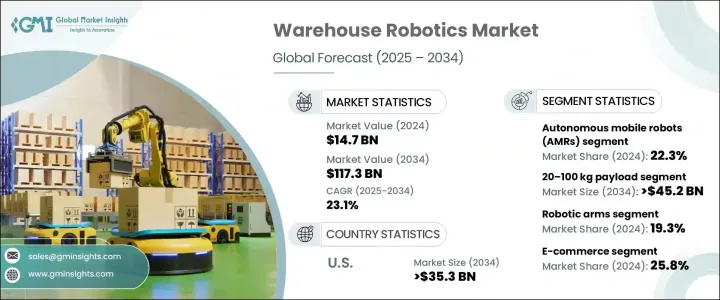

2024 年全球倉庫機器人市場價值為 147 億美元,預計到 2034 年將以 23.1% 的複合年成長率成長,達到 1,173 億美元。隨著倉儲和物流營運日益向自動化轉型以滿足不斷成長的消費者期望,該市場正在快速擴張。隨著電子商務的爆炸式成長,對精簡的供應鏈和更快的交付模式的需求比以往任何時候都更加強烈。線上零售商、第三方物流供應商和大型分銷商正在迅速投資機器人解決方案,以提高生產力、最大限度地減少對勞動力的依賴並最佳化倉庫佔地面積。

從智慧導航系統到基於精度的拾放技術,倉庫機器人正在改變庫存的管理、處理和運輸方式。工業 4.0 的出現以及人工智慧、物聯網和機器學習技術的整合進一步加強了機器人在倉庫生態系統中的作用。企業採用機器人技術不僅是為了管理大量訂單,也是為了在競爭日益激烈和自動化驅動的環境中確保其營運的未來發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 147億美元 |

| 預測值 | 1173億美元 |

| 複合年成長率 | 23.1% |

2024 年,AMR 領域佔有 22.3% 的佔有率。這些機器人採用人工智慧和地圖技術,可以自主導航倉庫地板並適應動態佈局和高流量條件。它們無需固定基礎設施即可運行,這使得它們非常適合電子商務履行中心等快節奏的環境。機械手臂也因其能夠自動執行挑選、堆疊和分類等重複性任務的能力而在整個倉庫設置中越來越受歡迎。當與人工智慧和機器學習相結合時,這些手臂可以實現更高的精度和靈活性,使它們能夠以更高的準確度和速度處理不同的 SKU。

倉庫機器人市場按最終用途細分為汽車、化學、半導體和電子、電子商務、醫療保健、食品和飲料、金屬和重型機械以及其他行業。 2024年,電子商務領域佔整體市佔率的25.8%。對數位商務的日益依賴增加了對支援高吞吐量操作和及時最後一英里交付的先進自動化工具的需求。電子商務參與者正在利用機器人技術來簡化庫存控制、提高揀貨效率並縮短訂單週轉時間以維持客戶滿意度。

預計到 2034 年,美國倉庫機器人市場規模將達到 353 億美元,這主要得益於頂級電子商務巨頭引領的自動化舉措的蓬勃發展。隨著勞動力成本的上升以及對智慧、可擴展自動化系統的需求不斷成長,美國倉庫正在轉向機器人技術來提高營運效率並降低管理費用。

全球倉庫機器人市場的知名企業包括 ABB、KUKA、Fanuc Corporation、Yaskawa Electric Corporation、Dematic 和 Honeywell Intelligrated。這些公司正在大力投資下一代機器人技術,以提供更智慧、更具適應性的解決方案。透過人工智慧整合、與物流領導者的策略合作以及持續的研發,這些公司旨在加強其在高成長地區的影響力並滿足倉儲領域不斷變化的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 新興的電子商務產業

- 人工智慧和機器學習的進步

- 勞動力短缺和工資上漲

- 自主移動機器人 (AMR) 的採用率不斷提高

- 零售和物流行業對倉庫自動化的需求不斷成長

- 產業陷阱與挑戰

- 初期投資成本高

- 系統整合的複雜性

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按組件,2021 - 2034 年

- 安全系統

- 通訊系統

- 作業控制系統

- 交通管理系統

- 電池充電系統

- 感應器

- 控制器

- 驅動器

- 機械手臂

第6章:市場估計與預測:按機器人類型,2021 - 2034 年

- 自主移動機器人(AMR)

- 自動導引車(AGV)

- 關節型機器人

- 圓柱形機器人

- SCARA機器人

- 協作機器人

- 並聯機器人

- 笛卡兒機器人

第7章:市場估計與預測:按有效載荷容量,2021 - 2034 年

- 少於20公斤

- 20–100公斤

- 100–200公斤

- 超過200公斤

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 汽車

- 化學

- 半導體和電子產品

- 電子商務

- 食品和飲料

- 衛生保健

- 金屬和重型機械

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- ABB

- Amazon Robotics

- Bastian Solutions

- Boston Dynamics

- Daifuku

- Dematic

- Fanuc Corporation

- Fives

- Fortna

- Geek+

- GreyOrange

- Honeywell Intelligrated

- Knapp

- Korber

- KUKA

- Murata Machinery

- SSI Schaefer

- Symbotic

- Swisslog

- Vanderlande

- Yaskawa Electric Corporation

The Global Warehouse Robotics Market was valued at USD 14.7 billion in 2024 and is anticipated to grow at a CAGR of 23.1% to reach USD 117.3 billion by 2034. The market is witnessing rapid expansion as warehousing and logistics operations increasingly transition toward automation to meet rising consumer expectations. With the explosion of e-commerce, the need for streamlined supply chains and faster delivery models has never been greater. Online retailers, third-party logistics providers, and large-scale distributors are rapidly investing in robotic solutions to boost productivity, minimize labor dependency, and optimize warehouse floor space.

From intelligent navigation systems to precision-based pick-and-place technologies, warehouse robotics are transforming how inventory is managed, handled, and shipped. The emergence of Industry 4.0 and the convergence of AI, IoT, and ML technologies are further reinforcing the role of robotics in warehouse ecosystems. Organizations are adopting robotics not only to manage high order volumes but also to future-proof their operations in an increasingly competitive and automation-driven landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.7 Billion |

| Forecast Value | $117.3 Billion |

| CAGR | 23.1% |

AMRs segment held a 22.3% share in 2024. These robots are powered by AI and mapping technologies, allowing them to navigate warehouse floors autonomously and adapt to dynamic layouts and high-traffic conditions. Their ability to operate without fixed infrastructure makes them ideal for fast-paced environments such as e-commerce fulfillment centers. Robotic arms are also gaining traction across warehouse setups for their capacity to automate repetitive tasks like picking, palletizing, and sorting. When integrated with AI and machine learning, these arms achieve higher precision and flexibility, enabling them to handle diverse SKUs with greater accuracy and speed.

The warehouse robotics market is segmented by end-use into automotive, chemical, semiconductor & electronics, e-commerce, healthcare, food & beverage, metals & heavy machinery, and other industries. In 2024, the e-commerce sector accounted for 25.8% of the overall market share. The increasing reliance on digital commerce has amplified the demand for advanced automation tools to support high-throughput operations and timely last-mile delivery. E-commerce players are leveraging robotics to streamline inventory control, improve picking efficiency, and deliver faster order turnaround times to maintain customer satisfaction.

U.S. Warehouse Robotics Market is projected to reach USD 35.3 billion by 2034, largely driven by surging automation initiatives led by top-tier e-commerce giants. With rising labor costs and the growing need for intelligent, scalable automation systems, U.S. warehouses are turning to robotics to enhance operational efficiency and reduce overheads.

Prominent players in the Global Warehouse Robotics Market include ABB, KUKA, Fanuc Corporation, Yaskawa Electric Corporation, Dematic, and Honeywell Intelligrated. These companies are investing heavily in next-gen robotics to deliver smarter, more adaptive solutions. Through AI integration, strategic collaborations with logistics leaders, and continuous R&D, these firms aim to strengthen their presence across high-growth regions and address the evolving demands of the warehousing landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising E-commerce industry

- 3.2.1.2 Advancements in AI and machine learning

- 3.2.1.3 Labor shortages and rising wages

- 3.2.1.4 Increasing adoption of autonomous mobile robots (AMRs)

- 3.2.1.5 Growing demand for warehouse automation in the retail and logistics sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Complexity in system integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Billion)

- 5.1 Safety systems

- 5.2 Communication systems

- 5.3 Job control systems

- 5.4 Traffic management systems

- 5.5 Battery charging systems

- 5.6 Sensors

- 5.7 Controllers

- 5.8 Drives

- 5.9 Robotic arms

Chapter 6 Market estimates & forecast, By Robot Type, 2021 - 2034 (USD Billion)

- 6.1 Autonomous mobile robots (AMRs)

- 6.2 Automated guided vehicles (AGVs)

- 6.3 Articulated robots

- 6.4 Cylindrical robots

- 6.5 SCARA robots

- 6.6 Collaborative robots

- 6.7 Parallel robots

- 6.8 Cartesian robots

Chapter 7 Market estimates & forecast, By Payload Capacity, 2021 - 2034 (USD Billion)

- 7.1 Less than 20 kg

- 7.2 20–100 kg

- 7.3 100–200 kg

- 7.4 More than 200 kg

Chapter 8 Market estimates & forecast, By End Use, 2021 - 2034 (USD Billion)

- 8.1 Automotive

- 8.2 Chemical

- 8.3 Semiconductor & electronics

- 8.4 E-commerce

- 8.5 Food & beverage

- 8.6 Healthcare

- 8.7 Metals & heavy machinery

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Amazon Robotics

- 10.3 Bastian Solutions

- 10.4 Boston Dynamics

- 10.5 Daifuku

- 10.6 Dematic

- 10.7 Fanuc Corporation

- 10.8 Fives

- 10.9 Fortna

- 10.10 Geek+

- 10.11 GreyOrange

- 10.12 Honeywell Intelligrated

- 10.13 Knapp

- 10.14 Korber

- 10.15 KUKA

- 10.16 Murata Machinery

- 10.17 SSI Schaefer

- 10.18 Symbotic

- 10.19 Swisslog

- 10.20 Vanderlande

- 10.21 Yaskawa Electric Corporation

倉儲機器人市場報告:按類型、功能、最終用戶和地區分類(2026-2034 年)

倉儲機器人市場報告:按類型、功能、最終用戶和地區分類(2026-2034 年) 自動化揀選市場:依技術、組件、功能、終端用戶產業及倉庫類型分類-2026-2032年全球市場預測

自動化揀選市場:依技術、組件、功能、終端用戶產業及倉庫類型分類-2026-2032年全球市場預測 倉儲機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類庫存管理機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署、最終用戶和功能分類

倉儲機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類庫存管理機器人市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署、最終用戶和功能分類 全球倉儲機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球倉儲機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球庫存機器人市場報告

2026年全球庫存機器人市場報告 2025-2029年全球庫存管理機器人市場倉儲機器人市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

2025-2029年全球庫存管理機器人市場倉儲機器人市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 倉儲機器人市場-全球產業規模、佔有率、趨勢、機會及預測(依軟體、類型、酬載、功能、垂直產業、區域及競爭格局分類,2021-2031年)日本倉儲機器人市場報告:按類型、功能、最終用戶和地區分類(2026-2034年)

倉儲機器人市場-全球產業規模、佔有率、趨勢、機會及預測(依軟體、類型、酬載、功能、垂直產業、區域及競爭格局分類,2021-2031年)日本倉儲機器人市場報告:按類型、功能、最終用戶和地區分類(2026-2034年)