|

市場調查報告書

商品編碼

1721529

CT 掃描儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測CT Scanner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

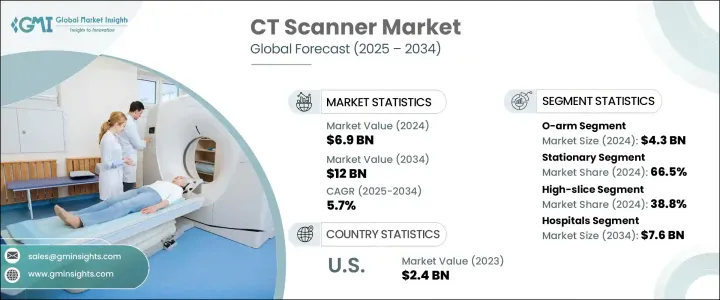

2024 年全球 CT 掃描儀市場價值為 69 億美元,預計將以 5.7% 的複合年成長率成長,到 2034 年達到 120 億美元。隨著醫療保健提供者優先考慮早期疾病檢測、精準醫療和改善治療結果,對先進診斷影像解決方案的需求持續成長。電腦斷層掃描 (CT) 掃描儀透過提供人體的高解析度橫斷面影像在實現這些目標中發揮關鍵作用。從常規篩檢到緊急診斷,CT 掃描儀已成為現代醫學影像的基石。醫療機構越來越依賴這些系統來視覺化複雜的內部結構,從而能夠準確診斷癌症、心血管疾病、內傷和神經系統疾病等病症。隨著政府和私人醫療保健提供者擴大基礎設施並採用數位健康技術,CT 掃描儀市場預計將持續成長。正在進行的創新進一步支持了這一勢頭,這些創新旨在利用人工智慧和機器學習演算法來減少掃描時間、降低輻射暴露並提高影像清晰度。隨著醫療保健產業傾向於微創手術和以患者為中心的護理,CT 影像的採用繼續以顯著的速度成長。

市場按架構分為 O 型臂和 C 型臂系統,其中 O 型臂部分在 2024 年創收 43 億美元。預計 2025 年至 2034 年期間該部分的複合年成長率為 5.6%。 O 型臂系統透過在手術室中直接提供即時 2D 和 3D 成像功能,正在改變手術成像格局。其緊湊、移動的設計使其能夠無縫整合到手術工作流程中,最大限度地減少了將患者運送到專用成像室的需要。外科醫生受益於手術過程中增強的可視性和準確性,從而降低了併發症的風險並帶來了更好的手術效果。預計對術中成像和精準引導手術的不斷成長的需求將在預測期內推動該領域的持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 69億美元 |

| 預測值 | 120億美元 |

| 複合年成長率 | 5.7% |

就類型而言,市場分為攜帶式 CT 掃描儀和固定式 CT 掃描儀。 2024 年,文具市場佔據主導地位,產值達 46 億美元,佔 66.5% 的市佔率。這些系統以其卓越的影像解析度、高速掃描和在高容量醫療保健環境中的強大性能而聞名。迭代重建、人工智慧診斷工具和多層掃描功能等最新進展提高了固定 CT 系統的診斷價值。對於尋求在廣泛的醫療應用中實現一致、高品質成像的醫院和診斷中心來說,它們仍然是首選。

2024 年北美 CT 掃描儀市場價值為 27 億美元,預計到 2034 年將達到 46 億美元。該地區市場擴張的動力來自於慢性病發病率的上升,以及對診斷基礎設施和研發的大力投資。尤其是美國,由於高昂的醫療支出和領先醫療設備製造商的強大影響力,繼續透過先進的影像解決方案引領創新。

全球 CT 掃描儀行業的一些知名企業包括富士膠片控股公司、Accuray、美敦力、島津製作所、Xoran Technologies、Koning Health、佳能、GE HealthCare Technologies、PLANMED、CurveBeam AI、三星電子、西門子醫療、東軟醫療系統、荷蘭皇家飛利浦和深圳荷蘭皇家安科高科技。這些公司正在大力投資人工智慧驅動的增強、迭代成像技術和策略合作,以提升診斷能力並擴大其全球影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 全球慢性病盛行率不斷上升

- 微創診斷程序日益受到青睞

- CT 掃描儀相對於其他影像方式的優勢

- CT掃描儀的技術進步

- 產業陷阱與挑戰

- 安裝和維護成本高昂

- CT掃描相關風險

- 成長動力

- 成長潛力分析

- 技術格局

- 監管格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依架構,2021 年至 2034 年

- 主要趨勢

- O型臂

- C臂

第6章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 便攜的

- 固定式

第7章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 高切片

- 中片

- 低切片

- 錐形束

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 人類

- 診斷

- 神經病學

- 腫瘤學

- 心臟病學

- 其他

- 術中

- 診斷

- 研究

- 獸醫

第9章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- CRO

- 門診手術中心

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 波蘭

- 奧地利

- 瑞士

- 斯洛伐克

- 捷克共和國

- 挪威

- 芬蘭

- 瑞典

- 丹麥

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 台灣

- 印尼

- 越南

- 柬埔寨

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Accuray

- Canon

- CurveBeam AI

- FUJIFILM Holdings Corporation

- GE HealthCare Technologies

- Koning Health

- Koninklijke Philips

- Medtronic

- Neusoft Medical Systems

- PLANMED

- Samsung Electronics

- Shenzhen Anke High-tech

- Shimadzu Corporation

- Siemens Healthineers

- Xoran Technologies

The Global CT Scanner Market was valued at USD 6.9 billion in 2024 and is expected to grow at a CAGR of 5.7% to reach USD 12 billion by 2034. The demand for advanced diagnostic imaging solutions continues to rise as healthcare providers prioritize early disease detection, precision medicine, and improved treatment outcomes. Computed Tomography (CT) scanners play a pivotal role in meeting these goals by delivering high-resolution, cross-sectional images of the human body. From routine screenings to emergency diagnostics, CT scanners have become a cornerstone of modern medical imaging. Healthcare institutions are increasingly relying on these systems to visualize complex internal structures, enabling accurate diagnoses for conditions such as cancer, cardiovascular diseases, internal injuries, and neurological disorders. As governments and private healthcare providers expand infrastructure and adopt digital health technologies, the CT scanner market is expected to witness consistent growth. This momentum is further supported by ongoing innovations that aim to reduce scanning times, lower radiation exposure, and enhance image clarity using AI and machine learning algorithms. With the healthcare industry leaning toward minimally invasive procedures and patient-centric care, the adoption of CT imaging continues to grow at a significant pace.

The market is segmented by architecture into O-arm and C-arm systems, with the O-arm segment generating USD 4.3 billion in 2024. This segment is projected to grow at a CAGR of 5.6% between 2025 and 2034. O-arm systems are transforming the surgical imaging landscape by offering real-time 2D and 3D imaging capabilities directly in operating rooms. Their compact and mobile design enables seamless integration into surgical workflows, minimizing the need to transport patients to dedicated imaging suites. Surgeons benefit from enhanced visibility and accuracy during procedures, which reduces the risk of complications and leads to better surgical outcomes. The growing demand for intraoperative imaging and precision-guided surgeries is expected to drive sustained growth in this segment over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $12 Billion |

| CAGR | 5.7% |

In terms of type, the market is divided into portable and stationary CT scanners. The stationary segment dominated in 2024, generating USD 4.6 billion and accounting for a 66.5% market share. These systems are known for their superior image resolution, high-speed scanning, and robust performance in high-volume healthcare settings. Recent advancements such as iterative reconstruction, AI-powered diagnostic tools, and multi-slice scanning capabilities have elevated the diagnostic value of stationary CT systems. They remain the preferred choice for hospitals and diagnostic centers seeking consistent, high-quality imaging across a wide range of medical applications.

The North America CT Scanner Market was valued at USD 2.7 billion in 2024 and is forecasted to reach USD 4.6 billion by 2034. The region's market expansion is driven by the rising incidence of chronic diseases, along with strong investments in diagnostic infrastructure and R&D. The U.S., in particular, continues to lead innovation through advanced imaging solutions fueled by high healthcare expenditure and a strong presence of leading medical device manufacturers.

Some of the prominent players in the global CT scanner industry include FUJIFILM Holdings Corporation, Accuray, Medtronic, Shimadzu Corporation, Xoran Technologies, Koning Health, Canon, GE HealthCare Technologies, PLANMED, CurveBeam AI, Samsung Electronics, Siemens Healthineers, Neusoft Medical Systems, Koninklijke Philips, and Shenzhen Anke High-tech. These companies are heavily investing in AI-driven enhancements, iterative imaging technologies, and strategic collaborations to elevate diagnostic capabilities and expand their global footprint.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases worldwide

- 3.2.1.2 Rising preference for minimally invasive diagnostic procedures

- 3.2.1.3 Advantages offered by CT scanner over other imaging modalities

- 3.2.1.4 Technological advancements in CT scanner

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Significant installation and maintenance cost

- 3.2.2.2 Risks associated with CT scan

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Architecture, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 O-arm

- 5.3 C-arm

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Portable

- 6.3 Stationary

Chapter 7 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 High-slice

- 7.3 Mid-slice

- 7.4 Low-slice

- 7.5 Cone beam

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Human

- 8.2.1 Diagnostic

- 8.2.1.1 Neurology

- 8.2.1.2 Oncology

- 8.2.1.3 Cardiology

- 8.2.1.4 Others

- 8.2.2 Intraoperative

- 8.2.1 Diagnostic

- 8.3 Research

- 8.4 Veterinary

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 CROs

- 9.4 Ambulatory surgical centers

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Poland

- 10.3.8 Austria

- 10.3.9 Switzerland

- 10.3.10 Slovakia

- 10.3.11 Czech Republic

- 10.3.12 Norway

- 10.3.13 Finland

- 10.3.14 Sweden

- 10.3.15 Denmark

- 10.3.16 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Taiwan

- 10.4.7 Indonesia

- 10.4.8 Vietnam

- 10.4.9 Cambodia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Accuray

- 11.2 Canon

- 11.3 CurveBeam AI

- 11.4 FUJIFILM Holdings Corporation

- 11.5 GE HealthCare Technologies

- 11.6 Koning Health

- 11.7 Koninklijke Philips

- 11.8 Medtronic

- 11.9 Neusoft Medical Systems

- 11.10 PLANMED

- 11.11 Samsung Electronics

- 11.12 Shenzhen Anke High-tech

- 11.13 Shimadzu Corporation

- 11.14 Siemens Healthineers

- 11.15 Xoran Technologies

CT掃描儀市場報告:趨勢、預測和競爭分析(至2035年)

CT掃描儀市場報告:趨勢、預測和競爭分析(至2035年) CT掃描儀市場:按切片配置、技術、安裝類型、應用和最終用途分類-全球預測(2026-2032年)

CT掃描儀市場:按切片配置、技術、安裝類型、應用和最終用途分類-全球預測(2026-2032年) CT及MRI造影劑市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、劑型、材質類型、功能、組件、設備

CT及MRI造影劑市場分析及預測(至2035年):類型、產品類型、應用、技術、最終用戶、劑型、材質類型、功能、組件、設備 CT掃描儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2025-2034)

CT掃描儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2025-2034) CT掃描儀市場規模、佔有率和成長分析(按技術、應用、模式、最終用戶和地區分類)-2026-2033年產業預測

CT掃描儀市場規模、佔有率和成長分析(按技術、應用、模式、最終用戶和地區分類)-2026-2033年產業預測 CT 掃描儀市場按產品類型、技術、應用、最終用戶和地區分類全球 CT 大腸造影市場規模(按類型、應用、最終用戶、地區和預測):

CT 掃描儀市場按產品類型、技術、應用、最終用戶和地區分類全球 CT 大腸造影市場規模(按類型、應用、最終用戶、地區和預測): CT 和 MRI顯影劑市場規模、佔有率、趨勢分析報告:按方式、產品、給藥途徑、應用、最終用途、地區、細分預測,2025-2030 年

CT 和 MRI顯影劑市場規模、佔有率、趨勢分析報告:按方式、產品、給藥途徑、應用、最終用途、地區、細分預測,2025-2030 年 先進 CT 掃瞄儀的全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

先進 CT 掃瞄儀的全球市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 錐形束 CT 掃描儀 (CBCT) 市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

錐形束 CT 掃描儀 (CBCT) 市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測