|

市場調查報告書

商品編碼

1721491

玻璃和鋁容器包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Glass and Aluminum Containers Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

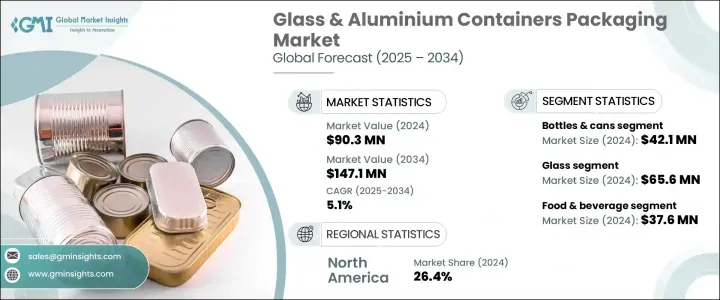

2024 年全球玻璃和鋁容器包裝市場價值為 9,030 萬美元,預計將以 5.1% 的複合年成長率成長,到 2034 年達到 1.471 億美元。隨著永續性成為各行各業的決定性力量,對環保包裝的需求正在迅速成長。消費者不再只是尋求功能性——他們正在積極選擇符合其環境價值觀的產品。這種行為轉變促使品牌優先考慮減少碳足跡和促進循環經濟實踐的包裝形式。玻璃和鋁完全可回收再利用,引領這場綠色革命。電子商務的激增提高了人們對健康和衛生的關注,而對塑膠使用的監管壓力不斷增加,進一步加劇了向永續包裝的轉變。

食品飲料、化妝品和製藥等行業正在進行這種轉變,不僅是為了滿足合規標準,也是為了贏得消費者的信任。品牌現在將包裝視為一種戰略資產,它傳達了品牌對地球的承諾並提高了客戶忠誠度。隨著創新提高成本效益和美觀度,玻璃和鋁容器正在成為高階產品和日常產品的首選。隨著生產技術的發展,製造商能夠提供更強大、更輕、更實惠的解決方案,以實現零浪費目標。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 9030萬美元 |

| 預測值 | 1.471億美元 |

| 複合年成長率 | 5.1% |

托盤和鋁箔容器的需求正在穩步成長,預計 2025 年至 2034 年的複合年成長率為 5.3%。鋁箔容器在食品配送和即食餐領域的需求強勁,這主要是因為其具有出色的耐熱性、輕質結構和高可回收性。這些好處確保食物在儲存和運輸過程中保持新鮮,同時符合永續發展目標。同時,玻璃托盤因其微波爐安全特性和高檔外觀,在高階包裝領域越來越受歡迎。隨著消費者偏好轉向便利、衛生和環保意識,這兩種形式都在擴展到多樣化的商業用途。

預計到 2034 年,僅在鋁包裝領域的複合年成長率就將達到 3.8%。鋁因其強度高、重量輕以及透過阻擋空氣、濕氣和污染物來保護產品完整性的能力而受到讚譽,正在成為食品、飲料和藥品包裝的首選。旨在減少塑膠垃圾的全球政策正在加速向鋁的轉變,特別是隨著回收基礎設施和技術的不斷改進。這些進步提高了鋁在整個生命週期內的成本效益和永續性,使其成為大規模應用的實用選擇。

預計到 2034 年,美國玻璃和鋁容器包裝市場規模將達到 3,220 萬美元。日益增強的環保意識和針對塑膠垃圾的政策驅動行動正在推動這一趨勢。聯邦計畫和地方對一次性塑膠的禁令正在鼓勵製造商採用可回收、低碳的包裝形式。更薄但更耐用的玻璃和最佳化的鋁回收製程等創新正在幫助企業在實現綠色目標的同時減少排放和成本。

包括 Ball Corporation、Verallia、Ardagh Group、Crown Holdings 和 OI Glass(歐文斯-伊利諾伊州)在內的主要參與者正在積極投資綠色技術和循環經濟計劃。這些公司正在擴大生產能力,推出可回收產品線,並與品牌進行策略合作,共同開發永續包裝解決方案。透過自動化、減少浪費和生態高效流程,他們在與不斷發展的監管框架保持一致的同時,為下一代包裝設定了新的基準。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 永續包裝需求不斷成長

- 嚴格的環境法規

- 回收技術的進步

- 不斷成長的飲料和製藥行業

- 優質美觀

- 產業陷阱與挑戰

- 生產和運輸成本高

- 易碎性和處理問題

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 玻璃

- 鋁

第6章:市場估計與預測:依貨櫃類型,2021 年至 2034 年

- 主要趨勢

- 瓶子和罐子

- 罐子

- 托盤/鋁箔容器

- 管子

- 小瓶/安瓿瓶

第7章:市場估計與預測:依最終用途產業,2021 年至 2034 年

- 主要趨勢

- 食品和飲料

- 個人護理和化妝品

- 製藥

- 工業和化學品

- 其他

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- OI Glass (Owens-Illinois)

- Ardagh Group

- Verallia

- BA Glass

- Vitro

- Gerresheimer

- Heinz-Glas

- Nihon Yamamura Glass Co.

- Ball Corporation

- Crown Holdings

- Trivium Packaging

- Can-Pack Group

- Toyo Seikan Group

- Silgan Holdings

The Global Glass & Aluminum Containers Packaging Market was valued at USD 90.3 million in 2024 and is estimated to grow at a CAGR of 5.1% to reach at USD 147.1 million by 2034. As sustainability becomes a defining force across industries, the demand for eco-friendly packaging is rapidly accelerating. Consumers are no longer just looking for functionality-they are actively choosing products that align with their environmental values. This behavioral shift is prompting brands to prioritize packaging formats that reduce carbon footprints and foster circular economy practices. Glass and aluminum, being fully recyclable and reusable, are leading this green revolution. The surge in e-commerce heightened focus on health and hygiene, and increasing regulatory pressures against plastic use are further intensifying the shift toward sustainable packaging.

Industries such as food and beverage, cosmetics, and pharmaceuticals are making this transition not only to meet compliance standards but also to earn consumer trust. Brands now view packaging as a strategic asset that communicates their commitment to the planet and drives customer loyalty. With innovations improving cost-efficiency and aesthetics, glass and aluminum containers are becoming the go-to choice for both premium and everyday products. As production technologies evolve, manufacturers are able to offer stronger, lighter, and more affordable solutions that align with zero-waste goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.3 Million |

| Forecast Value | $147.1 Million |

| CAGR | 5.1% |

The demand for trays and foil containers is increasing steadily, with projections indicating a CAGR of 5.3% from 2025 to 2034. Aluminum foil containers are seeing strong uptake across the food delivery and ready-to-eat meal segments, primarily due to their excellent thermal resistance, lightweight structure, and high recyclability. These benefits ensure food remains fresh during storage and transit while aligning with sustainability goals. At the same time, glass trays are gaining momentum in high-end packaging due to their microwave-safe properties and premium look. With consumer preferences shifting toward convenience, hygiene, and eco-consciousness, both formats are expanding into diverse commercial use cases.

The aluminum packaging segment alone is anticipated to witness a CAGR of 3.8% through 2034. Praised for its strength, low weight, and ability to safeguard product integrity by blocking air, moisture, and contaminants, aluminum is becoming a top choice for food, beverage, and pharmaceutical packaging. Global policies aimed at reducing plastic waste are accelerating the shift to aluminum, especially as recycling infrastructure and technologies continue to improve. These advancements enhance aluminum's cost-effectiveness and sustainability across its lifecycle, making it a practical choice for large-scale applications.

The U.S. Glass & Aluminum Containers Packaging Market is forecasted to reach USD 32.2 million by 2034. Growing environmental awareness and policy-driven action against plastic waste are fueling this trend. Federal programs and local bans on single-use plastics are encouraging manufacturers to adopt recyclable, low-carbon packaging formats. Innovations such as thinner yet more durable glass and optimized aluminum recycling processes are helping companies cut emissions and costs while meeting green targets.

Major players, including Ball Corporation, Verallia, Ardagh Group, Crown Holdings, and O-I Glass (Owens-Illinois), are actively investing in green technologies and circular economy initiatives. These companies are scaling up production capabilities, introducing recyclable product lines, and engaging in strategic collaborations with brands to co-develop sustainable packaging solutions. Through automation, waste reduction, and eco-efficient processes, they are setting new benchmarks in next-generation packaging while aligning with evolving regulatory frameworks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable packaging

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Advancements in recycling technology

- 3.2.1.4 Growing beverage and pharmaceutical industries

- 3.2.1.5 Premium and aesthetic appeal

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and transportation costs

- 3.2.2.2 Breakability and Handling Issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn & million units)

- 5.1 Key trends

- 5.2 Glass

- 5.3 Aluminum

Chapter 6 Market Estimates and Forecast, By Container Type, 2021 – 2034 ($ Mn & million units)

- 6.1 Key trends

- 6.2 Bottles & Cans

- 6.3 Jars

- 6.4 trays/foil containers

- 6.5 tubes

- 6.6 Vials/ampoules

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 ($ Mn & million units)

- 7.1 Key trends

- 7.2 Food & Beverage

- 7.3 Personal Care & Cosmetics

- 7.4 Pharmaceuticals

- 7.5 Industrial & Chemicals

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & million units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 O-I Glass (Owens-Illinois)

- 9.2 Ardagh Group

- 9.3 Verallia

- 9.4 BA Glass

- 9.5 Vitro

- 9.6 Gerresheimer

- 9.7 Heinz-Glas

- 9.8 Nihon Yamamura Glass Co.

- 9.9 Ball Corporation

- 9.10 Crown Holdings

- 9.11 Trivium Packaging

- 9.12 Can-Pack Group

- 9.13 Toyo Seikan Group

- 9.14 Silgan Holdings

折疊式散裝容器市場預測至2034年-全球材料、產品類型、容量、分銷管道、應用、最終用戶和區域分析

折疊式散裝容器市場預測至2034年-全球材料、產品類型、容量、分銷管道、應用、最終用戶和區域分析 模塑纖維泡殼式容器市場:依產品類型、材料類型、應用和分銷管道分類-2026-2032年全球預測吹塑成型容器市場:全球市場按產品類型、材料、容量範圍和應用分類的預測 - 2026-2032年貨櫃捆綁系統市場:依產品類型、材質、貨櫃類型、應用、產業和通路分類-2026-2032年全球預測預開袋製袋機市場:依包裝材料、技術、類型、薄膜類型、產能、最終用途產業和銷售管道,全球預測,2026-2032年捲裝預開袋市場按材料類型、袋子尺寸、分銷管道和最終用途行業分類,全球預測,2026-2032年發光反應杯市場按產品類型、材料、分銷管道和最終用戶分類,全球預測(2026-2032)

模塑纖維泡殼式容器市場:依產品類型、材料類型、應用和分銷管道分類-2026-2032年全球預測吹塑成型容器市場:全球市場按產品類型、材料、容量範圍和應用分類的預測 - 2026-2032年貨櫃捆綁系統市場:依產品類型、材質、貨櫃類型、應用、產業和通路分類-2026-2032年全球預測預開袋製袋機市場:依包裝材料、技術、類型、薄膜類型、產能、最終用途產業和銷售管道,全球預測,2026-2032年捲裝預開袋市場按材料類型、袋子尺寸、分銷管道和最終用途行業分類,全球預測,2026-2032年發光反應杯市場按產品類型、材料、分銷管道和最終用戶分類,全球預測(2026-2032) 全球折疊容器市場:市場規模、佔有率和趨勢分析(按材料、產品類型、最終用途和地區分類),細分市場預測(2026-2033 年)

全球折疊容器市場:市場規模、佔有率和趨勢分析(按材料、產品類型、最終用途和地區分類),細分市場預測(2026-2033 年) 全球容器清洗系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球容器清洗系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球安全卡扣容器市場報告

2026年全球安全卡扣容器市場報告