|

市場調查報告書

商品編碼

1721478

瓦楞折疊包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Corrugated Fanfold Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

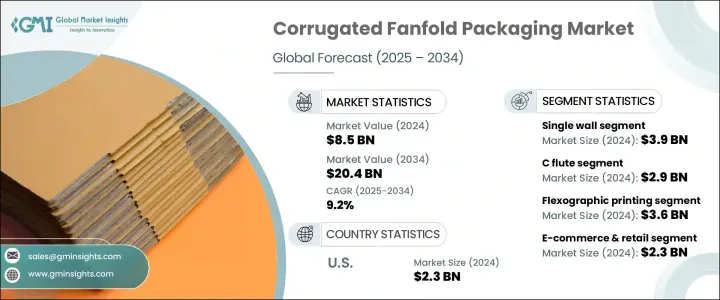

2024 年全球瓦楞紙折疊包裝市場價值為 85 億美元,預計到 2034 年將以 9.2% 的複合年成長率成長,達到 204 億美元。這一成長主要歸因於電子商務的快速崛起、消費者購買模式的動態變化以及整個行業向永續且具有成本效益的包裝解決方案的轉變。隨著線上零售在全球範圍內的擴張,對更智慧、更靈活的包裝形式的需求正在迅速成長。各行業的企業都在優先考慮能夠實現合適尺寸包裝的解決方案,以簡化操作、減少浪費並降低運輸成本。瓦楞紙折疊包裝正迅速成為注重營運靈活性和永續性的企業的首選。折疊格式支援自動化和客製化,同時無需儲存多種預製盒子尺寸。這大大減少了存儲空間,並允許公司根據不同的訂單量客製化包裝。消費者的環保意識和監管部門對企業減少碳足跡的壓力進一步加速了可回收、輕量折疊解決方案的採用。

隨著技術進步和智慧包裝解決方案的不斷發展,製造商正在投資與折疊包裝無縫整合的自動化工具和按需制盒系統。這些創新不僅提高了包裝效率,而且最大限度地減少了過多材料的使用並降低了物流成本。此外,食品配送、電子產品和時尚等領域對環保包裝的需求不斷成長,激發了全球市場對折疊包裝的持續興趣。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 85億美元 |

| 預測值 | 204億美元 |

| 複合年成長率 | 9.2% |

在牆體類型中,單壁折疊板部分在 2024 年創造了 39 億美元的收入。該部分因其輕量化設計和成本效益而廣受歡迎,使其成為電子商務零售商和訂閱服務的首選。隨著線上購物的持續成長(特別是化妝品、時尚和食品等消費類別),單壁折疊板提供了一個可靠的解決方案,在強度和經濟性之間取得平衡。食品配送平台的持續擴張也推動了對永續且適合不同訂單規模的包裝的需求,有助於減少浪費並最佳化配送效率。

C 型瓦楞在瓦楞類型中佔有最大的佔有率,2024 年的市值為 29 億美元。它能夠支撐中等重量,同時保持耐用性和抗衝擊性,使其成為廣泛應用的理想選擇。這種瓦楞類型廣泛用於包裝食品和飲料,例如瓶裝飲料、罐頭食品和餐包。其結構完整性確保了運輸安全,使其成為尋求提高包裝性能和永續性的公司的首選。

2024 年,德國瓦楞紙折疊包裝市場產值達到 4.811 億美元。該國作為電子產品、消費品和食品主要出口國的強勢地位繼續推動對客製化和耐用包裝的需求。德國工業和汽車行業的成長進一步推動了對雙層和三層折疊紙板的需求。企業也面臨越來越大的壓力,需要遵守歐盟永續發展指令,鼓勵廣泛採用可回收和生物基包裝替代品。

全球瓦楞折疊包裝市場的主要參與者包括 Smurfit Kappa Group、Ribble Packaging、Papierfabrik Palm、Stora Enso、Hinojosa Packaging Group、Kite Packaging、Abbe、DS Smith、International Paper Company、Rondo Ganahl、Papeles y Conversiones de Mexico、Corrugated。這些公司正在積極投資自動化技術,擴大產品組合以滿足電子和製藥等利基行業的需求,並通過 FSC 認證和可回收包裝材料符合綠色計劃。與電子商務平台和物流供應商的策略合作也使得包裝作業更快、交貨週轉更快。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 電子商務與網上購物的興起

- 客製化和個人化需求日益成長

- 自動化和智慧包裝解決方案的興起

- 食品飲料業的擴張

- 數位印刷技術的進步

- 產業陷阱與挑戰

- 自動化包裝系統初始投資高

- 回收和廢棄物管理挑戰

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按牆體類型,2021 年至 2034 年

- 主要趨勢

- 單壁

- 雙層牆

- 三層牆

第6章:市場估計與預測:按長笛類型,2021 年至 2034 年

- 主要趨勢

- B長笛

- C長笛

- E長笛

- 其他

第7章:市場估計與預測:按印刷技術,2021 年至 2034 年

- 主要趨勢

- 柔版印刷

- 數位印刷

- 平版印刷

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 電子商務與零售

- 消費性電子產品

- 醫療保健和製藥

- 個人護理和化妝品

- 汽車和工業產品

- 食品和飲料

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbe

- Corrugated Supplies Company

- DS Smith

- Hinojosa Packaging Group

- International Paper Company

- Kite Packaging

- Mondi

- Papeles y Conversiones de Mexico

- Papierfabrik Palm

- Ribble Packaging

- Rondo Ganahl

- Smurfit Kappa Group

- Stora Enso

- WestRock

The Global Corrugated Fanfold Packaging Market was valued at USD 8.5 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 20.4 billion by 2034. This surge is largely attributed to the rapid rise in e-commerce, dynamic shifts in consumer purchasing patterns, and an industry-wide pivot toward sustainable and cost-efficient packaging solutions. As online retail expands globally, the demand for smarter, more flexible packaging formats is growing rapidly. Businesses across sectors are prioritizing solutions that enable right-sized packaging to streamline operations, reduce waste, and lower shipping costs. Corrugated fanfold packaging is fast becoming a preferred choice for enterprises focused on operational agility and sustainability. The fanfold format supports automation and customization while eliminating the need for stocking multiple pre-formed box sizes. This significantly reduces storage space and allows companies to tailor packaging for varying order volumes. Environmental consciousness among consumers and regulatory pressure on businesses to cut down on their carbon footprint has further accelerated the adoption of recyclable, lightweight fanfold solutions.

With technological advancement and smart packaging solutions gaining traction, manufacturers are investing in automation tools and on-demand box-making systems that seamlessly integrate with fanfold packaging. These innovations not only improve packaging efficiency but also minimize excess material use and drive down logistics costs. Moreover, the increasing demand for eco-friendly packaging from sectors like food delivery, electronics, and fashion is fueling sustained interest in fanfold packaging across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.5 Billion |

| Forecast Value | $20.4 Billion |

| CAGR | 9.2% |

Among wall types, the single wall fanfold boards segment generated USD 3.9 billion in 2024. This segment is popular for its lightweight design and cost-effectiveness, making it the go-to option for e-commerce retailers and subscription-based services. As online purchasing continues to rise-especially for consumer categories like cosmetics, fashion, and food-single wall fanfold boards offer a reliable solution that balances strength with affordability. The continued expansion of food delivery platforms is also fueling demand for packaging that is both sustainable and tailored to different order sizes, helping reduce waste and optimize delivery efficiency.

C flute held the largest share among flute types, generating USD 2.9 billion in 2024. Its ability to support moderate weight while maintaining durability and impact resistance makes it ideal for a wide range of applications. This flute type is widely used for packaged food and beverage items such as bottled drinks, canned goods, and meal kits. Its structural integrity ensures safe transport, making it a preferred option for companies looking to enhance both performance and sustainability in packaging.

Germany Corrugated Fanfold Packaging Market generated USD 481.1 million in 2024. The country's strong position as a major exporter of electronics, consumer goods, and food products continues to drive demand for custom and durable packaging. Growth in Germany's industrial and automotive sectors further boosts the need for double and triple-wall fanfold boards. Businesses are also under increasing pressure to align with EU sustainability directives, encouraging widespread adoption of recyclable and bio-based packaging alternatives.

Key players in the Global Corrugated Fanfold Packaging Market include Smurfit Kappa Group, Ribble Packaging, Papierfabrik Palm, Stora Enso, Hinojosa Packaging Group, Kite Packaging, Abbe, DS Smith, International Paper Company, Rondo Ganahl, Papeles y Conversiones de Mexico, Corrugated Supplies Company, and Mondi. These companies are actively investing in automation technologies, expanding product portfolios to cater to niche industries such as electronics and pharmaceuticals, and aligning with green initiatives through FSC-certified and recyclable packaging materials. Strategic collaborations with e-commerce platforms and logistics providers are also enabling faster packaging operations and improved delivery turnaround.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise of e-commerce and online shopping

- 3.2.1.2 Growing demand for customization and personalization

- 3.2.1.3 Rise in automation and smart packaging solutions

- 3.2.1.4 Expansion in the food and beverage industry

- 3.2.1.5 Advancements in digital printing technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment in automated packaging systems

- 3.2.2.2 Recycling and waste management challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Wall Type, 2021 – 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Single wall

- 5.3 Double wall

- 5.4 Triple wall

Chapter 6 Market Estimates and Forecast, By Flute Type, 2021 – 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 B flute

- 6.3 C flute

- 6.4 E flute

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2021 – 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Flexographic printing

- 7.3 Digital printing

- 7.4 Lithographic printing

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 E-commerce & retail

- 8.3 Consumer electronics

- 8.4 Healthcare & pharmaceuticals

- 8.5 Personal care & cosmetics

- 8.6 Automotive & industrial goods

- 8.7 Food & beverage

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbe

- 10.2 Corrugated Supplies Company

- 10.3 DS Smith

- 10.4 Hinojosa Packaging Group

- 10.5 International Paper Company

- 10.6 Kite Packaging

- 10.7 Mondi

- 10.8 Papeles y Conversiones de Mexico

- 10.9 Papierfabrik Palm

- 10.10 Ribble Packaging

- 10.11 Rondo Ganahl

- 10.12 Smurfit Kappa Group

- 10.13 Stora Enso

- 10.14 WestRock

瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類)

瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類) 全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年

全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年 按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測

按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測 瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年)

瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年) 紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 紙箱內襯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

紙箱內襯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 塑膠瓦楞紙板市場,規模,佔有率,趨勢,產業分析:各材料類型,各厚度,各最終用途,各地區,2025年~2034年的市場預測

塑膠瓦楞紙板市場,規模,佔有率,趨勢,產業分析:各材料類型,各厚度,各最終用途,各地區,2025年~2034年的市場預測